Touchstone Exploration seems undervalued by the market

Touchstone Exploration seems undervalued by the market

But that could change if 2024 sees a significant increase in production beyond guidance

Touchstone Exploration (TXP.TO) is a Canadian oil & gas developer operating exclusively in Trinidad, and has started on a path of rapid growth after making significant natural gas finds which it has contracted with Trinidanian utilities at US$2.47 per gigajoule with 2% annual escalation. Production surged in 2023 growing from 1,577 barrels of oil equivalent (BOE) per day in 2022 to almost 4,000 BOE/day in 2023, with 2024 guidance at 9,700 BOE/day. Based on the projected 2024 output, Touchstone has a reserve life of over 30 years.

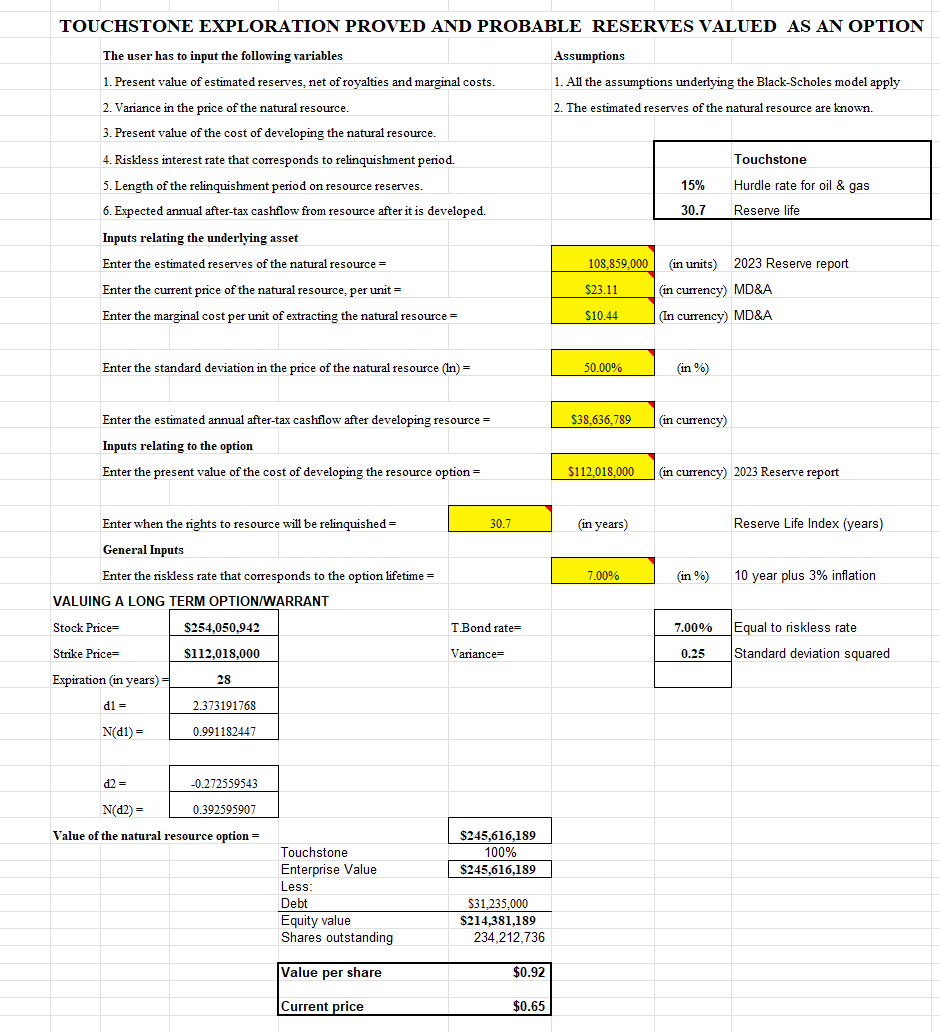

A Black Scholes valuation of those reserves treated as an option on future commodity prices yields a value of US$0.92 versus current trading prices of US$0.65 per share (CDN$0.87).

Touchstone reports in U.S. dollars despite its Calgary head office and Canadian listing. The company has been building out infrastructure capable of delivering more than double current output, and if 2024 drilling expands output to fill out infrastructure (presuming demand is there) the value doubles to the US$1.80 range as the reserve life index falls to ~15 from 30.7 years. Simply stated, no increase in reserves or reserve replacement is needed to surface added value. This is not to say no additional reserves will be found. In fact, Touchstone’s acreage is a long way from fully developed and further growth is more likely than not.

I owned 500,000 Touchstone shares purchased at CDN$0.43 per share in 2019, but sold those shares as part of a reorganization of the private company through which I held them where some of the TXP shares became registered to me directly and others to the new owner of the private company. I sold those registered to me at prices close to cost. The new owner of the private company eventually sold the TXP shares they acquired as part of the transaction for close to CDN$2.00 a share.

I continued to follow the company but owned no shares.

Now that Touchstone has become a more interesting investment, I contemplate adding shares in the coming quarters if evidence of continued growth emerges. In my opinion, the shares are undervalued and have speculative appeal.

Nice article, certainly a conservative view but considering the management teams long tenure I think they know this market and the routes to success well, they current have built out infrastructure to handle over double current production levels but we will have to see how successful their future prospects deliver over the next 2-3 Qtrs, great baseline in FY23, FY24 will be 50%+ minimum by end of year...