What do U.S. LNG exports mean for domestic prices in Canada?

Expect strong pricing for years to come in the WCSB

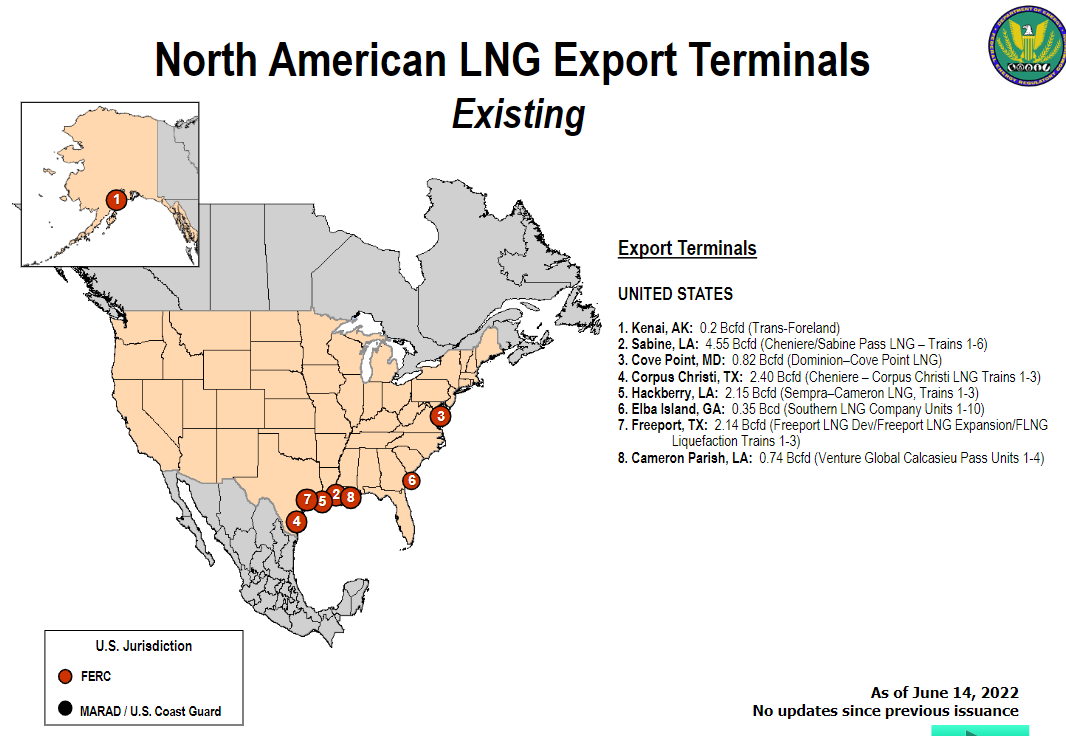

The wide price gap between domestic natural gas prices and those in Europe and Asia creates a major opportunity for American producers to export Liquified Natural Gas (LNG) to customers abroad. The United States already has eight LNG terminals in operation with an export capacity of over 13 Bcf/day.

