2024 will be a tough year for investors

Irrational exuberance will end in tears

The Standard and Poor’s 500 stock index and its ETF counterpart demonstrate significant overvaluation. At its current price of $450 SPY is trading at about 23 times earnings and pays a dividend of 1.56% according to data from Yahoo.com Finance. The U.S. government projects 2024 growth at 2.1%. Would you pay 24 times earnings for an economic entity growing at 2.1%? Not me.

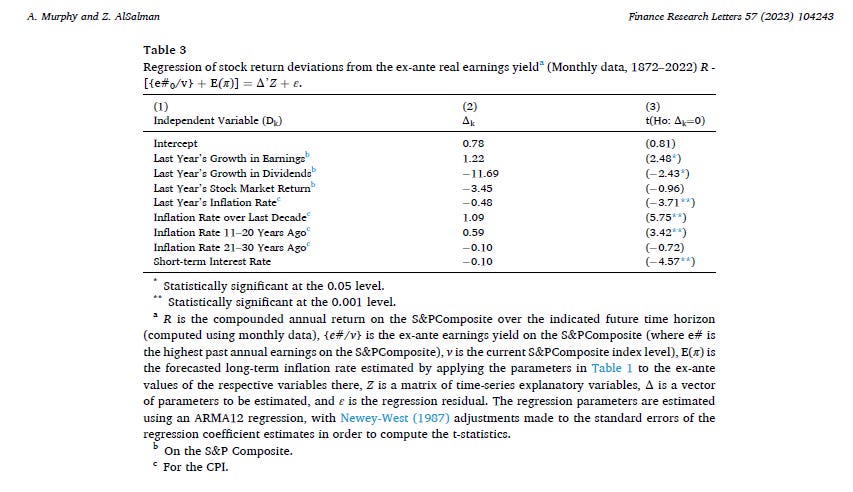

In an excellent recent paper1, Austin Murphy and Zeina ElSalman explored the relationship real stock market returns, inflation and future index returns.

They argue that contractionary monetary policy is responsible in part for the decline in the market indices in subequent years which (while little more than common sense) is supported by the empirical data they examined over 150 years. Rates above the rate of inflation both lower the rate of economic growth (and profit) growth while increasing the discount rate for valuation of business entities. The Fed’s current policy rate is 5.25% to 5.5% and the inflation rate is now running at about 3.9% according to the Department of Labor.

In this environment, the likelihood of a sharp market decline is higher than normal. In my lifetime, the old “rule of thumb” was that the price to earnings multiple of the market should approximate 20 less the rate of inflation. That would be about 16 times today but SPY is trading at closer to 24 times.

For the SPY, which in many respect mirrors the U.S. economy, a valuation of the SPY as if it were a single entity using the Gordon Dividend Growth Model would yield a value somewhere around $375 yet the SPY is trading at $428. Something is likely to give. Here is that valuation using a 9% desired rate of return (about what the S&P has returned for decades) and a 3% real economic growth rate with 4% inflation (7% nominal growth).

SPY Value = dividend of $7.50 (increased over 2023 by the nominal expected growth of 7%) divided by (9 percent required return less 7% nominal growth rate) = $375

Higher growth would result in a higher valuation as would lower inflation while a higher required return to compensate for risk would lower valuation. In my view, the former are unlikely to materialize and the latter is my expectation given the uncertain environment. If anything, SPY should trade below $375 but with the obvious imperfections in the data, my call is for a year end value of SPY of $400 and for the S&P index of 4,000.

The rapid introduction of artificial intelligence (AI), an election year replete with government handouts to buy votes, and falling commodity prices are market tailwinds while monetary constraint, geopolitics and massive government debt and deficits are headwinds, so the data are far from perfect. AI promises higher productivity but that will take time and the hype borders on “irrational exuberance” which is reflected in SPY over valuation today.

In my opinion, for what that is worth, it is a time for caution.

Relationships between stock returns and real earnings yields over the last 150 years, Murphy and ElSalman, Finance Research Letters 57 (2023) 104243

Is the S&P at 4000 really a cause for tears? I have seen much worse.

Liked better your article on seeking alpha. Very well done.