Biden's policies contribute to the global energy shortage

Will surging power costs in Europe make electrical vehicles uneconomical?

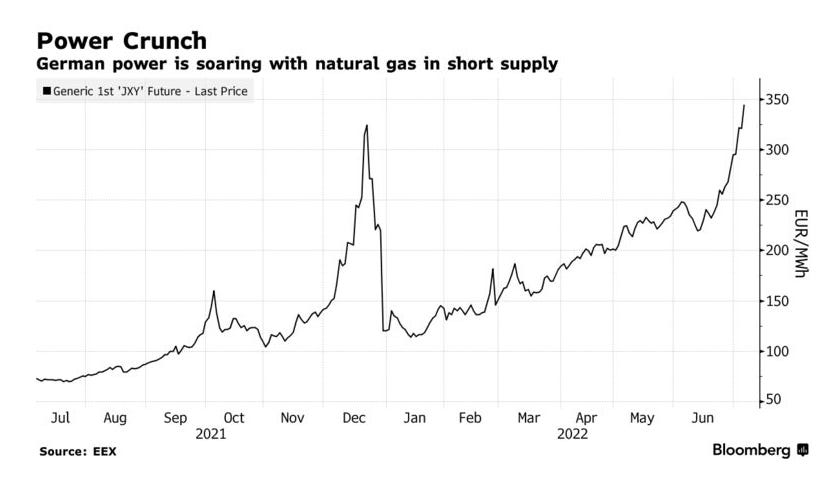

The left wing dream of a world powered by wind and solar with everyone driving an electric vehicle has moved from utopia to calamity in Europe and Joe Biden’s administration can share the blame. To set the stage for this discussion, consider the cost of electricity per Megawatt Hour in Germany and France, both poster children for the “green” revolution. Today, wholesale power costs in Germany have risen to 345.55 Euros per Megawatt Hour and in France to 398 Euros per Megawatt Hour, both all-time high prices.

Desperately short of natural gas to power its electricity generators, Germany is bringing back coal-fired power to keep the lights on.

German automaker Volkswagen has committed itself to a major push into electric vehicles (EV’s). The selling point has been both the “green” benefit of lower emissions (as if emissions were an issue, which is absurd since CO2 is harmless) and lower operating costs that offset the higher intital cost of an EV. The typical EV can travel 100 kilometers on 15 Kilowatt Hours of charge. Converting to Canadian dollars, 345.55 Euros is CAD$456 and 398 Euros is CAD$525, making the equivalent cost per hundred kilometers in an EV CAD$6.84 in Germany and CAD$7.88 in France.

My gas guzzling Mercedes cls450 burns about 8.7 litres of premium gas per 100 km and unleaded premium in Canada costs about CAD$2.15 per litre so my cost to drive 100 km is CAD$18.70. Despite the sharp rise in electricity costs, EV’s continue to enjoy lower operating costs than ICE vehicles in Europe. But the trend is not positive - the recent run up in electricity costs seems poised to continue as the European energy crisis deepens. If hydro costs double again in Europe (a distinct possibility) EV’s will be no cheaper to operate than ICE vehicles, and the demand for electricity they create will do nothing but put upward pressure on hydro rates.

Think this is a short term anomaly? Think again. The shortage of fossil fuels in Europe is at a crisis level and getting worse. Supplies from Russia are being constrained by geopolitics and sanctions for the Ukraine war, and European governments have been suppressing fossil fuel production driven by their insane delusion that CO2 causes climate change, an absurdity. The “green revolution” is on the cusp of becoming the “green nightmare”.

Natural gas prices in Europe and United Kingdom are now the equivalent of US$300 a barrel oil. Goldman Sachs projects a doubling of current natural gas prices in Europe in 2023.

So why is Joe Biden at fault? The United States is the only jurisdiction in the world which has the demonstrated capacity to rapidly increase oil & gas production and with a serious effort supported by policies that encourage hydrocarbon development, could close the fossil fuel supply gap in a short few years. But Biden won’t do that. To keep the support of his radical left wing base, most of whom share Alexandria Ocasio-Cortez’s obsession with the inane “climate change” narrative, Biden persists in policies that suppress American oil and gas development while paying lip service to the United States ability to supply LNG to United Kingdom and Europe.

In March 2022, Biden agreed that the U.S. will supply at least 15 billion cubic meters of LNG to Europe this year growing to 50 billion cubic meters by 2030. This commitment is more political show than reality since the U.S. LNG shipments to Europe were already greater than the amounts committed in the agreement for 2022. To really make a difference, the United States would have to rapidly expand both natural gas output and LNG terminal capacity.

