Whitecap ticks a lot of boxes

Hedging disease caps gains

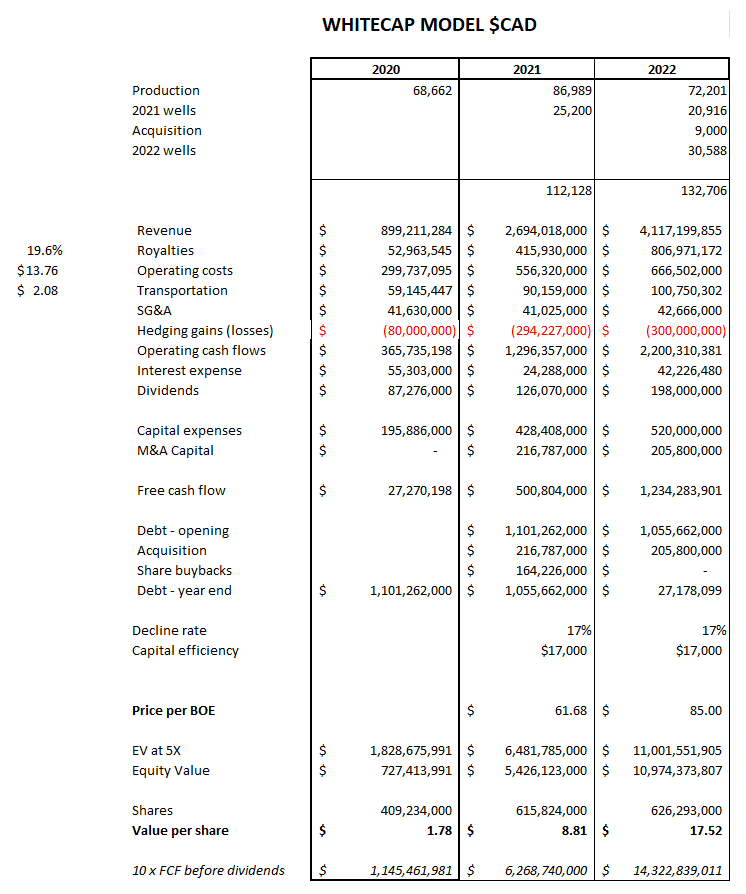

Whitecap Resources (WCP.TO) is a long time favourite of mine with top drawer management and timely acquisitions. Like some of its peers, the company has contracted the “hedging” disease that caps the potential benefit of higher commodity prices by selling calls in addition to buying puts to protect against price collapse. The puts make sense but the calls provide little value and become liabilities when commodity prices rise above the strike price of the calls. Whitecap booked “hedging” losses of almost CAD$300 million in 2021 and I expect at least that amount of lost opportunity in 2022.

Having said that, Whitecap’s excellent asset base is generating a lot of cash and should all but eliminate any debt this year while paying a decent dividend. I model operating cash flow of CAD$2.2 billion which should be enough to fund the company’s CAD$520 million capital program, pay about CAD$200 million in dividends, and retire debt that was $CAD1.1 billion at 2021 year end.

Considering the company’s size and strong balance sheet, I put a value of five times EBITDA on the company which by year end 2022 amounts to CAD$17.50 a share, substantially higher than the current trading price of CAD$10.00.

I hold 15,000 shares.

WCP is in my portfolio too and not looking to sell. Mike, what are your thoughts on Saturn Oil & Gas (SOIL)? It's Oxbow purchase seems terrific but they are bogged down by hedges even into 2023.