How bad is it? That is the question I want American banks to answer

Higher rates will make it worse

Economist Nouriel Roubini has been pretty vocal pointing out the risks of a systemic problem in the American banking industry, reporting that Fed data show a “mark-to-market” loss on “hold to maturity” investments on bank balance sheets of more than US$600 billion in a system with total equity capital of US$2.2 trillion. Often called “Dr. Doom” for his catastrophe predictions of economic collapse, Roubini is dismissed by other economists. But his source, the Federal Deposit Insurance Corporation (FDIC) reports that unrealized losses of some US$620 billion do in fact exist, and some experts think that figure understates the problem which they say could be as great as US$1.7 trillion.

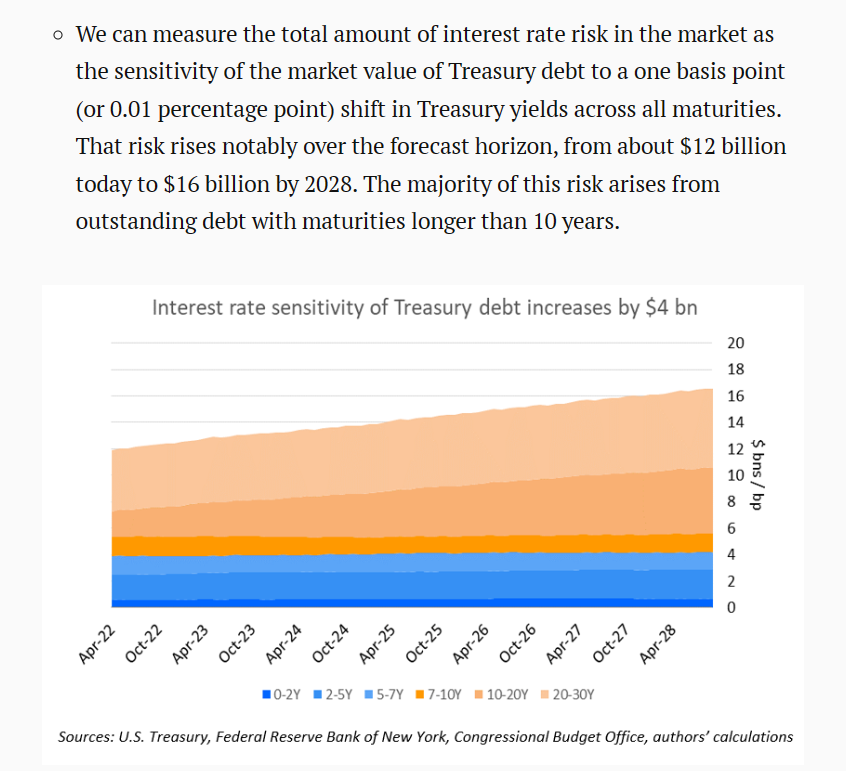

Whether the unrealized losses on U.S. treasuries is US$620 billion or US$1.7 trillion, it is a big number and in my opinion one which will grow. Rates have moved up sharply in the past year or so, from close to zero to as high as 4 or 5 percent for some maturities. The average interest rate paid on U.S. federal debt with a maturity longer than 10 years in December 2022 was about 1.8%, a rise from a negative rate of about -.4% in January of that year according to Treasury data; short term rates now run between 4% and 5% (data from the same source). The weighted average duration of outstanding U.S. federal debt is just over five years according to Brookings Institute. That short duration means a lot of debt must be refinanced every year. That same institution estimates the interest rate risk for a one basis point rise in rates at $4 billion.

Stated differently, for every full percentage point rise in interest rates the market value of outstanding U.S. treasuries falls by US$400 billion.

Who suffers that loss? Lots of people. Pension funds, the Fed itself, and U.S. banks which hold billions of dollars of “hold to maturity” bonds are at risk. For example, as of December 31, 2022 Bank America reported the mark-to-market unrealized loss on its “hold to maturity” portfolio was $114 billion (about half the bank’s equity capital)

Source: Copied from Bank America’s 2022 annual report

That US$114 billion unrealized loss resulted from the bank’s holdings (at cost) of US$867 billion of hold-to-maturity securities. Data on the duration of that portfolio are absent, but if you assume it was an average of 10 years with an average coupon of 1%, the 13.5% drop in market value corresponds to a rise in rates of 150 basis points to 2.5%. What happens if rates rise to 10% for 10 year treasuries? The value of that portfolio would drop to US$388 billion and the mark-to-market loss of US$479 billion would be double Bank America’s equity capital. In all likelihood the bank would fail despite its “too big to fail” status.

There are some 5,000 banks in United States and an analysis of each of them would be both time-consuming and tedious, but there is plenty of evidence that Roubini is right to warn of the risk. Think a 10% ten year rate on Treasury bonds is a bit extreme? It did happen quite quickly in the 1970’s when the ten-year bond rate ran up to over 14% in a short few years.

Source: Macrotrends

In 1976 the U.S. reported inflation rate of 4.9 percent was lower than today and only four years later it was in double digits. Talking heads on Bloomberg, CNBC, BNN and other financial news outlets keep prattling about the “terminal rate” and the “Fed pivot” just as they did in the 1970’s, as if the imperfect tools of monetary policy alone were enough to stem rising inflation and could be tweaked on a moment’s notice to change the course of the economy. Utter nonsense. Absent sensible fiscal policy the Fed’s efforts will fail and there is no hint of sensible fiscal policy coming out of Biden’s administration which keeps pouring gasoline on the inflation fire with rampant and relentless borrowing and nonsensical energy policies which will manifest themselves in higher energy prices (albeit with a lot of volatility) and fuel even worse inflation until the deepening shortage of fossil fuels is met with a supply response.

Biden has tried to intervene in energy markets by pillaging the Strategic Petroleum Reserve only to prompt OPEC to respond by cutting production recently by 1 million barrels a day. Stopgap measures like using up reserves just delay the problem and ultimately make it worse. We will see a repeat of the 1970’s and 1980’s over the next few years unless the electorate in United States, Europe, Australia and Canada get rid of the climate nutter socialists they were foolish enough to elect in the recent past and install sensible governments that deal with the real issues. CO2 is harmless but climate policies are toxic and will impoverish millions worldwide until voters change the direction of Western democracies. In the meantime, China, Russia, Africa and India will flourish by using cheap and reliable coal and oil and Western democracies will keep shooting themselves in the foot with climate-related stupidity.

I am not optimistic. The mass delusion caused by years of left wing propaganda has too many people buying into the climate charade and exhibiting lemming-like behaviour rushing towards the doomsday cliff - not doomsday caused by any global warming but one caused by institutonal stupidity.

I share your concerns. The other issue not talked about is the daily drain of deposits to money markets , credit unions, etc; the greed of the banks not changing what they pay to depositors will also haunt them.