Touchstone Exploration - emerging gas producer?

This small cap stock has big plans and high risk but may be worth a gamble

A few weeks ago I wrote an article on Touchstone Exploration (TXP.TO) in which I held 500,000 shares through a corporation I then controlled. The shares were a residue of a company called Petrobank which was parent of Petrobakken, a company which failed owing to too much debt. I touted a BNN interview with Josef Schacter in which he had named Touchstone as a “top pick” calling for growth to 28,000 Boe/Day based on some recent exploration successes. I was skeptical but intrigued.

Yesterday, the company announced it had received an environmental permit for a large natural gas discovery and was beginning construction. The press release indicated the permit allowed a 200 million cubic feet per day facility. That is significant for a company whose annual oil production was less than 1,500 barrels a day, since 200 million Mcf is about 33,000 Boe/day based on a 6.1 to 1 conversion factor. Index Mundi reports that Trinidanians pay over $45 (Trinidanian dollars) per million BTU’s for natural gas, equivalent to about CAD$9.00 per Mcf. That is not far off the current Henry Hub price and I suspect Touchstone will get a price of at least half of that.

It is early days and there is not much data to work with, but my guess is that Touchstone will take a few years to get anywhere close to 200 million cubic feet per day from this discovery, but if and when the company reaches that level of output, revenue at $5 per gigajoule would be $5 x 365 x 200,000 = CAD$365 million. Natural gas producers typically earn at 30% gross margin on a fully costed basis and to put four corners around the size and scale of this potential, I see Touchstone having cash flows north of $100 million a year and an enterprise value of ~CAD$400 million, more or less. The company has 212 million shares outstanding trading at CAD$1.65 a share so the market is discounting much of the potential.

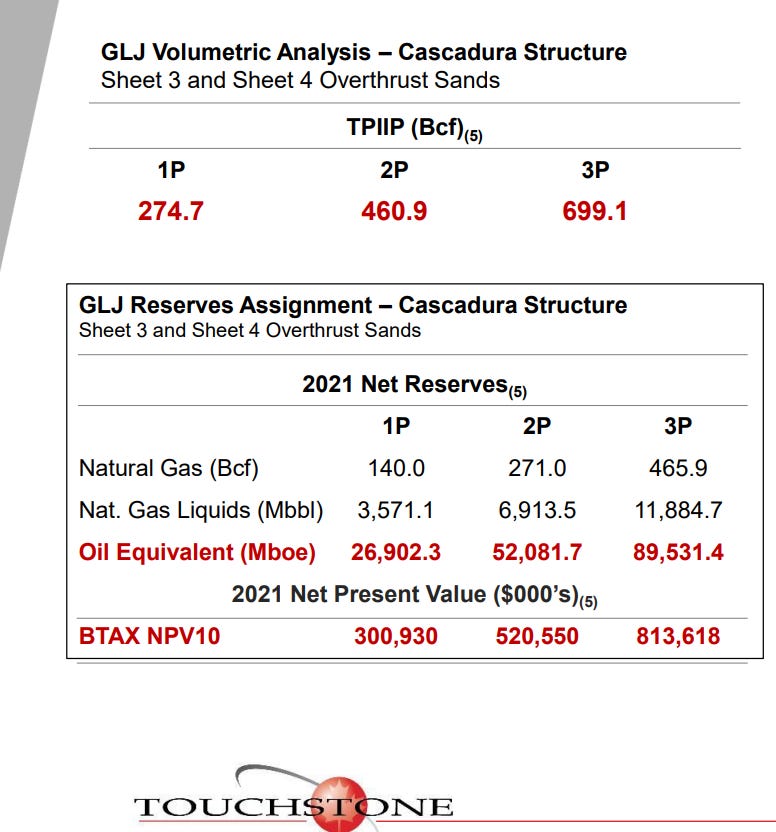

I typically do not buy into speculative positions but in this case I am making an exception and bought 20,000 shares. The Cascadura reservoir operated by Touchstone reportedly has at least 140 Bcf of natural gas reserves, capable of supporting a lot more than 200 million cubic feet a day of production.

I expect capital costs to develop Cascadura are likely to be CAD$300 million or more and the risks are high. But it would be nice to see another Canadian success story and I can well afford to lose my CAD$34,000 investment if it goes badly. I have no idea whether it will work out well or go bust. Good money after bad? Probably, but it has speculative appeal for me given the size and scale of the Cascadura formation.

It is shaping up like Josef Schacter was right. We will see.

I agree. I like the odds on this one

You do realise that TXP has a fixed price deal for their gas with the NGC. They get 2.5$. They will not be getting "half the HH gas price" you suspect...no........fixed price 2.5$