Time for calm and patience

Oil prices remain at profitable levels and there is no evidence supply growth worldwide

Oil prices have fallen over 30% from their peak earlier this year, largely reflecting nervous investors concerned that COVID lockdowns will impair growth in China and see a reduction in world demand that will put pressure on prices. According to Statista, China consumed about 718.5 million metric tonnes of crude oil in 2021. A metric tonne comprises 7.46 barrels of crude so China’s usage is 718.5 x 7.46 divided by 365 = 14.7 million barrels a day. Assuming oil consumption is directly correlated with economic activity, a deep recession (say a 5% reduction in GDP) might see Chinese demand fall to 14 million barrels a day taking 700,000 barrels of demand out of the market.

Two factors are worth consideration. First, the lockdowns are a choice, not compelled by external factors. In a major economic downturn, it is questionable whether the Chinese government will continue with its “zero COVID” policy. Assume it does and demand falls by 700,000 barrels a day. Second, the United States is withdrawing 1 million barrels a day from it’s Strategic Petroleum Reserve and that supply will dry up sooner or later. These forces will likely counteract one another with the absence of SPR withdrawals offsetting a decline in Chinese demand by mid-next year.

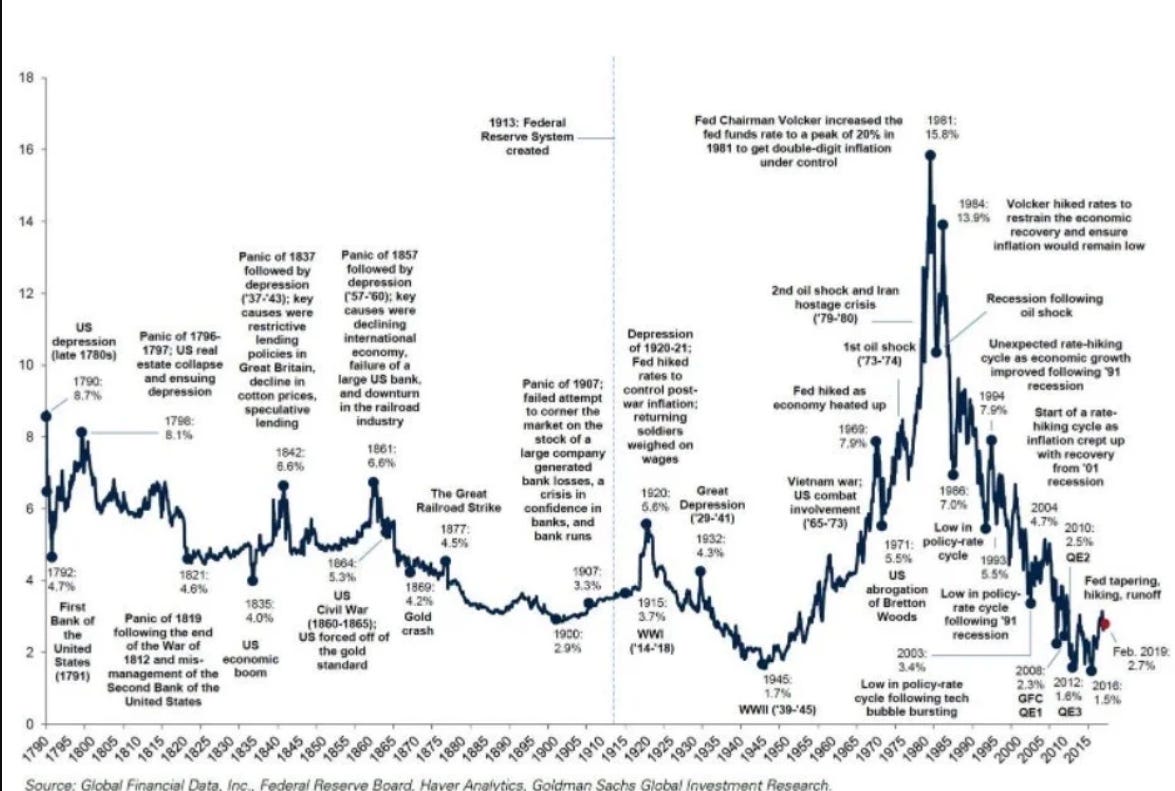

A more important factor in the supply-demand balance is the state of the economies of the world outside of China. Interest rates are on an upward march and that trend is likely to continue until inflation is tamed and history suggests that won’t happen quickly. A global recession might reduce demand by 3 or 4 million barrels a day and prices will plummet. Then what?