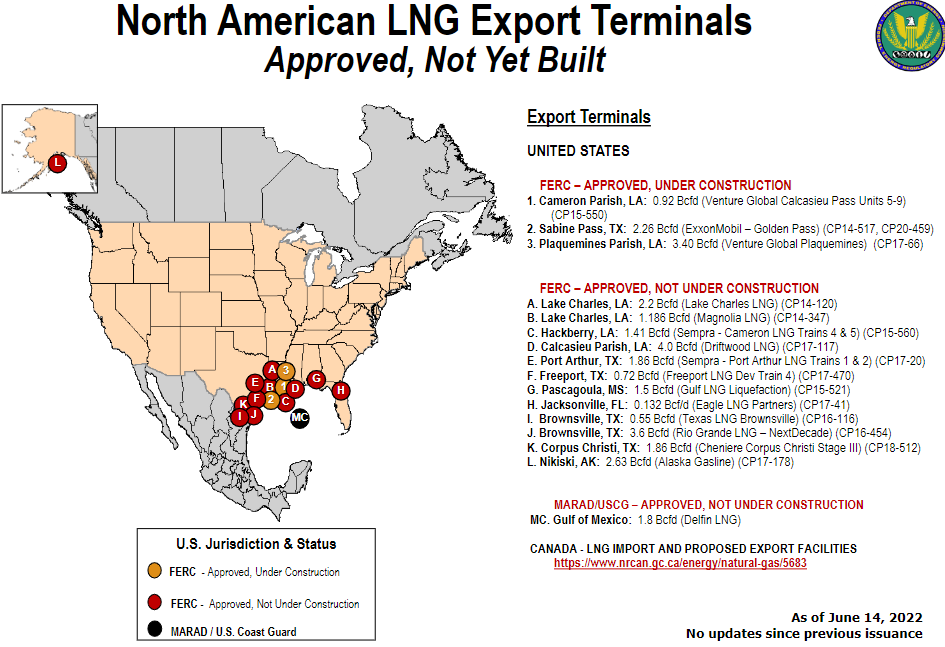

Another three LNG terminals with a capacity of 6.5 Bcf/day are under construction and 12 more have been permitted but have yet to begin construction but could potentially add about 22 Bcf/day of export capacity.

Taken together, these terminals when and if operational would bring export capacity to over 40 Bcf/day of natural gas. That compares to total domestic natural gas production of about 90 Bcf/day and domestic demand that amounts to about 70 Bcf/day in summer months and over 90 Bcf/day in winter. It should be clear that there is not enough natural gas being produced to supply domestic and export markets if all these LNG projects proceed unless domestic production ramps up significantly.

The Biden administration has promised to supply LNG to gas-starved Europe where local prices are multiples of those paid by U.S. consumers. The related agreement commits United States to supply 15 Bcf/day for the balance of 2022 and as much as 50 Bcf/day in future years. Gas producers would be more than happy to supply Europe (and Asia for that matter) with LNG at prices more than double what they receive at home, but can do so only if they expand drilling, something they have been loathe to do since the Biden administration has threatened the end of the oil & gas industry and is doubling down on its senseless “climate change” policies that pretend CO2 can cause global warming (which it most assuredly cannot).

What this tug of war means to investors is that U.S. natural gas prices will have tailwinds for years to come and tight markets will persist for an extended period. Natural gas production is quite profitable at US$3.00 per Mcf and is highly profitable at today’s prices north of US$7.00 per Mcf. With not enough gas produced south of Canadian border to meet the domestic and export demand, demand for Canadian gas will be firm and Canadian gas producers will enjoy robust pricing with their economic limited by pipeline capacity rather than willing customers. Like the Biden regime, the Trudeau government is anti-fossil fuel, anti-pipeline and deluded by left-wing “climate change” rhetoric.

The stand off has important implications for Canadian natural gas producers. Canadian gas markets are already tight for capacity and the start up of the Kitimat LNG terminal will create another 2 Bcf/day of demand, and prices are likely to remain firm for at least the next few years. Low cost Canadian producers will turn in high cash flows but rather than build output that cannot be shipped (owing to the stupid pipeline policies of Trudeau’s regime), they will try to match supply with transporation limited demand and use their surplus cash flows to pay dividends and repurchase stock. This is an investors dream outcome.

For interest, I estimate Spartan Delta (SDE.TO) cash flow at CAD$100 oil and CAD$3.00 natural gas to be ~CAD$500 million; Birchcliff (BIR.TO) cash flow at those same commodity prices to be ~CAD$550 million and Peyto (PEY.TO) cash flow at those prices to be ~CAD$800 million. That implies share prices (at 4x EBITDA) of SDE.TO of CAD$13.00; BIR.TO of CAD$13.50 and PEY.TO of CAD$14.00. I think it unlikely natural gas prices will fall to the CAD$3.00 range in a deep recession given the lack of gas in storage and don’t see enough downside in these gas-weighted shares to run for cover. The share prices may well fall below these values, but in my opinion that is more of a buying opportunity than a reason to fear losses.

Great article! Thanks for it!

As these export terminals take years AND YEARS to build, it will be interesting to see how many of the 12 permitted [but not yet in construction] terminals will actually get built. Especially so as the author references the additional supply of nat gas required for all 12 of these export terminals to profitably operate. So how does this work? Do the planned export terminals line up nat gas supply reaching them FIRST in such-and-such future year before they make a final construction decision? and for that matter also do they line up offshore customers to export the gas to, also before the construction decision is made? With price tags in the billions I assume something like this must make up a lot of their "go-no go" decision making. ?

I found your 7 May blog on the Spartan Delta business model quite interesting. Perhaps I could suggest something similar done for BIR.TO and PEY.TO as this could give us side-by-side numbers to compare the companies to each other looking out a couple of years. Just an idea.

I'm a big fan and love your content! Thanks!