Will associated gas be the downfall of the U.S. natural gas industry?

Unlikely. If La Nina occurs as meteorologists predict, winter 2024 shortages are likely and should see higher prices

Oil wells throw off natural gas called “associated gas”. In 2019, associated gas comprised an estimated 15 Bcf/day of total U.S. gas production of about 92 Bcf/day. Associated gas is typically “wet gas” containing natural gas liquids such as butane, propane, and C5’s which require processing.

The Permian Basin has been the most prolific oil play in the U.S. and is the largest source of associated gas, growing in lock-step with Permian oil output. In 2019, associated gas comprised about 16% of total U.S. natural gas production while U.S. oil output in 2019 was 12.4 million barrels a day.

Fast forward to 2024. U.S. oil production is forecast to reach 12.8 million barrels a day, slightly higher than in 2019, owing primarily to slowing output in the Permian basin. Some analysts expect U.S. oil output to “flatline” in 2024 and resume growth in 2025.

If so, associated gas should not by itself create a glut of natural gas this year, certainly not in time to cause oversupply for the winter of 2024-2025. Associated gas growth rolled over in 2020 in the main oil producing regions according to the Energy Information Administration (EIA), comprising less than half of the total gas output of the oil producing regions, falling about 4% in 2020 and not changing much thereafter.

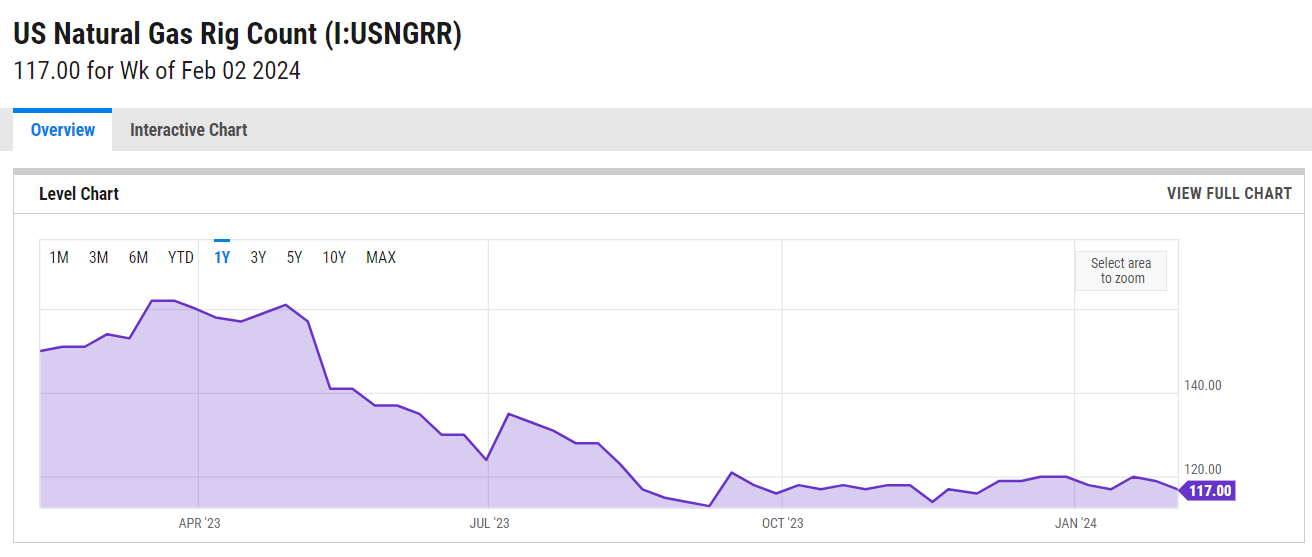

The EIA forecasts 2024 natural gas production in the U.S. at about 105 Bcf/day. Demand hit a high of 118 Bcf/day in the recent cold snap with about 13 Bcf/day of that demand made up of LNG withdrawals for export abroad and pipeline exports to Mexico. Despite the relatively high demand, the U.S. natural gas rig count has fallen sharply in the past year (although rig productivity has risen).

U.S. LNG production continues to grow despite the recent embargo on new permits by the Biden Administration (certain to be repealed if Trump re-enters the White House in early 2025). U.S. LNG exports are expected to rise this year and next adding over 2 Bcf/day of demand ovet the next year.

This confluence of factors points to a resurgence in profitability of natural gas producers this fall and through the winter starting this December. Those factors are:

Less growth in associated gas

Fewer gas rigs in the field

Higher LNG exports

La Nina expected by the fall leading to a cold winter.

It is always dangerous to make predictions, particularly in commodity markets. Nonetheless, I am betting on Canadian natural gas producers to benefit from a likely U.S. shortage just as the first Canadian LNG facility in Kitimat B.C. comes onstream and the result manifests itself in higher prices for Canadian gas. If this does happen (and there is no guarantee it will) then Canadian companies like Tourmaline Oil (TOU), ARC Resources (ARX), Peyto Exploration & Development (PEY), Birchcliff Energy (BIR), NuVista Energy (NVA), Spartan Delta (SDE), Pine Cliff (PNE), and Advantage Oil & Gas (AAV) should have a field day.

I have placed my bets on Birchcliff, Peyto, Spartan Delta, and Pine Cliff and opened a sizeable short position on Advantage in case I am wrong. If gas prices tank this summer, I expect them to drag Advantage down with them (and all of the other stocks as well) and gains on the AAV short will provide cash to increase my bets on my long positions.

I have avoided ARX which I consider to be badly managed and squandering free cash flow buying back stock which in 2023 resulted in higher debt. ARX projects a decline in production in 2024 and I estimate the value of ARC shares at about CDN$17.00 a share. The sizzle on the steak for winter 2024 will be dry gas in my opinion since I do not foresee much rise in condensate prices, a material part of ARC’s output.