Trump's proposed tariffs are unlikely to fuel inflation

But they won't replace much income tax as a source of revenue either

For over 100 years the U.S. government was funded through tariffs. Income taxes did not exist until 1913 when enacted to fund WW1. The inflation rate from the time tariffs were first enacted in 1789 to 1913 was one tenth of one percent yet American went through the longest growth phase of its existence - the industrial revolution. Tariffs became a less important source of revenue from 1850 to 1913 comprising about half of government revenue until income taxes were levied in 1913, with government revenues augmented by revenues from various fees and charges.

Trump has declared he will enact higher tariffs. American imports run about $3 trillion a year and an across the board 10% tariff would raise no more than $300 billion, a fraction of the over $4 trillion of federal spending, half of which is funded from income taxes and another 35% or so by social security taxes and contributions. But a well targeted set of tariffs will make a difference to the U.S. economy and claims they will fuel high inflation are nonsense. They will have a one-time and quite minor impact on retail prices.

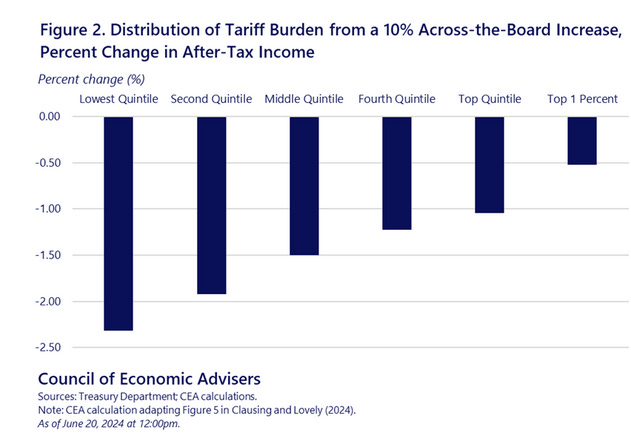

The U.S. Council of Economic Advisers (COE) estimates a 10% across the board tariff would result in a higher cost of living ranging from 2.3% at the lowest income band to 0.5% at the highest income level, the difference being a result of the lower income bands spending more of their income to meet day to day costs of living.

That COE estimate assumes all tariffs are passed on to consumers in the price of imported goods either directly or indirectly. But exporters to the U.S. have to compete in the U.S. market and if they don’t match the prices offered by U.S. suppliers they will just lose market share. Some portion of tariffs will be passed on but not all. Domestic suppliers will benefit from higher volumes and, owing to competition among them and improved economies of scale, will likely reduce prices on their domestic production. On balance, I think the one-time increase in retail prices arising from a 10% across the board tariff would be closer to 1% for the lowest income quintile and a fraction of 1% on average.

Stronger domestic production should manifest itself in higher employment levels and a stronger economy. Trump proposes to cut corporate tax rates which will also tend to soften inflationary pressures. Corporate taxes in the U.S. aggregate about $440 billion and Trump’s plan to cut corporate tax rates to 20% from 21% would reduce revenues from that source by about $40 billion while the tariff proposal should generate a multiple of that amount with a net improvement in the fiscal balance of 6% to 8%.

Trump (and Harris now) proposes to end taxes on tips, which will cut federal revenue by a nominal amount since total taxable income from tips in the last year was about $38 billion and the tax collected no more than $10 billion. Of all income taxes collected, 97.7% of those taxes are paid by the highest 50% of income earners and only 2.3% by the bottom half. That 2.3% amounts to about $50 billion, and this group will see their taxes fall by $10 billion from the “no tax on tips” policy, more than offsetting the impact of tariffs.

Trump proposes to make benefits from social security non-taxable, again assisting those low income Americans reliant on social security benefits. On balance, lower income Americans will be better off under Trump than they have been under the Biden-Harris administration.

Harris has been quiet about tax policies, other than copying Trump’s “no tax on tips” policy and matching his child tax credit proposal with a $6,000 credit for first children compared to Trump’s $5,000 child tax credit for all children. At this point, Harris has not disclosed enough policy proposals to permit a meaningful comparison of any detailed proposals relative to those suggested by Trump.

The major point of tax policy difference relates to the expiring Trump tax cuts from his time in office. Trump would extend them and Harris would let them expire. That is a major tax increase if Harris is elected with all of the economic consequences of higher taxes, which perversely may result in less tax revenues if the Laffer curve applies, and certainly means lower economic growth. Laffer posits that higher tax rates can cause lower economic activity resulting in lower tax revenues if the tax rates are higher than what Laffer calls an “optimum” level. There is considerable debate about where the optimum tax rate lies but it is clear that at a 100% tax rate there would be zero revenue since no one would even bother working if all of their income were taxed away.

In many ways, tax policy and fiscal policy have similar impacts on economic activity. Deficits traditionally stimulate more economic activity by pumping money into the economy and higher taxes restrain activity by taking money out. But in both cases, it is a matter of degree. Very high deficits (such as those in U.S. and Canada today) lead to less growth as government borrowing crowds out private borrowing and drives up interest rates which restrain economic growth. Sensible governments seek to find a balance that ensures social services are funded while economic growth continues at sustainable levels and inflation remains manageable. These decisions cannot be made rationally based on ideology but must deal with reality.

Trump’s proposed tariffs can benefit or harm America and, like deficits and taxes, it is a matter of degree. Based on his published proposals, Trump’s 10% across the board tariff proposal with higher tariffs on certain items should produce a good result.