High break-even prices threaten Canadian oils who have squandered capital on buybacks

Repayment of debt provides safety, buybacks add risk

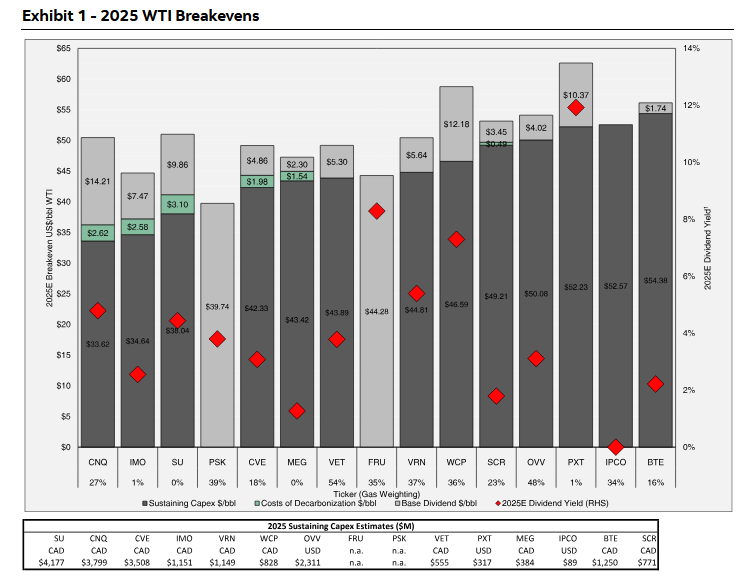

Scotia iTrade published its estimates of WTI prices needed for Canadian oil companies to “break-even”. The range of break-even prices is from about US$40 a barrel in the case of Prairie Sky (a royalty company) to US$60 a barrel in the case of Parex (which operates in Colombia). The break-even estimate is based on the price needed to generate enough cash flow to fund sustaining capital and current dividend payment rates.

Scotia goes on to project break-even WTI prices for 2026, which generally fall in the same range.

One can debate the assumptions but the analysis is robust enough to draw one key conclusion - if WTI falls to the $40 level in an economic downturn (which has happened more than once in recent years) heavily indebted companies like Baytex and Veren will need to cut capital outlays or curtail dividends, neither of which will be met with a cheerful market reception. In my opinion, MEG Energy investors will take a bath since Access Western Blend (AWB) sells at a deep discount to WTI and in an oversupplied market heavy oil producers that need the cash flow to keep up with debt repayments (e.g. Baytex) or meet social budgets (e.g. Saudi Arabia, Venezuela, Iran) will flood the market with heavy oil and AWB will fall further than WTI in percentage terms. In the Alice-in-Wonderland world of energy investment, investors rarely see low commodity prices as opportunity (which it is) and dump energy names hand over fist out of fear that is only warranted in cases where the company has too much debt.

Companies that will sail through a period of low commodity prices virtually unscathed are those that maintain pristine balance sheets and enjoy low operating costs. Those include Suncor, Canadian Natural Resources, Cenovus, Imperial Oil, Whitecap and the royalty companies Freehold and Prairie Sky. A market sell off is a chance to add to those names at bargain prices for long term holds.

Well-managed companies manage their reserves and balance sheets. Poorly managed companies try to manage their share price with nonsense like share repurchases, pretending they are valuation experts rather than petroleum engineers and CPA’s. It is easy to pick out which ones are better investments.

I've been through this show before and my average cost of my Oilco's is miniscule and although I wish I could just keep getting the dividends if they do sell off to ridiculous levels again I'll just increase my positions and sell the excess back to the market when it becomes rational again. Rinse repeat.

BTW, you do realize that the companies which you applaud (CNQ/SU/CVE/IMO) are ALL RETURNING 75-100% of their FCF to shareholders mostly via buybacks right? Yet you call MEG and other companies "poorly managed" LOL