Watch Quantitative Tightening threaten more bank failures

SVB is the canary in the coalmine

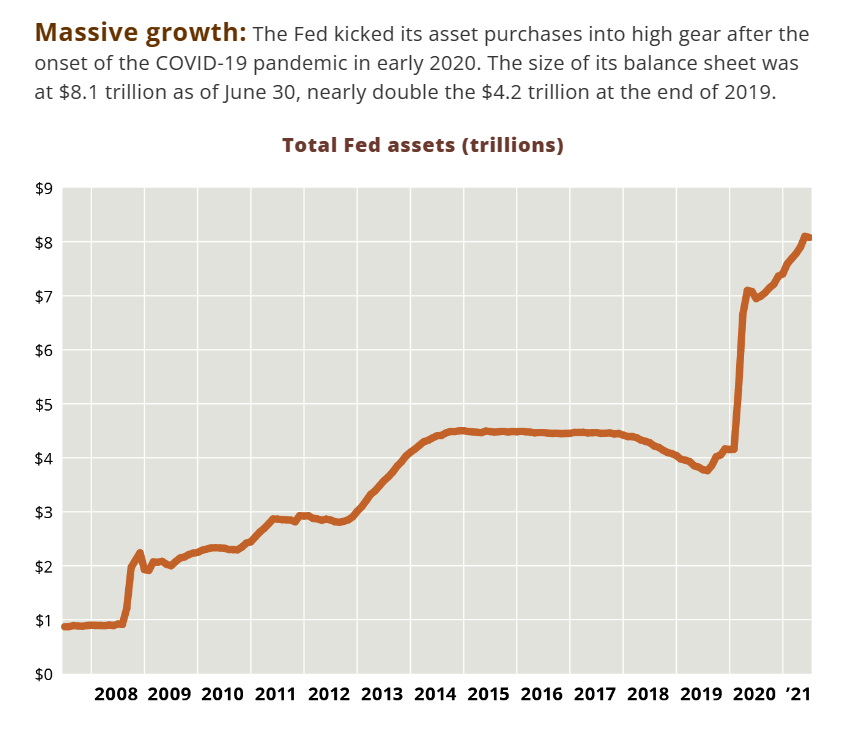

Over its years of Quantitative Easing (QE) the federal government was essentially being funded by the banking system as the Fed bought bonds and kept them on its balance sheet. The Fed’s aggressive buying of treasuries and mortgage backed securities did its job of lowering interest rates and European central banks were just as keen on QE as part of a low interest rate policy. Under this program, the Fed’s balance sheet grew to about $8.1 trillion in a decade.

The central banks of Europe, Japan and the United Kingdom added another $3 trillion (Europe 688 billion Euros,United Kingdom over 1 trillion pounds sterling and Japan 152 trillion yen). They were having a party and no one wanted to stay home.

Modern Monetary Theory (MMT) proponents argued that governments could just keep borrowing money as long as the added money supply did not go into circulation but sat on the Fed’s and banking system’s balance sheets and that the growth in money supply was not inflationary since the effect of QE was to lower the velocity of money by enough to offset the rise in bank balances. And the velocity of money did fall during the period QE was operating, from about 2 times in 2000 to as low as 1.1 times in the first quarter of 2020.

A side effect was increased bank liquidity allowing loan growth. Almost utopian while it works.

But it stopped working when COVID prompted governments to flood society with cash giving billions of dollars to individuals and businesses to keep them afloat during periods of mandated “lockdown” erroneously believed to be necessary to stop the spread of COVID and “save lives”. The lockdowns did little to prevent the spread of COVID but did real damage to the economy and the “free money” from governments swept the problems being created down the road. The money pumped into society began increasing the velocity of money, a uniquely inflationary outcome. By the beginning of the third quarter of 2022, the velocity of money in United States had increased from 1.1 times to 1.2 times, a rise of ~10%. I suspect it is still rising and will continue to rise throughout QT.

In parallel with actions to support people during COVID, left wing governments in United States, Canada and Europe universally bought into the specious “climate change” narrative promoted by the United Nations and th World Economic Forum (WEF). The theory that CO2 causes global warming is nonsense, readily disproved by application of the laws of physics, as this recent paper by Dieter Shildknecht reports. The left wing addiction to its climate change narrative is so pervasive open discussion is censored, grant money is denied and scientists (including over 60 Nobel laureates) who disagree were vilified for their heresy. I like to remind people that true science recognizes there are questions that cannot be answered but it is only political and religious leaders who claim there are answers that cannot be questioned.

