Transform your portfolio with Hammond Power Solutions

One by-product of the EV craze is that transformer demand is booming

As leftist governments squander billions on subsidies for wind, solar and electric vehicle (EV) battery plants, their dream of an electrified world ignored the demand created for battery metals and caused a bull market for copper, nickel, cobalt and lithium miners. Except for Tesla, North American auto assembers have been taking a bath on EV’s, losing billions and showing signs of strain to the extent they are cutting back on EV output and related investments.

Notwithstanding, EV demand will continue to grow since, green or not, EV’s are nice vehicles - quiet, fast, and in many cases beautifully designed. The electrical grid needs upgrades to support the charging infrastructure. At the same time, housing shortages are prompting efforts to quite sharply increase residential construction.

Almost ignored in this environment, manufacturers of power and distribution transformers should have a field day. Transformers are fundamental to expanding the grid and delivering power to charging stations and new homes.

Source: Energy Minute

Federal Pioneer Limited (acquired by Group Schneier in the late 1980’s but of which I was chairman for a couple of years and through The Enfield Corporation Limited (which I founded in 1984) was the controlling shareholder until 1989, operated a power transformer business with operations in Regina and Winnipeg. That once public enterprise is gone, and the transformer business is now privately owned by PTI Power Systems.

That leaves former FPE competitor Hammond Power Solutions (HPS.A.TO) (Hammond) as the only publicy traded Canadian transformer supplier. Early investors in HPS.A have foudn the investment more than satisfactory with the shares rising from $18 to $80 in the past year. The company still trades at about 16 times earnings and revenue has almost doubled since 2018.

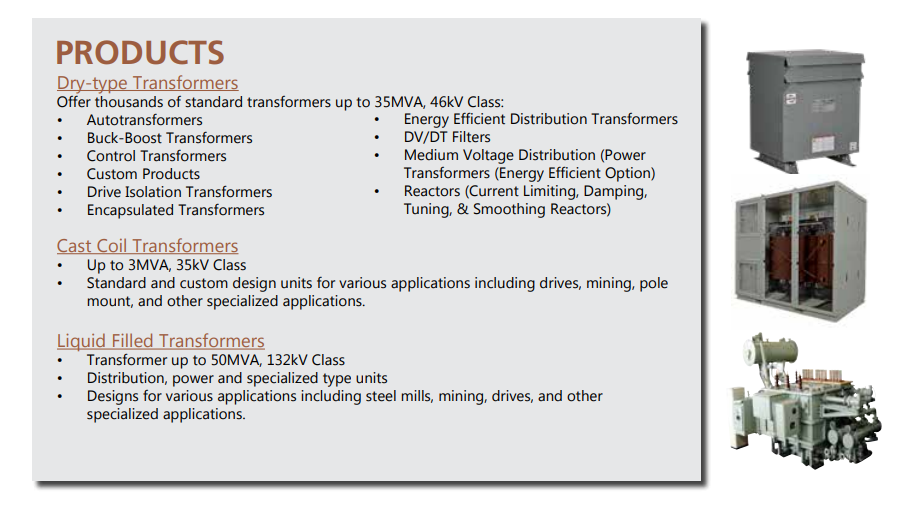

Headquartered in Guelph, Hammond has been in operation since 1917 and operates not only in Canada but also in United States, Europe, and Asia. The company’s dry type, cast coil and liquid filled transformers are staples of electrical distribution and in my opinion the company can look forward to years of sustained growth and profitability.

A small capitalization company with 1,300 employees and a market capitalization of about CDN$750 million carries risk but with only 9 million shares outstanding has high share price leverage to improving results.

I think it is undervalued and a reasonable speculation for risk takers.