Will the Chinese Yuan become the world's reserve currency?

In time, it well might.

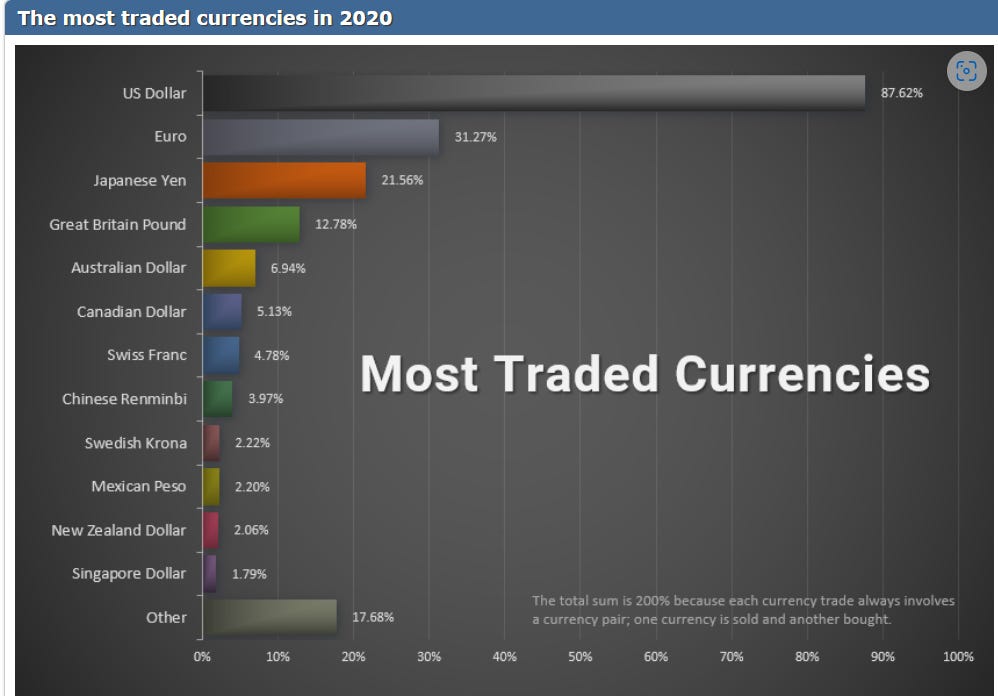

Over 200 years ago, the British pound was the world’s reserve currency bolstered by the size and scale of British seaborne trade. But United States greenback displaced the pound as the American trading economy grew and prospered. By 2020, the greenback accounted for well over 80% of world trade and the British pound struggled to hold fourth place behind the Euro and Japanese Yen. Canadian and Australian dollars and Swiss francs and the Chinese currency have measurable roles in currency trades.

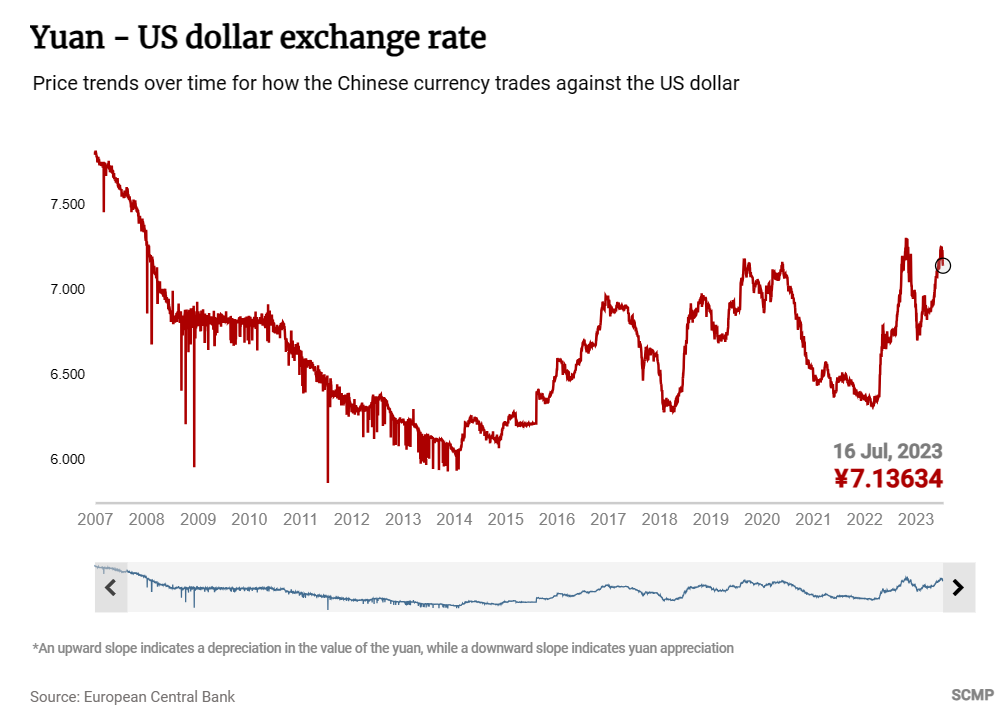

But the Chinese currency is increasingly become the currency in which trading with China is settled. Between 2020 and 2022 the share of Chinese trade settled in the Yuan rose from 20% to 30% according to Allianzbanc. The desire of the Chinese to increase the usage of its own currency for settlement of trade is understandable but comes at a price. The Yuan is losing value relative to the U.S. dollar (the chart shows the U.S. dollar rising relative to the Yuan). For most countries, a declining currency manifests itself in higher inflation, and many countries actively defend their currency when it comes under pressure.

