Will MEG Energy break out in 2024?

A lot depends on TMX and whether it breaks out to the upside or downside

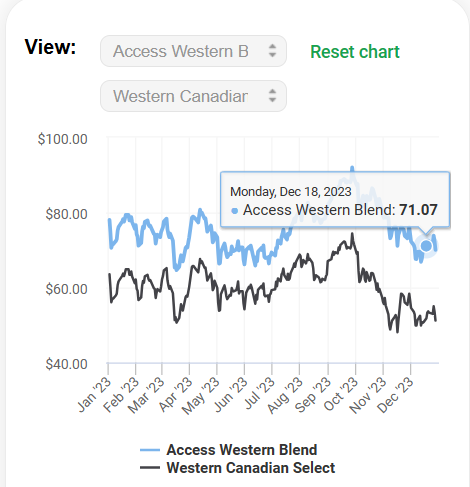

MEG Energy has made great progress delevering its balance sheet and enters 2024 in the best financial position in a decade. Many investors are confused by the company’s reporting since MEG sells Access Western Blend (AWB) yet most analysts focus on Western Canada Select (WCS), a related blend but not precisely what MEG sells to its customers.

AWB has traded at a premium to WCS throughout 2023. In mid-December AWB changed hands at about US$71 a barrel. With the Canadian dollar at about $0.75 U.S. the Canadian price of AWB comes out to about CDN$95 a barrel, more or less what is was in the first quarter of 2023.

That is not the end of the analysis since both AWB and WCS realize a price in Canada at a discount of about US$18 a barrel which is expected to shrink to about US$14 a barrel once TMX is onstream. That narrowing differential is important to the value of MEG shares. [US$18 a barrel is about CDN$24 a barrel].

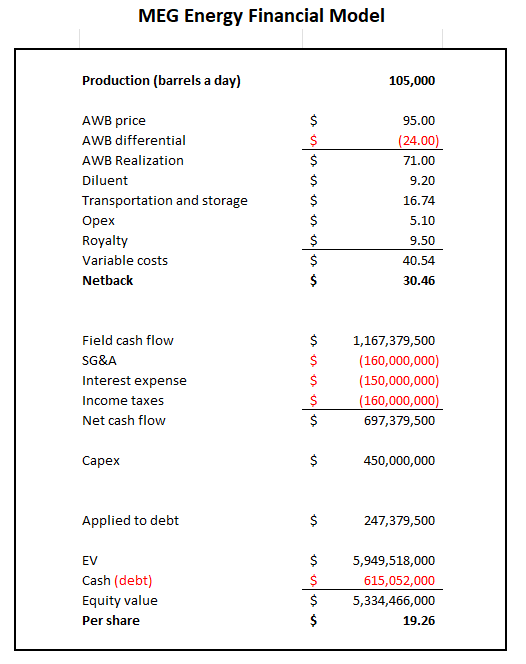

A simplified model of MEG using a valuation metric of 4 X EBITDA and based on a CDN$450 million capital budget with output averaging 105,000 barrels a day puts a value on MEG shares of about CDN$19 a share - a bit less than where they trade today

With TMX up and running and no increase in expected tolls arising from the cost overruns and lengthy delay, the differential in Canadian funds shrinks to $18.60 and the same model returns a value of CDN$23 a share for MEG, more or less today’s trading price. I presume the market is discounting the completion of TMX on time (end of Q1 2024) and perhaps applying a higher than 4 x EBITDA multiple given the absence of exploration risk.

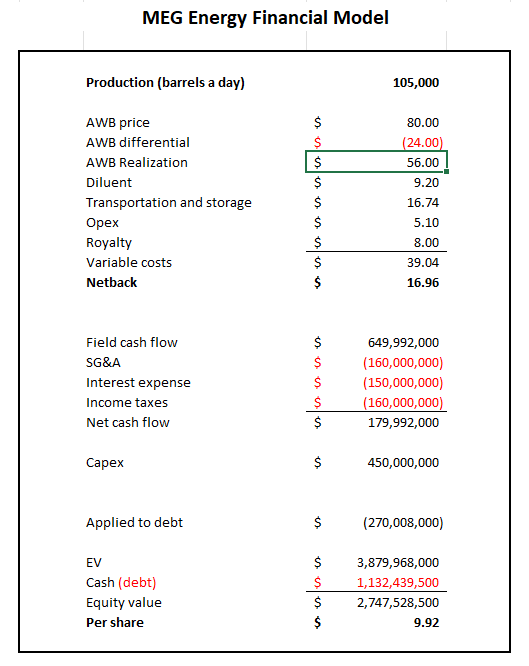

But what happens if TMX is not completed as planned and, worse, if world oil prices fall and AWB trades at CDN$80 a share? That picture is not quite as pretty with the value of a MEG share (based on the same metrics) falling to under CDN$10 a share.

Like all models, this one is susceptible to errors and there are a lot of factors not considered in the basic arithmetic. Think of the analysis as a sensitivity test rather than a valuation. The point is that for MEG shares to generate returns that many analysts seem to expect with so-called “target prices” in the range of CDN$30 a share.

On December 20, 2023 TD Waterhouse reduced its commodity price outlook by $5 a barrel and reduced its “target price” for MEG shares to CDN$28 from CDN$30.

To me, that remains aggressive in a volatile commodity price environment in a market which in aggregate is over valued by historic standards. I would be cautious about energy investments in 2024 and in particular about a bullish stand on MEG despite its excellent assets. I had a short position in MEG which I closed before year end, and I expect I will re-open a similar position in the first quarter if oil falls. However, if oil prices firm (as many expect) in 2024, MEG will be a big winner.

Place your bets.

Excellent article. Dr. Blair makes kalkulations based on his knowledge of finance and figures not just guesses based on other people's comments on Twitter. Always be more careful than optimistic.