Has Jerome Powell forgotten the Taylor Rule?

Or are political issues limiting his flexibility to raise rates?

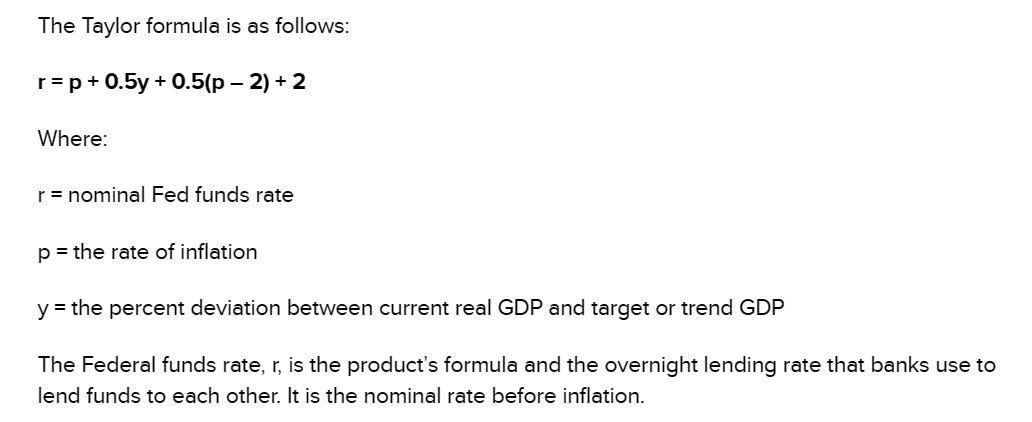

John Taylor was a Sanford economist who studied inflation and central bank interst rate policies, in 1993 coming up with the “Taylor Rule” as a systematic empirically derived guideline for monetary policy. The so-called Taylor Rule is a well-established and simple formula for determining what level of interest rates will achieve price stability in a market economy. Taylor argued that central bank discretionary approaches to interest rates led to boom and bust cycles. He was right.

Here is the rule:

The U.S. rate of inflation is about 5% today and current GDP growth is estimated at 1.1% by the U.S. Bureau of Economic Analysis versus a target GDP growth rate of 3-4%. Use 3%. The current Fed funds rate is between 4.5% and 4.75%. Call it 4.5% to make the point.

Applying the Taylor Rule, the Fed should be targeting a Fed funds rate of 9.5%.

r = 4.5 + 0.5 * 3 + 0.5(5-2) + 2 = 9.5%

Fed governor Powell doesn’t unilaterally set the Fed funds rate - the rate is set by the Fed governors as a group. They are under pressure from the Administration and the progressive Democrats to stop raising rates. On the evidence, it certainly appears that politics, not economics, are a major consideration in setting the Fed funds rate.

But, but, but inflation has declined from over 8% to about 5% . . . Isn’t that an argument for a pause in rate increases? Hasn’t that been the norm for central banks - to pause punitive rate rises when it is clear that inflation is abating?

Laughable really. As recently as 2015, Argentina’s rate of inflation had fallen to single digits and was declining rapidly. Under political pressure, the Argentine central bank eased its anti-inflation measures and cut interest rates from the 30% range to about 10% as they had done in 2014 only to see a resurgence of inflation that year. Higher rates take time to have effect, but lower rates have immediate consequences if consumer spending has been bridled by the higher rates and consumers have been struggling to make ends meet.

Inflation returned with a vengeance. Now Argentine has inflation running over 100%, a mere eight years later. Argentine’s “official inflation rate” is much lower since the Argentine government lies about it.

Central bank rates alone are not responsible for Argentine’s inflation problems but comprise virtually the only policy response to try a curb the rampant rise in prices. Argentine has excess government debt and leftist leadership. Sound familiar? Think Biden Administration. Sure Argentine has suffered a plunging currency, an abysmal balance of payments, and economic chaos. But those are the results of leftist policy, not the causes.

United States continues to be a strong economy with a strong currency and low unemployment and a manageable balance of payments1. Those strengths delay the inflationary pressures from taking hold but do not prevent them. They are results, not causes, and they are threatened by Democrat policies to keep borrowing, keep spending and pretend United States is immune to bad outcomes.

I hope they are right but I don’t see why they can’t be wrong.

Balance of Payments for United States (USABCAGDPBP6) | FRED | St. Louis Fed (stlouisfed.org)