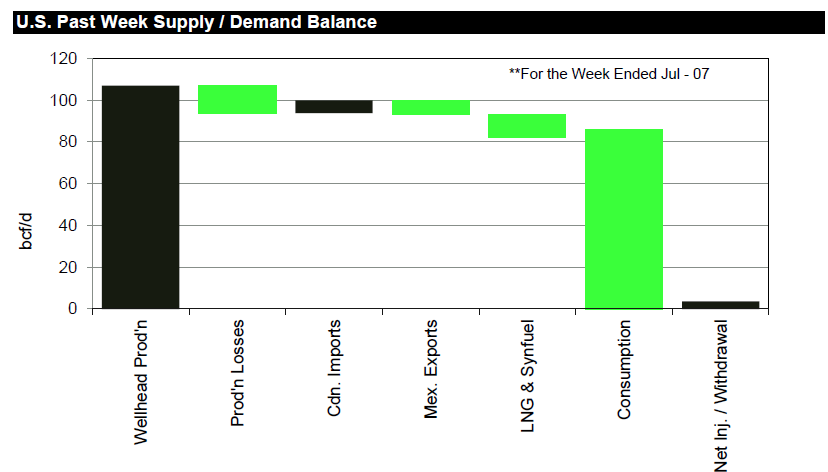

At existing production and LNG export rates, U.S. gas markets are roughly in balance right now with no excess capacity to ease the situation in Europe.

Source: TD Gas Line

United States natural gas production is running at about 97 Bcf/day and domestic demand is running at about 85 Bcf/day in summer months but winter demand will exceed production with draws from storage needed to balance the market. With imports from Canada less exports to Mexico and pre-agreement LNG exports to both Asia and Europe, the United States gas markets are in balance already and the U.S. will struggle to meet any additional commitment to Europe. Of course, it is possible the March agreement was merely an agreement to maintain the status quo and count existing LNG shipments to Europe in the commitment, making it an agreement to change nothing but political rhetoric.

To put it bluntly, Europe and the United Kingdom are in trouble and there is no relief in sight. Policy makers will have to abandon the “climate change” nonsense and take steps to increase their access to fossil fuels, or impoverish their citizens. They are already returning to coal, the fuel they typically vilify for its emission profile, and coal producers will benefit. Austria recently announced a return to coal. But coal won’t be enough. Nuclear expansion is decades away, renewables have been a costly experiment that today is a bad joke, and a return to fossil fuels is desperately needed. Given their evangelical obsession with their climate change narrative, European leaders are unlikely to move very quickly to deal with the looming crisis so investors should think carefully about how much damage the energy shortage will do to European manufacturers, distributors and retailers and protect their portfolios from the collapse of many European stocks vulnerable to higher energy prices. The tumbling dominoes of European and U.K bankruptcies caused by nosebleed energy prices is already in high gear. More will follow.

At the same time, smart money maintains its exposure to fossil fuel producers. A global shortage is a a tailwind for these companies who are already enjoying record profits in many cases.

I am developing strategies to short European market indices for some sectors while increasing my exposure to North American natural gas producers. Biden is not likely to retain power in 2024 and a shift to a Republican president seems possible and will prompt major shifts in policy driven by common sense rather than left wing ideology and gas producers should benefit. In the meantime, a pair trade of short European companies vulnerable to surging energy prices (Bulb Energy was the canary in the coal mine) and long oil & gas producers may pay off handsomely. Typical of left wing democracies, the failure of utilities is dumped in the laps of taxpayers, but energy intensive companies like aluminum producers, steel makers and glass manufacturers are at risk and may have to work it out in public markets.

This is a time for calm, caution and patience. Fossil fuel companies should benefit and there is a reasonable chance that demand for uranium will increase as those with the ability to increase nuclear powered electric stations do so. Uranium miners such as Cameco (CCO.TO) and late stage developers such as Denison (DML.TO) are likely to benefit materially.

What we need in the UK and Europe, is a short sharp shock - a really harsh severe winter lasting weeks of sub-zero temps (which automatically means no wind).

Such an event, would be enough to kill Net Zero once and for all!

It is a shame - a tragedy that people have to die & much misery & poverty has to be endured before the message is received & understood.

Pain & death may be the only language the political left understand, but sadly we all have to suffer, whilst our political class are largely immune from the detrimental effects of their self-serving decisions.

Michael Thankyou for your thoughtful writings. I am in Australia and my largest holdings are thermal coal exporters to Japan Taiwan and Korea mainly asx listed whc and nhc the free cash flow yields are extraordinary with the market pricing a very low terminal value . Whc reports quarterly on Monday