That is not happening in the case of China. Instead, China seems on the brink of deflation and welcomes the lower exchange rate which may spur higher exports and fuel a recovery in economic growth.

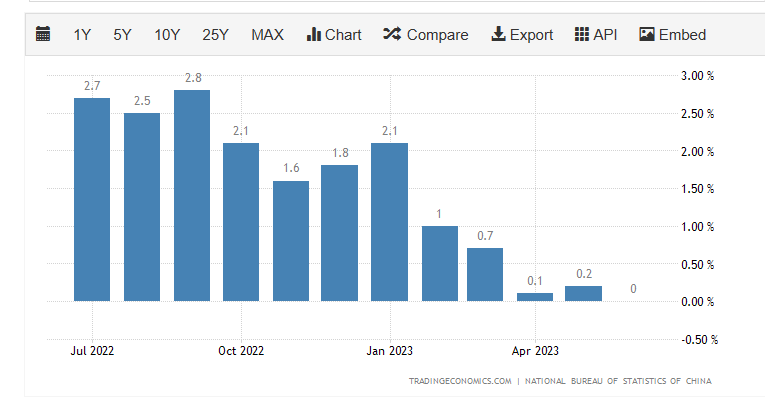

Chinese inflation rate reported by Trading Economics.

The relatively high inflation in Europe and North America combined with the declining currency and low inflation in China should see China benefit from an increase in its balance of trade despite the nascent efforts of many countries to bring production back to their own shores. China’s dramatic economic success for the past few decades can be traced to their relative labor cost advantage and this currency trend increases that advantage. In parallel, China has made massive investments abroad. According to World Bank data published by Macrotrends, China’s foreign investment has grown from virtually none in 1980 to over $300 billion annually today and totals well over $1 trillion for the past five years. Income from those foreign investments will create more demand for Chinese currency as the profits are repatriated.

The U.S. credit rating dropped below AAA as Fitch downgraded the country’s bonds owing to excess spending, excess borrowing, and persistent deficits under Joe Biden and his predessor Donald Trump. Lower credit ratings become higher bond rates and less confidence in U.S. treasuries as “risk free” securities. Markets reacted by selling U.S. stocks and bonds.

American analysts and economists are dismissive of the possibility that the U.S. dollar will lose its status as the world’s reserve currency just as United Kingdom leaders were dismissive of the possibility the world would ever shift away from Sterling. In a nutshell, those conclusions reflect a desired outcome and a rationalization of trade policy with little attention to what is actually happening. Reality is the 70-80% of the products sold in Walmart are sourced in China and Chinese suppliers comprise 75% of Amazon.com’s growth in vendors. China is today one of the world’s largest importers of copper, aluminum, iron ore, coal and oil but is also one of the largest exporters of the refined metals. Mines depend on China as a customer and manufacturers depend on China as a supplier. Western technology titans like Apple (AAPL), Microsoft (MSFT), Amazon (AMZN) and NVidia (NVDA) While Western governments are trying to shift to “onshoring” jobs from China, they are having little success to date. The currency and inflation macroeconomic trends will make that chore even harder.

In my opinion, the U.S. dollar will lose is status as the world’s reserve currency some time in the next thirty or forty years. That loss will reflect a parade of poor fiscal and monetary decisions by U.S. administrations that have seen U.S. sovereign debt grow out of control and the seeds of pervasive entrenched inflation created by poorly considered energy policies vilifying fossil fuels while China builds its economy sensibly using coal and oil without any concern for the nonsense that permeates Washington regarding the role of CO2 in climate. CO2 has virtually no effect on climate, now well established by recent climate research1 by phyicists rather than political scientists seeking to promote the leftist narrative to benefit from government funding of what they call “research”.

China and the rest of Asia, India in particular, are developing into the real titans of international commerce and building the educational infrastructure to support their emergence as world powers both militarily and economically. China graduates over 8 million students from its universities annually, with over 700,000 of those engineers or with advanced technical degrees. United States has about 2 million university graduates of which less than 6% are engineers and a tiny fraction have advanced degrees.

Shortages of metals to support the “transition” to the so-called “carbon free” economy are seeing massive wealth transfers to jurisdictions which are host to large deposits of copper, nickel, cobalt, graphite, iron ore and lithium while United States lags in development of its own mining deposits under the weight of leftist “environmental” policies.

These powerful trends seem secular and pervasive and if they persist, which I expect they will, the risk of the U.S. dollar losing its status as the world’s reserve currency is not trivial.

[2004.00708] Saturation of the Infrared Absorption by Carbon Dioxide in the Atmosphere (arxiv.org)

World Atmospheric CO2, its 14C Specific Activity, Non-fossil Component, Anthropogenic Component, and Emissions 1715-2018

Too many variables , which you have ably identified, to guess ; other than to say :

Does the world really want its reserve currency to be controlled by a bunch of evil tyrants ?