ARC Resources is undervalued

Management can surface the value by altering course

With the acquisition of Seven Generations, ARC Resources (ARX.TO) transformed itself into a natural gas and condensate powerhouse with a suite of assets in the Montney rivaled only by Tourmaline (TOU.TO) and Canadian Natural Resources (CNQ.TO). Despite criticism for taking on the acquisition debt at the time, ARC management should be recognized for their wisdom in seeing the natural fit of Seven Generations and the flawless execution of the combination.

At the time, to protect against an unforeseen but calamitous plunge in commodity pricds, ARC not only assumed Seven Generations’ hedge book but seems to have added its own hedges. The nature of the hedges is often referred to as “costless collars” where the company buys puts and writes calls with the premium received from writing calls offsets the premium paid for the puts. ARC can deliver physical gas or oil or condensate against the respective call options if called, so the risk of actual loss on the collars is limited.

But actual loss omits opportunity cost. The premium received for the calls written is small in relation to the risk of higher commodity prices with both actual and opportunity losses possible or even likely. Commodity risk is not only downside risk but upside risk, and the probability of either is quantifiable. For readers who are family with Black Scholes (B-S) and option valuation, the Delta1 metric is a measure of the probability a call will be exercised at the given strike, and by running the B-S calculation at arbitrarily higher and arbitrarily lower strike prices, you can develop a probability distribution of likely outcomes. You can do the same with the purchased puts. Management can formally and reliably assess the risk-reward of their hedging program and in my opinion should do so.

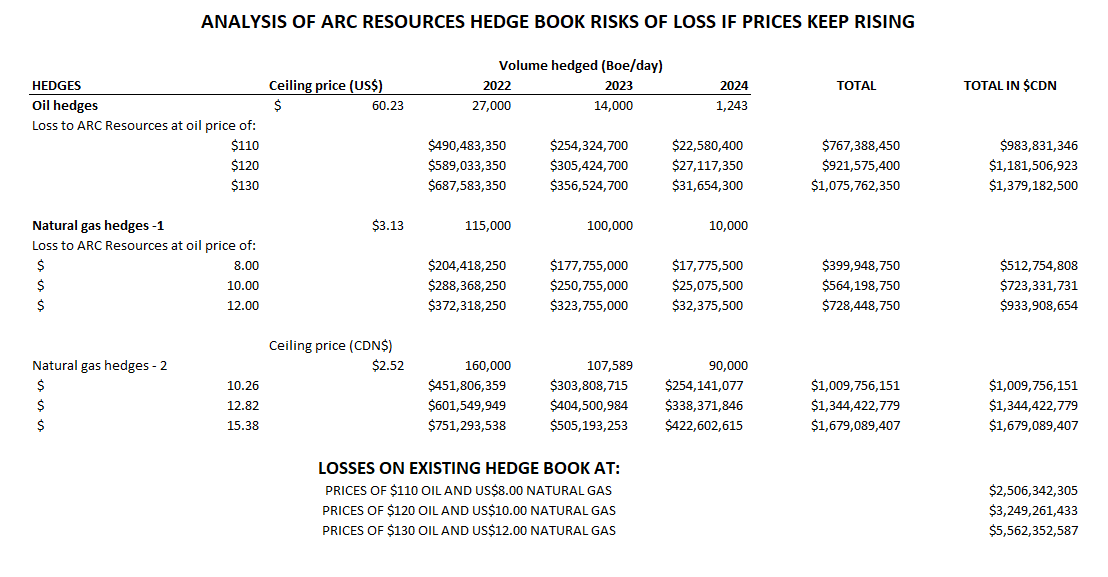

I prepared a spreadsheet of the ARC hedge book as at Q1 2022 and a sensitivity analysis of the opportunity costs of the written calls. The picture shows potential opportunity losses of CAD$2.5 to CAD$5 billion based on oil prices from CAD$110 to CAD$130 and natural gas prices from CAD$8 to CAD$12 per Mcf.

To be clear, ARC will not lose money on its “hedges” but will leave money on the table if prices rise to these levels. They already have.

To put the program into perspective, I have prepared a comparison of Q1 results as released and pro forma to without any hedges at all. Pre-tax income would have been 217% greater without the written calls. The put premiums would have been absorbed (not included in the pro forma) and ARC would have had all the protection its directors deemed warranted and been a much more profitable company.

Let me be clear. The decision to enter risk management contracts by buying “puts” was a board decision and cannot be faulted ex post simply because the risk did not materialize. But the decision to use “costless collars” was in fact very costly and unnecessary. The only benefit was the call premia received and that was not disclosed but I am certain it was a tiny fraction of CAD$827,500,000.

Options are traded on the CME, which provides useful tools for assessing risks on options including B-S calculators. Using today’s values, I quickly calculated the B-S value of a call option on oil at US$121 a barrel with a term ending December 2022. The option has a premium of US$6.52 a barrel and that is what a risk manager receives for writing the call. The Delta of .35 tells you there is a 35% chance the option will be excercised.

That merits some thought. Goldman Sachs thinks Brent oil will average US$135 this year and WTI follows Brent at a discount. With WTI now at US$115, to average US$130 (Brent less $5.00) WTI will have to average at least US$145 for the second half of 2022. The possible loss on the US$121 call is US$24 a barrel offset by the $6.52 premium. On 100,000 barrels a day for the balance of 2022 a call option at $US121 (above today’s market and therefore seductive for risk managers) will result in a loss of about US$440 million (offset by premiums received of about US$140 million) if Goldman is right.

With a global oil shortage and no supply response in sight, there is no reason to believe that Goldman is wrong or to believe the is little risk of a rise in oil prices to very high levels later this year - I see US$200 as a tail risk not out of the question.

There is also a risk of a price collapse if the world enters a deep recession. The issue for risk managers is to handicap that possibility and estimate how much “insurance” is needed, if any, to mitigate that risk. If ARC’s balance sheet can stand oil at US$63 a barrel (the ceiling price they agreed to in their current hedges, so presumably they are satisfied with that price), buying Puts at a US$63 strike is enough to protect their balance sheet. Those puts are relatively cheap today since they are over US$50 out of the money. They are also at a higher strike than the current portfolio of puts ARC holds.

My conclusion is that ARC’s “hedging” is a disease devoid of common sense. I hold no ARX stock today despite my deep admiration for its operating management and world class assets.

Delta is a proxy for the risk of the option being “in the money”. The actual risk is the first derivative of the option price with respect to strike, but the Delta metric is a reasonable proxy.

Mr Blair: An excellent write up. You would think that management would have engaged an options professional to develop a better strategy...or even easier, they could have call you.

Thank you.