Policy makers will tolerate a recession for as long as voters will tolerate economic malaise and that is unlikely to be an extended period. The longest recession since the Great Depression was 2007-2009 which lasted over two years. The next Presidential election in United States is just two years away and incumbents get tossed almost always if the election takes place during a period of economic malaise. The policy tug-of-war between inflation fighting and recession is hard to assess, but history has shown us that democracies are willing to put up with higher than recent interest rates for an extended period and adapt to them so the economy grows despite rates that today would seem high.

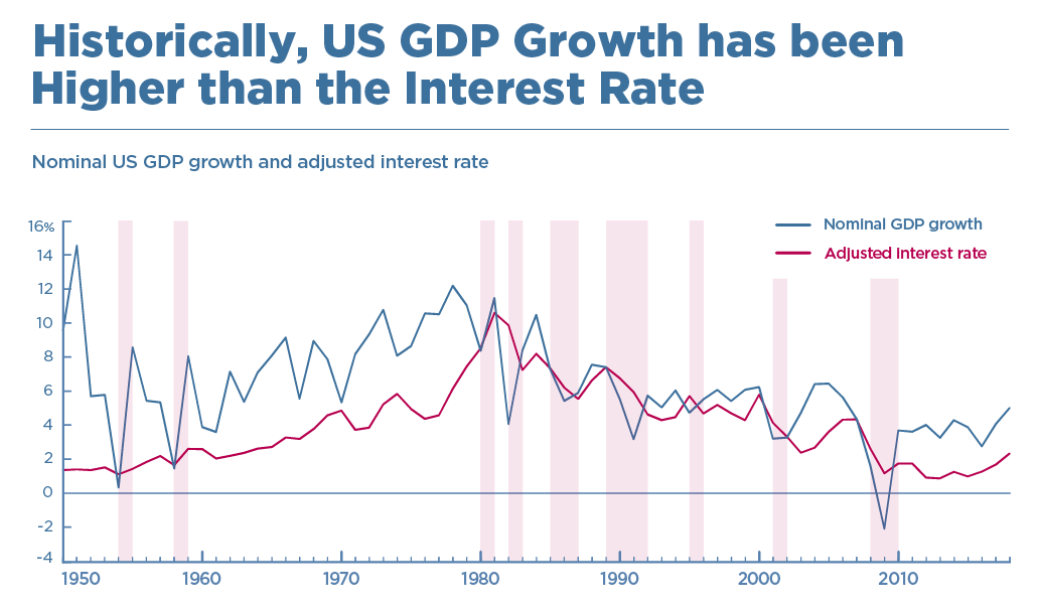

Historically, U.S. GDP growth has been higher than interest rates (both in nominal terms) even in periods of relatively high interest rates (the pink shaded areas are periods where GDP growth lagged adjusted interest rates).1

Economic activity simply means people at work. It does not mean profitable work and it requires as much energy when companies are suffering losses as when they are coining profits. World population is now 8 billion and is the healthiest and best educated in history. Politicians can interrupt progress but can’t really stop it. The world economy will keep growing and keep demanding more energy, and fossil fuels will remain the major source for decades to come.

The short term price fluctutions will affect short term stock prices as will interest rate levels, taxation policies, investor sentiment and a host of other factors but the relentless reality is that energy investors will benefit from the lack of capital going into the sector manifesting itself in higher prices, and management teams that now understand it is better to be profitable than to grow.

