Wealth management = wealth destruction

When advisers and portfolio managers get rich, you become poorer

Wealth management is in vogue today, with every major bank and related brokerage firm, insurance company and a plethora of private “wealth management” firms offering to manage your money for a fee. Globally, the “assets under management (AUM)” were an estimated $103 trillion in 2020. Typical fee structures and trading commissions (often called the Management Expense Ratio or MER) amount to 2 to 3% of the AUM, sometimes a lot more but rarely less. 3% of $103 trillion is $3.1 trillion of fees and commissions paid by investors. Advisory firms add no value to the firms in which they invest your money, in every respect they are parasitical.

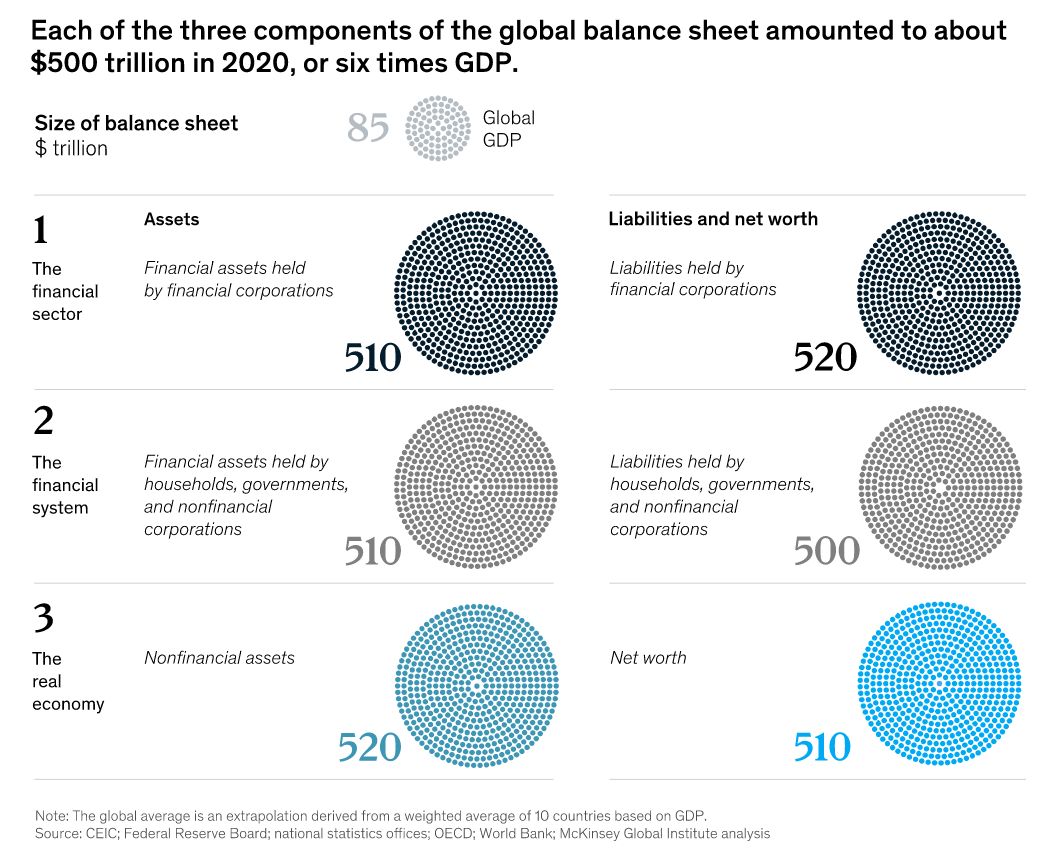

McKinsey & Company, Inc. (at one time my employer) estimates world financial assets - stocks, bonds, and related securities - total about $510 trillion. You can ignore financial assets held by financial corporations since they comprise loans offset by deposits by and large. And for the purposes of this article, you can ignore the non-financial asset sector, the largest of which is real estate. Financial assets are about six times global GDP and the “wealth” of humanity on the planet amounts to $510 trillion. Note that the “wealth” or net worth is approximately equal to the non-financial assets comprising the “real economy”. Basically, investments of any kind are financial claims on real assets, sometimes with derivatives in the mix clouding the picture but amounting to a “wash” in aggregate.

The real estate making up the largest component of non-financial assets has an estimated value of $326 trillion, leaving $194 trillion of non-financial assets comprising industry, trade and commerce (ITC) assets. A large portion of that $194 trillion of non-financial assets underlying the economy are subject to debt and equity claims comprising the $103 trillion AUM of the “wealth management industry”.

