We are in bubble territory

Even at five foot six, I don't think I am short enough

A great article in Bloomberg today discusses the arcane concept of “equity risk premium” or ERP, a concept frequently embraced by market theorists who “calculate” the ERP with hindsight to draw conclusions about investor sentiment based on the theory that equity investors “demand” a higher return than bond investors to compensate for the presumedly higher risk of equities. ERP is a concept that is inherent in the now-famous capital asset pricing model (CAPM) which reduces securities valuation to a formula based on relative risk (measured by the ratio of the volatility of the price of a given security to that of the market in general, often proxied by the S&P 500 Index). CAPM has no terms which peek into the fundamentals of the wealth creating activities of the underlying business, presuming (based on the Efficient Market Hypothesis or EMH made notorious by Eugene Fama) that the fundamental are embodied in the market price of a company’s securities. The “return” ERP includes is primarily the result of changes in the market price of a security as if the “market price” fairly values the security. Oddly, financial advisors and analysts both embrace EMH yet claim they can select undervalued securities to buy or overvalued securities to sell.

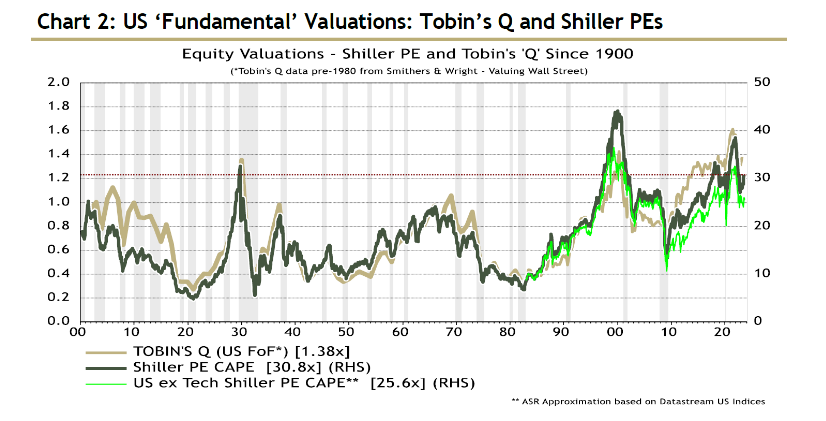

The presumption in this theoretical charade is that investors benefit from higher stock prices. They don’t. If you can buy an interest in a business at a lower price you compel a higher return unless the lower price reflects some change in the underlying business, but market price fluctuations are not driven solely by business success or failure but are more often influenced by the level of interest rates, changes in tax regimes, the rate of economic expansion or contraction, and investor sentiment. Academia is rife with studies and articles claiming investors benefit from a higher value of Tobin’s Q ratio, essentially the inverse of the price to book value ratio or the inverse of the “cost of capital” which is theoretically the return investors demand. A higher Tobin’s Q is correlated with a lower cost of capital, in essence, investors paying a higher price for the same underlying earnings stream. Humpty Dumpty is alive and well.

Bob Shiller developed the cyclically adjusted price to earnings ratio (CAPE) as an indicator as to when the stock market is overvalued or undervalued, and CAPE has been a reliable predictor of market declines when it is abnormally high and market surges when CAPE is low. The old mantra “buy low, sell high” comes to mind. A better mantra is “buy well, and hold”.

Both CAPE and Tobin’s Q are useful metrics for market watchers. Both measure the same phenomena using different methods. Lower cost of capital (or higher Tobin’s Q) rather than being a benefit is a precursor to taking a bath. Higher CAPE points to a similar experience. Today, both are in “bubble” territory. You don’t need linear regression to calculate the correlation between these two metrics.

While the throngs of sell-side analysts, advisors, brokers and fund managers on BNN, MSNBC, Bloomberg and Fox Business are telling you the markets are going higher and you should double up, they are telling their local Tesla, Porsche or Range Rover dealer they will be ordering their newest model and paying cash from your fees and commissions just as you are going to see your wealth decimated at their hands. Don’t buy into the scam. Keep some cash, invest in securities of profitable companies growing in line with the economy, paying dividends and currently out of favor with the go-go dealers on the street and look forward to a sustained flow of dividends while your cocktail party pals can brag about how well they are doing on their NVidia stock or META shares on the eve on the possible economic collapse when bubbles burst.

This is a good time to keep a cash reserve and hold some energy names since energy markets are tight and may be tight enough to ride out a recession without too much damage to balance sheets while continuing to pay reasonable dividends. At this point in the cycle, I see value in $PEY.TO, $LGN.TO, $BIR.TO, $WCP.TO AND $BNE.TO which comprise my major holdings.

Here’s a list of the energy names (compiled by Simply Wall Street) with return on equity greater than 30% in 2022, likely higher this year if the current oil & gas prices prevail through the winter. There are plenty to choose from.

Good luck with your investments.

Great post Michael. Always appreciate your analysis. Cheers