Where is the action in battery metals?

Spoiler alert - it is not in lithium

Joe Biden’s government just made a commitment to Lithium Americas to provide US$2.26 billion in financing for its construction of a lithium refinery at its Thacker Pass mine in Nevada. Like most Biden initiatives, it is poorly targeted at lithium which an also-ran in the shortage of key metals for batteries to be used in electric vehicles (EV’s). No doubt the Biden administration wants all the brownie points it can get before the November election and a loan to expand domestic lithium output is in many ways sensible since most of the world’s lithium is currently produced in Australia, Chile and China and relatively little in the domestic United States. The Thacker Pass output is expected to provide enough lithium to support production of 800,000 EV’s. The U.S. light vehicle market has annual demand for about 17 million vehicles. The Biden support for Lithium Americas is spit in the ocean, more performative than substantive.

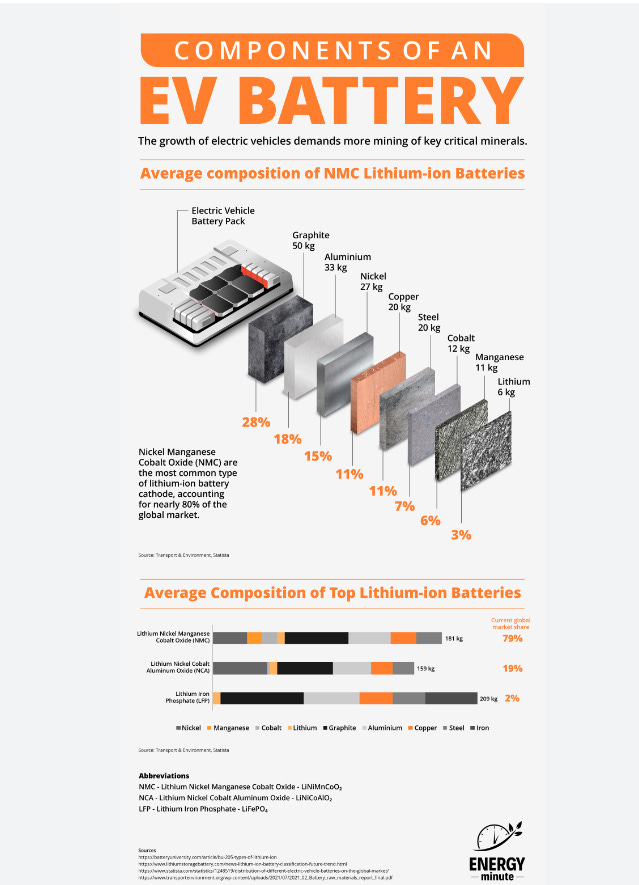

The real action in EV batteries is graphite, aluminum, nickel and copper. The United States produce virtually no graphite. China produces 65% of the world’s graphite, followed by Madagascar, Mozambique, Brazil and Russia. Canada is a small graphite producer. Any EV batteries produced in North America will rely on imported graphite from jurisdictions not all that friendly to United States or Canada.

There is currently a world surplus of aluminum and, while that may change, it is not a gating factor on EV production for the near term.

Likewise, with significant growth in nickel output in Indonesia and China, there is a current surplus of nickel worldwide. Longer term, it seems likely to turn to deficit if EV’s catch on.

Copper is a significant problem for the climate nutters who think there will be an energy revolution with widespread adoption of EV’s. There is about three times as much copper in every EV than in a typical internal combustion engine (ICE) vehicle, and demand for copper for wiring, transformers, switchgear, and many other electrical applications keeps growing in line with global economic growth. Slower growth in China points to a copper market in surplus for the next few years but long term scarcity is in the cards. Cumbersome permitting regulations in both United States and Canada make it difficult to get a new mine permitted within one or two decades, with major deposits such as the Pebble deposit held by Northern Dynasty Mines and the Prosperity deposit held by Taseko Mines (both world class deposits in size, scale and grade) have been stalled or stopped by environmentalists based on a host of complaints about the effect on fish population or endangered species. If the claim that CO2 causes climate change were valid (fortunately it is not) the only endangered species that would be at risk is humanity, a risk exacerbated by the delays in permitting these large mines.

Most of the world’s copper comes from third world countries such as Chile, Peru and Panama, and while Chile and Peru are quite mining friendly, the massive Cobre Panama mine operated by First Quantum has been put on care and maintenance after the mining license was revoked by the Panamanian government and the mine ordered closed, curbing output of about 660 million pounds of copper. World primary and secondary (i.e. recycled) copper output is about 55 billion pounds per year. If 30% of world car production of about 70 million light vehicles a year were EV’s, the EV market alone would demand about 3 billion pounds of copper and with few new mines expected to enter production over the next decade and output of existing mines in decline, a severe shortage of copper seems inevitable.

Global copper demand is projected to grow 20% by 2030 raching 30 million metric tonnes a year (66 billion pounds) and there is little doubt that existing mines cannot meet that demand even with a portion of that demand satisfied by extensive recycling. Higher copper prices and shorter permitting times are needed to meet the demand or the “EV revolution” will stall out, which I see as the likely outcome.

To my mind, it is absurd that the Biden administration pours billions into lithium while stalling the permitting of the Pebble deposit which could produce as much as 6.4 billion pounds of copper over the next 20 years, going a long way to ease the expected shortage. The dichotomy between pouring money into Lithium Americas while stifling the Pebble mine’s progress is typical of leftist politicians - what they really want is headlines that support a saleable story, not actual progress.

Environment Canada’s denial of a permit for the Prosperity mine is has a similar odour to it. Trudeau’s Liberals are giving billions of tax breaks to companies committing to building EV battery plants in Canada almost certain to become white elephants owing to the shortage of copper limiting EV output globally. Prosperity has about 1.8 billion tons of reserves grading about 0.23% copper and would have been one of the largest copper mines in North America. Canada’s Liberals are as inept as Biden’s Democrats, all hat and no cattle.

Thank you for your insights. I used to follow Jim Rogers for these kind of reviews, but he does not seem to be very active anymore, at least that I can see. I have never gone wrong investing in commodities for the long run, and suspect that will continue to be true in the future.

Just as there has been no planning to expand grids around the world while Virtue Signalling about Climate Change & EV’s. Ultimately the Liberals & Dems don’t care that there won’t be enough electricity to satisfy even a 1/3 adoption to EV’s. I certainly will need to add a couple of Copper names to my portfolio however, in the meantime I will hold on to my Uranium names until eventually even the Green nutters will embrace Niclear since it is the only suitable option for a cleaner environment.