Birchcliff Energy is strutting its stuff

Jeff Tonken is among the best E&P CEO's in Canada

Last November I wrote about Birchcliff Energy (BIR.TO) pointing out that CEO Jeff Tonken and his management team and board had decided to stop all hedging, hold production output level and pay down debt. I was impressed with the common sense of this strategy and wish others had emulated it. I initially bought 10,000 Birchcliff shares at an average cost of CAD$0.88 and have since added 60,000 shares at an average cost of CAD$4.78. The stock is now approaching CAD$10.00 a share and in my opinion CAD$20.00 is in sight.

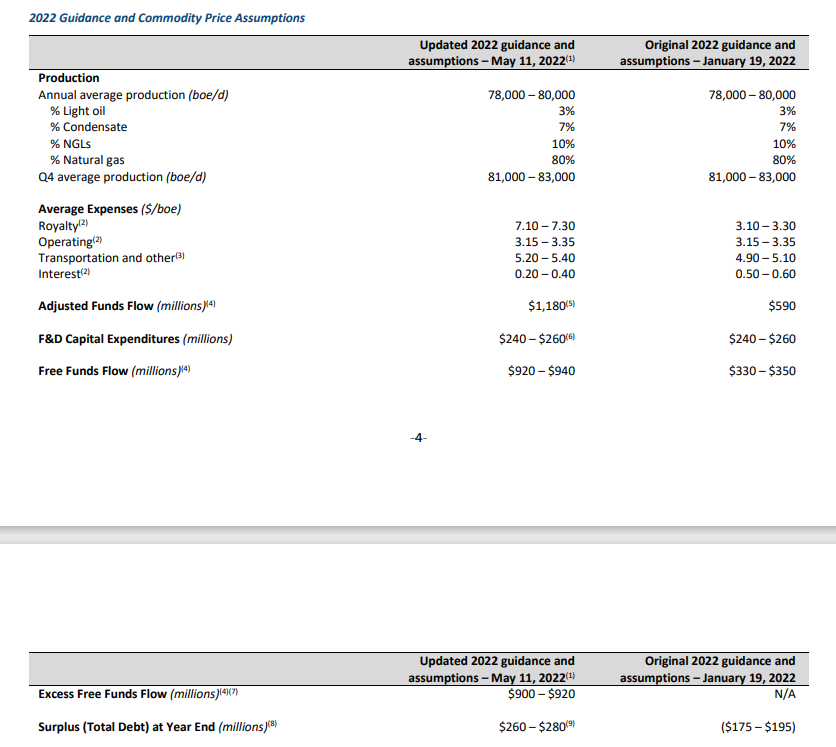

The unhedged strategy has paid off. While other E&P companies like ARC Resources (ARX.TO) are eating losses of hundreds of millions on their so-called “hedge book”, Birchcliff is raking in mountains of cash flow. As at March 31, 2022 Birchliff’s debt is down to CAD$408 million and the company expects to end this year with not debt and a cash balance of over CAD$250 million. Birchcliff updated its 2022 guidance with the Q1 report:

Projecting adjusted funds flow of CAD$1.18 billion for 2022 and keeping true to its CAD$240 to $260 million capital budget, Birchcliff is keeping its production relatively flat while building a fortress balance sheet. The company doubled its dividend with this report and is considering a 2023 dividend rate of at least $0.80 per share, well within its free cash flow.

The key factors in the success of an exploration and devlopment company are the quality of its resource base and the capability of its management to deal with the volatile commodity pricing world. Jeff Tonken seems to have mastered the latter and the Deep Basin acreage is among the most productive in the WCSB.

Valuation is more an art than a science and I don’t need to lecture anyone on modern valuation techniques like Black Scholes where you treat proven but undeveloped reserves as a “real option”. But a simple formula of 4X EBITDA adjusted for debt gets you an equity value for Birchcliff of ((4 x 1,180) +260 cash) divided by 266 million shares gets you ~CAD$19.00 a share and I (and others I am sure) will pay a premium for solid management and a clean balance sheet, so my view is that CAD$20 a share is in sight.

Birchcliff remains undervalued. I now hold 70,000 shares but will add to this holding over the coming weeks.