Who gets hurt if energy prices tank?

Hard data make it easier to plan for a downturn and to react should one occur

I have seen articles on Bloomberg making the case that economic growth may falter and a surplus of oil & gas result which could see sharply lower prices. Reality is we don’t know, but we can plan our portfolios for the possibility that they might and do some hard analysis of what effect sharply lower oil, gas and condensate prices may have on Canadian exploration and production companies.

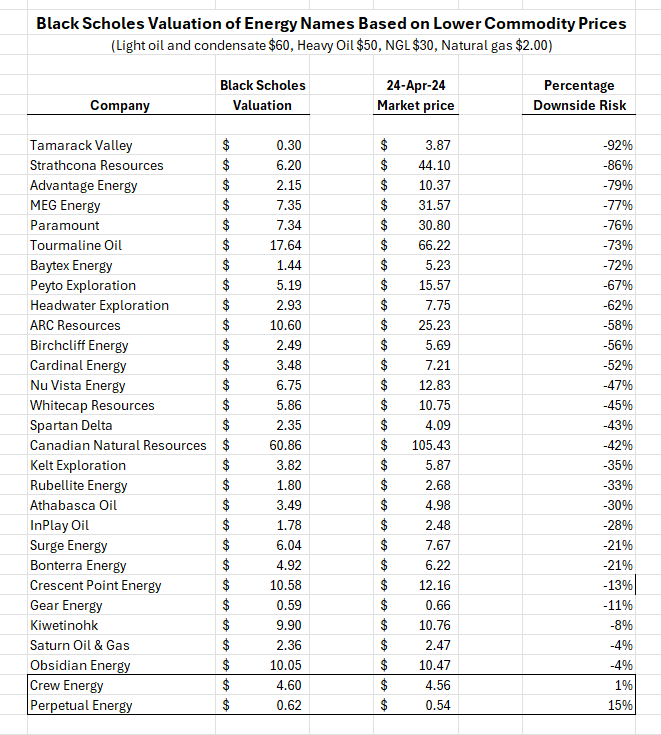

I have done a comprehensive analysis of the companies I follow using a Black Scholes model of their reserves as an option and the following commodity prices as if they were as of today, all in Canadian funds:

Light oil - $60 a barrel

Heavy oil - $50 a barrel

Condensate - $60 a barrel

NGL - $30 a barrel

Natural gas - $2.00 a gigajoule

I have ignored hedge books in this analysis since they are relatively short term and this analysis looks beyond the hedge book horizon.

As set out in the table below, only two Canadian companies valuation is unharmed by lower commodity prices - Crew Energy and Perpetual Energy. It may seem obvious but these two names are so undervalued in today’s market trading that even a significant drop in commodity prices to the assumed levels would not lower their intrinsic value below today’s trading price.

Of the balance, twelve popular names would see a drop in intrinsic value from today’s market price of over 50% and six names a drop of over 70%. The valuation of these companies by the market today is predicated on commodity prices at or above today’s levels and they are quite vulnerable to a sell off in oil & gas triggered by a recession or other event such as the recent pandemic.

Names at the bottom of the list are already discounting adverse conditions and pose less risk.

The assumed prices are harsh in the oil space where current prices are between $80 and $110 per barrel for oil & condensate and the drop assumed is steep. In the natural gas space, the assumed $2.00 per gigajoule is actually higher than today’s AECO price of about $1.20 a gigajoule as we enter the head and shoulders period but well below so-called “strip” pricing for natural gas and the forward futures prices on the CME.

I am not predicting a collapse in oil & gas prices nor do I believe one is imminent. This analysis is useful for building a resilient portfolio that recognizes the degree to which commodity prices affect intrinsic value of the companies listed and weights holdings according to the degree of risk.

My large holdings are Peyto, Birchcliff, Bonterra, Whitecap, Spartan Delta, Rubellite, Saturn and Perpetual Energy. None of them would fall below my adjusted cost base in the event of a downturn that saw their trading prices fall to the levels set out in the chart. I would see such a downturn as an opportunity to increase my holdings.

Michael, there is very little available research on Perpetual Energy. Aside from its price, can you tell me why you like it?