ITC generates the value added in society, which on an annual basis manifests itself in “interest” “taxes” and “profits”. The AUM held on your behalf by “wealth management” firms benefit from a share in those profits, either in the form of interest on debt or dividends. Governments at one level or another receive the taxes. I have ignored “capital gains” since those gains by one investor are losses to another. Trading in the secondary markets does not produce any value added, although it does contribute to the “commissions” portion of the $3.1 trillion or more of income to the “wealth management” industry.

Most of you have financial advisers or brokers. Do you know any of those people who live in inadequate homes or drive low-end cars? Do you know any who can’t afford to feed their families or depend on welfare? Likely not. But you should get to know the economics of your advisers or brokers since you are paying for them and the money is coming out of your shares of the value added of the businesses in which you hold investments.

Wealth management companies trade in public markets at about fifteen times net income. At fifteen times earnings the wealth management industry has a secondary market value of around $45 trillion, or almost half of the $103 trillion public market value of the investments they “manage” on your behalf. What they call “management” is difficult to comprehend, since what they actually do is trade securities back and forth between themselves and retail investors pretending that they have some special skill in finding “undervalued” securities ignoring that if they succeed, their success comes at the expense of some other poor bloke who had less insight and in aggregate all that has happened is a transfer of wealth from person or group to another, reduced by the transaction expenses. Investors as a group lose money in the process.

To encourage people to give them money to invest and add to their AUM, wealth management firms promote certain investments (the more complicated the better) and claim they can produce superior “returns” than their competitors. How have they done? Reality is that 90% of money managers do not produce above market returns and only a tiny fraction actually “beat the market” and those usually for a short time.

If investors managed their own money and did not use advisers or fund management firms, as a group they would be ~$3.1 trillion a year better off even though some of them would do worse than others. In promoting their acumen, the “wealth managers” promote the myth that higher stock prices benefit investors when the reality is that lower stock prices benefit investors. If you can buy the same interest in the future cash flows of a business for less money, you are better off, and if you pay a higher price for the same cash flows, you are worse off. This is tautological.

Society would benefit tremendously if financial management were a mandatory course in high school and citizens learned enough about investments to look after their own money. Only 52% of American households hold investments directly or indirectly. I assume that number is fewer worldwide and assuming an average of 2.1 people per household, the global number of households is ~3.8 billion and of those less than 2 billion have any investments at all. This overstates the number since the percentage of households with investments in India, China and sub-Saharan Africa is unlikely to be anywhere close to 52%, but the assumption may help make my point.

What point? $3.1 trillion in annual fees and commissions paid by <2 billion households amounts to >$1,550 per household. Gallup estimates global household income at less than $10,000 per year. Many countries have average household income below $1,000 per year. But using the averages, the fees and commission paid to “wealth managers” eat up 15% of global average household income - about the same as food or transportation for many people.

Sociologists study inequitable distribution of wealth and income worldwide should turn their minds to the “wealth management” industry which is the fastest growing and most profitable segment of banking today. It is also destructive to the wealth it purports to “manage”. In addition to the fees, commissions and expenses paid to the “wealth management industry”, investors pay for the enormous costs of regulating the participants in the secondary markets - the SEC, securities commissions across Canada and throughout the world, and a legal community who like “wealth managers” are paid handsomely for their role in mergers, acquisitions, initial public offerings, and, providing securities related advice to issuers. Like brokers, portfolio managers, advisers and all the paricipants in the “wealth management” industry, the lawyers involved contribute nothing to the creation of wealth by ITC but drain resources from the wealth creating sector of the economy, all of which is a cost paid by investors.

When reviewing your investment portfolio or pension benefits, keep in mind the following, since you are paying for them:

The average securities lawyer earns $160,017 a year

The average portfolio manager earns $114,671 a year

The average hedge fund partner earns $144,586 a year

Managing Directors of Ontario Teachers Pension Plan earns CAD$454,000 a year

Ontario Muncipal Employees Retirement System CEO earns ~CAD$2 million a year

The CEO of Caisse de Depot et Placement earns CAD$3.45 million a year

The CEO of Canada Pension Plan (CPP) earns CAD$5.3 million a year

I paid into CPP for 44 years. I now get a monthly pension of CAD$960.00.

But I earn millions managing my own money.

Regrettably I've seen this first hand. Conversation with wealth advisor inevitably turns to the purchase of their new cottage, next vacation or kids private school. Meanwhile I'm taking all of the risk and paying for meager results. Thankfully I ended this carnage years ago. Your insights are most welcome!

Hello Michael, I really enjoy your writings regarding financial markets. Thank you!