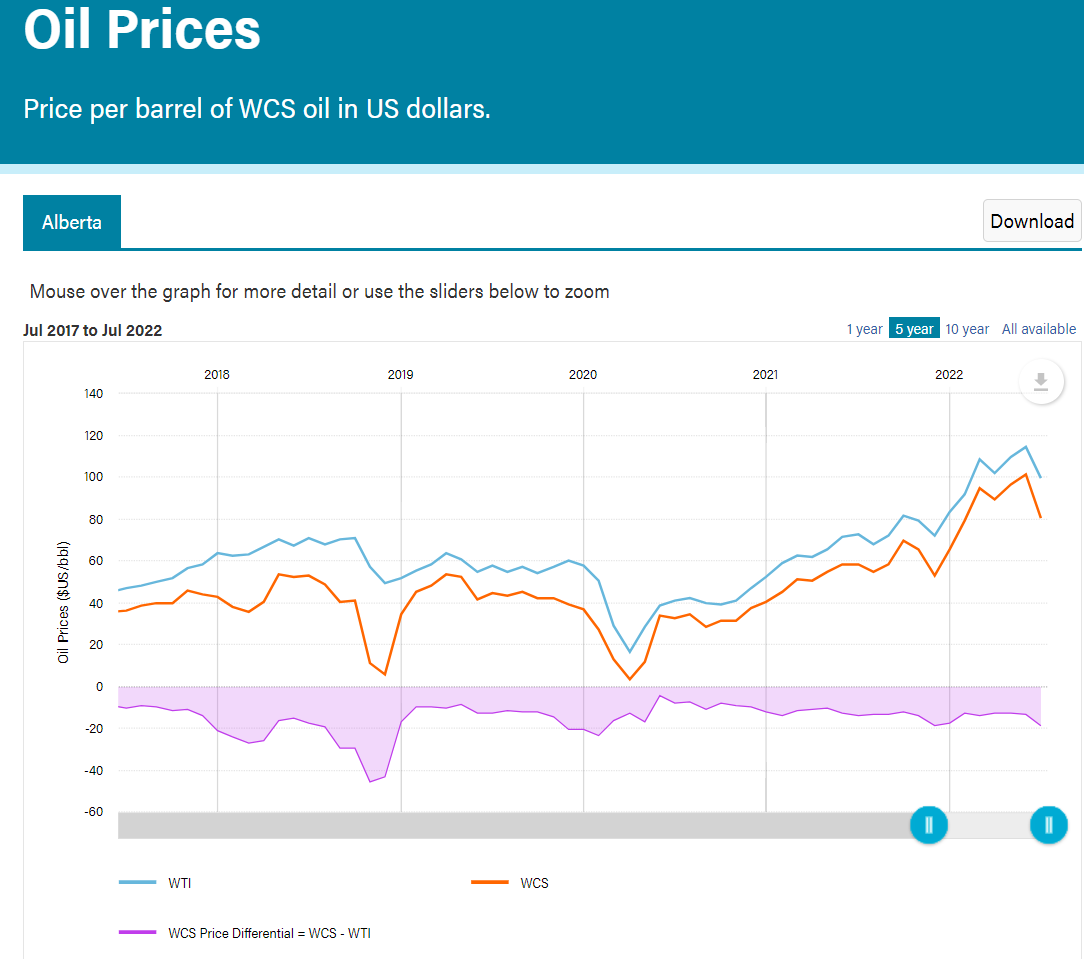

Investors typically over react to negative news. The recent declines in oil prices have many skittish but the price of Western Canada Select (in $US) must be seen in a historic context, and today’s price is relatively high and certainly high enough for Canadian producers to continue to enjoy robust cash flows.

Absent a material supply increase somewhere in the world, the oil prices received by Canadian producers should be more than sufficient to see them prosper. So I am hanging on to my oil stocks and adding on price dips. My holdings include Canadian Natural Resources (CNQ.TO) Cardinal (CJ.TO) Crescent Point (CPG.TO) Whitecap (WCP.TO) Bonterra (BNE.TO) Inplay (IPO.TO) Surge (SGY.TO) and Cenovus (CVE.TO).

Thank you Michael.i really appreciate you sharing your insights.