In any event, in order to curb inflation central banks have begun to raise overnight rates and embark on a program of Quantitative Tightening (QT) and have begun to reduce their bond holdings. But with governments continuing to run massive deficits, bond issuance is continuing and the bonds have to be owned by someone. Who?

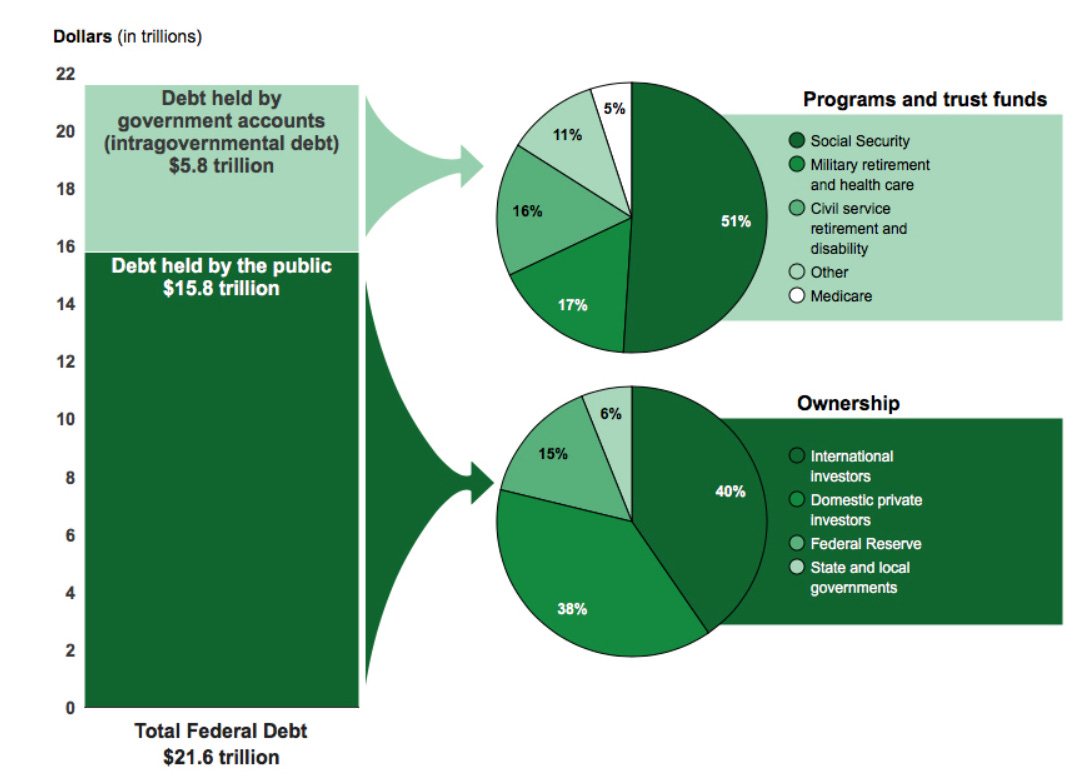

In 2019, U.S. national debt was over $21 trillion and 40% of that debt was held abroad.

Today, the American national debt is over $31 trillion. Rates are now rising and the market value of that debt is falling.

The case of Silicon Valley Bank (SVB) is illustrative. SVB’s depositors were mostly Silicon Valley businesses many of whom are early stage companies. To earn a spread on the deposits (most of which were uninsured) SVB invested in treasuries and mortage backed securities to get enough spread to keep the lights on had to move out along the yield curve since very short term debt had nominal interest. Not a credit problem since the treasuries were AAA credits, but the mismatch of maturities became an issue when some depositors saw the liquidity risk and asked for their money and word got around with a snowballing effect. A “run on the bank” ensued. In a short few days, SVB failed and was taken over by the FDIC with government deciding to bail out the depositors, even the uninsured ones.

The total U.S. banking system has assets of about $24 trillion. Domestic ownership of U.S. national debt must be approximately $15 trillion if foreign ownership is still about 40%. It is safe to assume a significant portion of U.S. banking assets (either directly or in terms of collateral for loans) comprises U.S. treasuries. U.S. banks have leverage ratios between 6.5% and 11.5% according the Global Association of Risk Professionals. Assuming an average of 8% U.S. banks have a capital base of $2.4 trillion more or less.

