Valuation of Commodity stocks

A key to investing in energy or mining stocks

Academic have long known that commodity prices are log-normally distributed. Since the Nobel prize winning work of Fischer Black, Myron Scholes and James Merton in creating the Black-Scholes model of option pricing, valuation experts have expanded Black-Scholes concepts to the valuation of oil & gas reserves as a “real option”. Mercer Capital, a Business Valuation and Advisory firm has published papers on how Black Scholes can be usefully applied to valuation of proven but undeveloped oil reserves.

The United States Energy Information Administration uses Black Scholes concepts to forecast the range of future oil prices based on market implied volatility. Log normal distributions are used for real estate prices, stock prices and the size of oil reservoirs, among other applications. The distribution follows the same principles as the normal distribution except that the values are skewed to the lower end of the range of possible values. Probabilities based on analyis of mean and standard deviation produce the same results as in the standard Gaussian distribution.

Why oil prices and related valuation of energy companies are subject to analysis using log normal distributions arises from the characteristics of most commodities - the ultimate value of a given commodity reserve is directly related to the size of the deposit or reserve and the price it may command at future points. Log-normal distributions are routinely applied to estimating the size of oil reserves and similarly applied to estimating future stock or commodity prices. So instead of over simplifying analysis of energy stocks by applying EBITDA multiples to reported financial results or attempting DCF valuation using projected commodity prices, a more robust valuation can be arrived at using Black-Scholes and valuing the proved and probably reserves as a “real option”. The result is often not far from the oversimplified multiple approach but sometimes produces widely different outcomes. In the example I will show, the differences are not extreme.

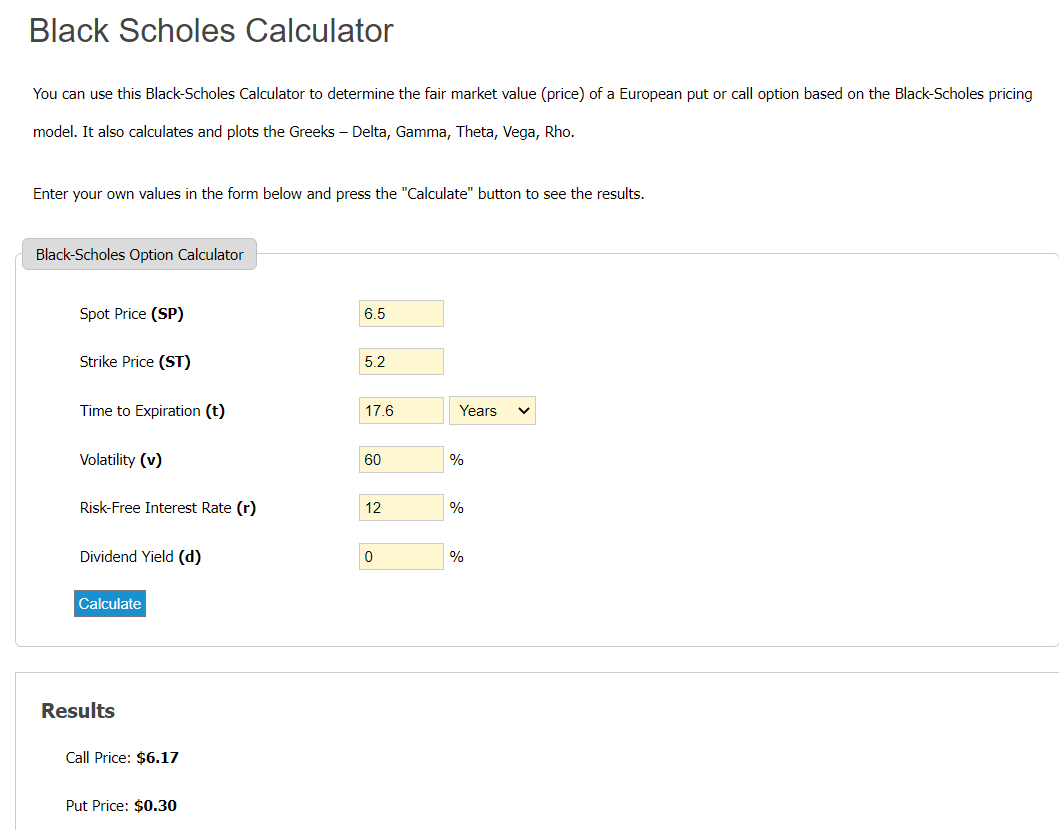

Output and Inputs are as follows (I will ignore dividends since they are discretionary and deal with when you receive the benefit of the investment, if any, not its quantum. Dividends are included when valuing stocks using Black Scholes since the dividends can be paid during the option tenure but the option holder does not get them. In valuing the totality of a commodity reserve, the investors receive all of the income from exploitation of the deposit, if it generates any income):

Spot price - CAD $6.5 billion Present value of future cash flows from reserve report without discounting.

Strike price - CAD$5.2 billion future development costs from the 2021 Whitecap reserve report without discounting.

Volatility - estimated using the market volatility of the related energy commodity prices as a proxy for future probabilty. Estimated annual volatility is equal to daily volatility multipled by the square root of the number of trading days in a year. With Monte Carlo simulation you can adjust for possible errors in the estimation of volatility by repeating the valuation with different volatility estimates creating a range of outcomes.

Time to maturity - the life of the option is the life of the reserves at current production rates, or for undeveloped but proven reserves, the time frame before which the reserves revert to the Crown if the company is not currently producing (more often the case with junior mines than with oil & gas companies)

Risk free rate - While the real risk free interest rate is a concept and not a reality, a useful proxy is the 10-year T bill rate plus the rate of inflation. Pretending the 10-year T bill rate is “risk free” when inflation is running at twice the interest rate on that instrument is a common error in valuation. Absent central banks intervening in markets, investors would demand a real return of about 4%.

Applying this approach to the example of Whitecap Resources (WCP.TO).

Spot price = CAD$6.5 billion

Strike price = CAD$5.2 billion

Volatility = 60% (~4% daily volatility x square root of 230 trading days = 60.4)

Time to maturity = Reserve life index reported as 17.6 years

Real Risk Free Rate = 12% (10 year T-bill rate of 4% plus 8% inflation)

Option price = CAD$6.17 billion or about CAD$10 per Whitecap share with 617 million shares outstanding (see below).

Based on this approach the current WCP.TO trading price of CAD$8.40 per share seems undervalued. This analysis which uses 2021 data does not include any impact (positive or negative) from the XTO acquistion which recently closed but which will have a material impact on future cashflows. Absent the XTO acquisiton, Whitecap was on track to being debt free in the near future so no adjustment for debt is included. Accordingly, this article is illustrative and not intended to be an estimate of current value of WCP.TO.

Interesting. Curious why is the strike on PDP of $6.5b and not total proved of $11.2b? Given future development costs are on total proved? Same thing with reserve life...using PDP but reserve life of ~17 years based on proved + PUD i.e. proved RLI only 12.5 years?

Newby take: if oil price is log normal and stock price is 100% correlated with oil price (which I believe it is) - then your exposure to oil stocks should be probably somehow proportional to area under the curve to the right of current price. Means - the higher oil price the less exposure you should have. Never to zero but 100% is also rather exceptional (like in once-in-a lifetime case with negative prices).

Of course this curve is not static and changes over time. And thought must be given if it commands your total exposure or just %% of your new investment related to available cash pool. But still it’s worth further elaboration.

Michael, thank you for this post, it gives some fuel to thinking.