Birchcliff Energy is poised to fly

Birchcliff Energy is poised to fly

Unhedged with low costs in a surging natural gas market

Birchcliff Energy (BIR.TO) is a low cost natural gas producer operating in the Pouce Coupe and Gordondale sections of the prolific Montney basin of Northeastern Alberta. About a year ago, Birchcliff CEO Jeffrey Tonken made the bold decision to end “hedging” of natural gas prices betting that an emerging North American shortage of natural gas would see prices firm through 2021 and 2022. He couldn’t have had better timing. Many rival oil & gas producers have seen muted benefits from rising commodity prices and several have eaten very large losses on their “hedge book” as prices rose above their hedged price and they had to make up the difference to their hedging counterparty.

Since Tonken’s decision, natural gas prices have approximately doubled.

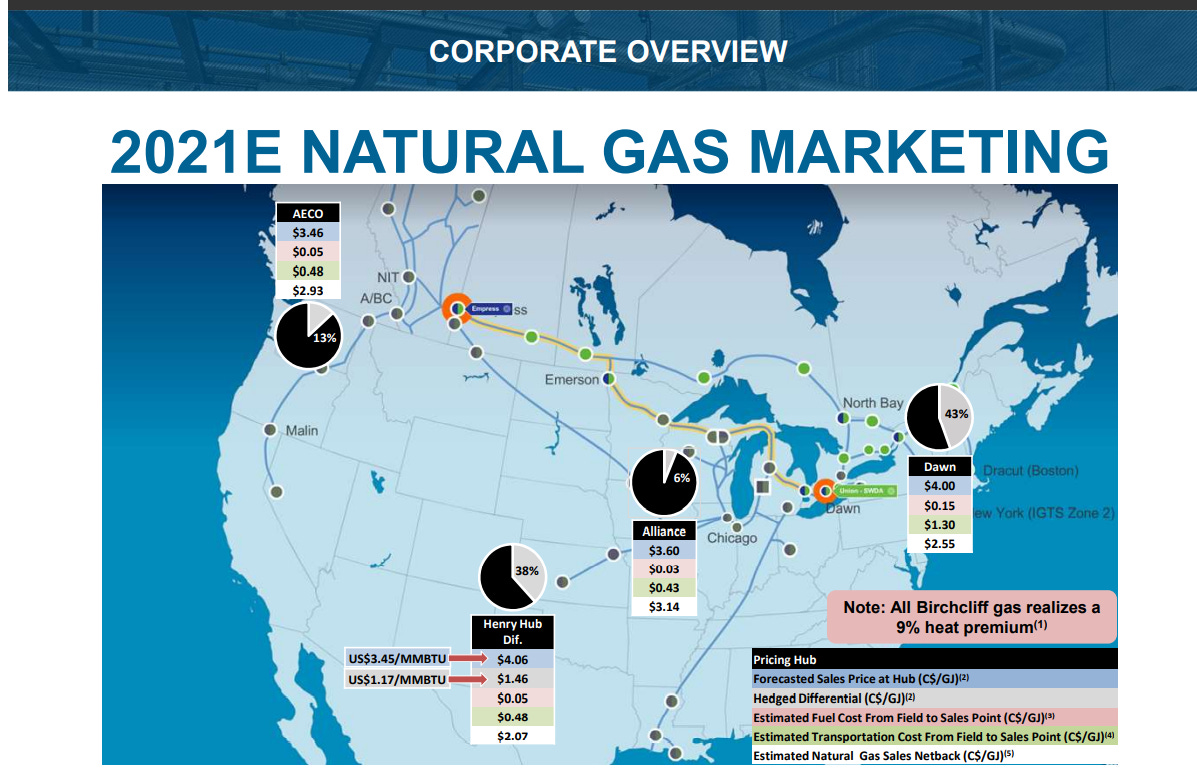

Birchcliff has diversified its markets for natural gas to avoid the egress issues that have plagued many Canadian producers, selling its gas into four main markets in Canada and the United States. U.S. market prices have tended to be higher than those in Canada, with Birchcliff on average receiving higher prices than many of its competitors.

In parallel, through ownership of its own processing facilities and improvements in drilling technology, Birchcliff enjoys very low costs. Since 2016, Birchcliff’s costs per thousand cubic feet of gas produced have averaged $1.75. The company produces approximately 80,000 Boe/day of oil & gas, some 80% of which is dry natural gas for which Birchcliff receives a 9% heat premium over the current gas price of approximately $5.45 per Mcf. That results in a gross margin of about 73% of natural gas sales.

Based on today’s natural gas, natural gas liquids and crude oil prices I estimate Birchcliff will earn cash flows of somewhere close to $700 million, enough to fund the company’s $230 million capital program and nominal dividend and leave free cash flow of about $450 million to repay debt. By year end 2022, Birchcliff should be debt free. I value Birchcliff at 5 times Earnings before Depreciation, Interest and Taxes resulting in an Enterprise Value of $3.5 billion. With debt gone and 265 million shares outstanding, I see Birchcliff shares having a value of somewhere in the $13 per share range, which compares to a current trading price of just over $7.00 per share.

A cold winter might see much higher natural gas prices and much higher cash flows for Birchcliff. Interesting, but investors are cautioned not to bet on the weather. Instead, Birchcliff shares should be seen as a reliable source of long term income despite the fact that today the company pays only a nominal dividend of $0.01 per quarter. With free cash flow expected to run in the $450 million range and debt on the way to zero, free cash flow of $1.70 per share by the end of next year would support a dividend of $1.20 while leaving well over $100 million a year for contingencies.

Birchcliff is not without risk. An economic downturn would reduce natural gas demand and could see both oil & gas prices suffer material declines. I am willing to bet that risk does not materialize any time soon and that by the time of any significant downturn Birchcliff will be a debt free entity generating free cash flow at even very low natural gas prices.

Birchcliff reports its Q3 results after the close on Wednesday, November 10, 2021. I own 55,000 shares of Birchcliff and will add more before those results are released, since I expect a strong showing.