The Brookings Institute estimates the weighted average maturity of the U.S. national debt is about 73 months (just over 6 years) and in 2021 the average interest rate on that debt was 1.6% (Pew Research). The Congressional Budget Office estimates the 2023 U.S. deficit will run about $3 trillion.

What does it all mean?

It means someone has to buy $3 trillion in treasuries to fund the government, another $5 trillion to roll-over existing debt with a 73 month duration, and some portion of the approximately $8 trillion of government debt the Fed will try to sell to execute QT over the next few years. That is a lot of supply and the market will react in rates. It is specious to think that existing holders of treasuries will be content to roll over their holdings at rates near zero and inflation approaching double digits, so buyers will demand higher rates. With rates more likely to rise than fall, trading values of fixed income securities on bank balance sheets will follow SVB down the rabbit hole of a major mismatch with large negative “mark to market” losses. Depositors often flee banks when net tangible equity falls to zero or a negative number, as was SVB’s experience, and some recapitalization will be needed to maintain the banking system and prevent “runs” on banks and government guarantees that exceed the $250,000 FDIC insurance on deposits is already being discussed.

All of these band aids will buy time but sooner or later real money is needed at where will it come from? Individual citizens, corporations, or foreign investors seems like a comprehensive list of potential sources. Much of individual savings is held by institutions on their behalf, names like Vanguard, Fidelity and Blackrock. Are money managers who are paid based on a percentage of AUM going to flood into treasuries during rising rates given their obligation to “mark to market” daily? That seems a bad bet.

Can American citizens increase their savings? That seems unlikely. U.S. households are already about $17 trillion in debt and costs of living are rising as both inflation and rising interest rates affect household budgets.

Corporations are in better shape with cash of close to $5.8 trillion. President Biden wants to grab some of that cash by raising taxes on corporations (as well as wealthy Americans). Corporations have shown a preference to distribute their surplus cash through dividends and buybacks, and a reduction in capital expenditures will manifest itself in lower economic growth and less government revenues. In 2021, U.S. corporations spent $848 billion of their $2.8 trillion profits on share repurchases and paid another $1.4 trillion in dividends. Don’t expect corporations to bail out Biden’s reckless spending plans.

Reliance on foreign investment is a dangerous road with plenty of national security implications. I doubt they will increase their exposure to the weakening credit of United States and may find their own budgets a bit stretched owing to inflation and slowing economic growth.

The table is set for a financial crisis of epic proportions accompanied by a seriously punishing rise in interest rates. The history of overextended governments and overtextended households is rife with examples of how markets resolve this dilemma. Argentina, Mexico, Turkey, Brazil, Zimbabwe, and Venezuela have all taken their turns at the “Weimar Republic” experience of dramatic rises in inflation, crippling interest rates and economic devastation.

As I see, this is so far a slow-moving train wreck that could go off the rails at any time. If it does - more banks will fail and the left wing policies that created the problem will now experience their inevitable product - economic chaos. Many triggers are developing to set off the time bomb the current debt situation presents - they include a worsening global energy shortage caused by failure to invest more capital in fossil fuels; an expansion of the war in Ukraine; an invasion of Taiwan by China; or the complete collapse of the so-called “crypto” industry which has sucked up a trillion dollars of capital globally but is devoid of any underlying value and with 19,000 unregulated “tokens” in existence is the wild west of excessive speculation. Cryptocurrencies have been touted as “safer” than fiat currencies but the line ups of depositors at banks like recently failed Signature Bank that made a business out of lending to cryptocurrency exchanges is evidence that the claims of “safety” were stretched past the breaking point. Loans “secured” by cryptocurrency tokens are essentially unsecured since those tokens have zero intrinsic value, a reality that Sam Bankman-Fried may find time to write a book about from his likely prison cell.

Today, investors are wise to batten down the hatches, reduce exposure to fixed income securities and keep a healthy cash balance despite its erosion by inflationary trends. Hold more “real assets” like resources and real estate financed with little financial leverage and wait for the market to serve up seriously undervalued stocks as the woefully stupid left wing policies of Western democratic leaders tank world markets. It can’t happen to soon for me.

But but but ... SVB had a really good ESG rating , That’s so important to sustainability

Michael do you know of an ETF of stocks with good ESGs ? I’d like to short it

Liquidity is such a fun dynamic to watch

Yesterday was chicken little for regional banks

Today ....

Hahaha

FIRST REPUBLIC BANK SURGES 61% AT OPEN AS RECORD ROUT EASES

*WESTERN ALLIANCE BANCORP JUMPS 53%, TRIGGERS TRADING PAUSE