Where are the risks and opportunities in Canadian energy names?

Models may provide some guidance but like climate models, are an oversimplification of many complex variables

I keep up to date models on a number of Canadian Exploration and Production (E&P) stocks and hold sizeable positions in most of them. With the recent volatility in both oil & gas prices, I have done some Monte Carlo simulation of where the best spots to allocate my investment dollars lie, and share my insights in this article.

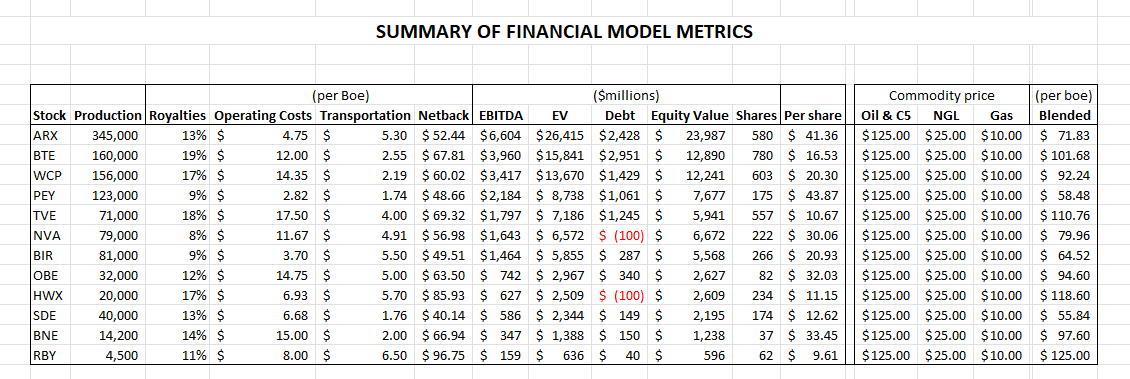

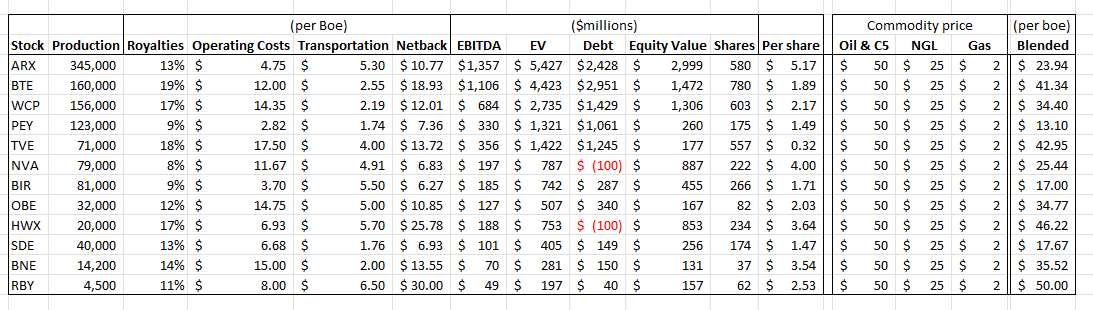

For the purposes of simulation, I chose a low-high range of CDN$2.00 to CDN$10.00 per gigajoule for gas and a low-high range of CDN$50 to CDN$125 for oil and condensate and applied those prices to each model with the results set out in a chart, carrying natural gas liquids (propane, butane and ethane) at a flat CDN$25.00 per boe.

During the past couple of years, we have seen CDN$125 per boe for oil and CDN$10 per gigajoule for natural gas, but those prices didn’t last long. During the pandemic, we had a brief exposure to oil in the CDN$50 range (it even went negative for a day or two) and natural gas at or below CDN$2.00 per gigajoule. These prices are all within the range of the possible.

I have assumed no change to current dividend rates and ignored the benefit or drag of existing hedge books (which overstates the benefit of higher prices and ignores the protection of hedges when prices fall). The simulation makes no adjustments for cost inflation or deflation, and is simply a sensitivity analysis to commodity prices.

Investors typically over react to bad news and underappreciate favorable trends (Thaler, 2017). In volatile markets, calm and objective valuation gives way to fear of loss. It is no surprise that there are periods of over valuation and undervaluation notwithstanding the legion of Nobel prize winning economists who promoted the efficient market hypothesis (Fama, Markowitz, Miller, Sharpe, Modigliani). But a calm and objective fact-based analysis will over time rule the day.

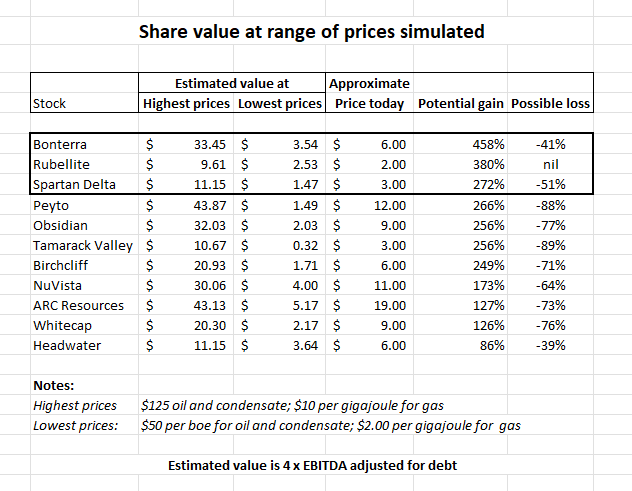

Here is the chart.

The highest leverage to favorable prices is held by Bonterra, Rubellite and Spartan Delta. Peyto, Obsidian, Tamarack Valley and Birchcliff have somewhat similar risk-reward profiles, while Nuvista, ARC, Whitecap and Headwater have more moderate potential and somewhat greater risk. Implicit in the analysis is the assumption that the respective prices persist for an extended period of time, not realistic but still useful for simulation.

Rubellite is unique in that its shares are trading below my estimate of value even at the lowest prices assumed (which are lower than today). The assumption of 4x EBITDA as enterprise value fails to reflect a higher multiple where warranted by growth within cash flow - arguably Rubellite, Spartan Delta, Tamarack Valley, ARC and Headwater merit higher multiples if commodity prices turn out to be firm.

My largest positions are in Birchcliff (for its unhedged exposure to natural gas prices which have little friction and can move from low to nosebleed levels overnight if shortages emerge, as they did in Texas a couple of years ago) and Rubellite (for its low risk high-growth profile. I hold positions in Spartan Delta, Peyto and Whitecap and am short NuVista.

My estimates are reasonable although not error free nor clairvoyant. To create this chart, I simply plugged in the price assumptions to existing models that I have used for a couple of years and have proven reasonably reliable when compared to actual results when released.

Here is a summary of those data inputs for the highest prices I modeled. I have rounded debt to the nearest million dollars and production to the nearest 100 Boe/day. Precision is pedantic and the enemy of sensitivity analysis.

Take the conclusion of “nil” risk of loss for Rubellite and Spartan Delta with a grain of salt. In commodity markets, there is always risk and my conclusion is limited to the prices assumed and ignores drilling risk, regulatory risk, financial risk, management risk, and a host of other risks including “finger trouble” by me in creating and applying the models.

The purpose of the article is to point out that even when commodity prices are in common, the risks and opportunities in E&P stocks differ widely and reflect their product mix, operating costs, exposure to differing royalties and capital structure. If prices keep falling, I will add to my holdings in Rubellite, Bonterra and Spartan Delta and sell none of my holdings.

what's your opinion on Athabasca Oil especially after the JV with Cenovus

many thanks for all your comments, happy holidays

Are you still long Nickel28?