Intel is in a buying range and getting cheaper

Long term outlook for semiconductors is robust

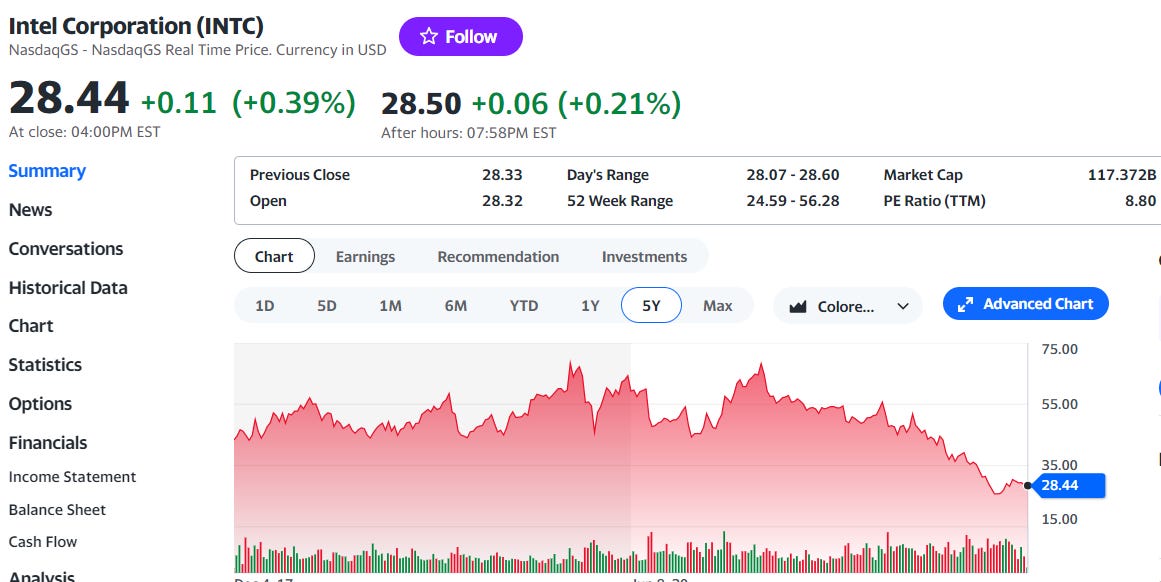

Intel Corporation (INTC) has had a rough year or two, with the shares falling by over 50% in a bit over one year and now trading at 8.8 times trailing twelve month earnings, shown on this chart from Yahoo.com.

Intel has been outgunned by nimble competitors like Advanced Micro Devices, NVidia and Taiwan Semiconductor who have focused on specific markets and leapfrogged Intel in driving their process technologies ahead of Intel. Intel has relied on its Windows franchise and chips for data servers, only to see competition from ARM based chips take some market share.

In the key x86 market for personal computers AMD has taken share from Intel over the past few years with cheaper chips and competitive performance. Statista reports the share trend in this chart.

Intel’s commanding share of the server market, estimated at over 90% in 2020, is being nibbled at by both ARM and AMD based processors. Intel shares remain under pressure and sentiment is negative.

Is it time to write off Intel as a core holding in semiconductors? Not in my opinion.

From a macroeconomic perspective, demand for semiconductors is likely to keep rising at a robust clip. Deloitte’s 2022 paper on the outlook for the $600 billion semiconductor industry is for sustained growth outpacing growth in the economy. Intel has embarked on a plan to expand its fabrication facilities building two new plants in Ohio estimated to cost $20 billion and begin operation in 2025. Intel has announced an ambitious program of process development, summarized by Intel as set out below:

With a global shortage of semiconductors today and likely to deepen in years to come, this program promises growth in sales and net income that I expect to exceed 15% annually for at least the next decade. Current revenues of ~$70 billion should more or less double twice in the decade reaching about $300 billion and net profit ratios of 15% (less than historic levels of 20 to 25% of sales) are a conservative expectation, so I foresee net income reaching the $45 billion level by 2032, or about $4.50 per share on 4 billion shares outstanding.

If that is anywhere close to reality (and I think it may prove conservative) Intel shares should trade in the $100 range within the decade, a compound rate of return of around 13% excluding dividends currently running at about 5% ($1.46 per share). That is a bit higher than valuation dean Aswath Damodaran calculates for Intel - Damodaran puts the cost of equity capital for Intel at 10.6% (the cost of capital is what the company pays and reciprocally is what investors get). Nobel prize winning economist Richard Thaler has demostrated that investors overreact to unfavorable news and under appreciate positive trends. In my opinion, the current market valuation of Intel undervalues the positive contribution of its capital expansion in a growing and undersupplied market.

Intel stock is in a buying range today in my opinion and may decline further if the expected U.S. recession materializes. I don’t hold any INTC shares at this time but expect to add them to my portfolio over the next year or sooner if the shares trade below $25.00 where I think they are a compelling value.

My biggest "fear" about Intel is that TSMC is going to start building in the US. And TSMC are really good in the foundry of Chips.

Time will tell, as always!

lol still cant believe you posted an article from 4 months ago to state the current state of things in the market.

Are you a time traveler?