The sell off in energy names creates opportunities

Pine Cliff Energy is coming of age

Pine Cliff Energy (PNE.TO) is a small capitalization gas-based Canadian producer which today reported it has become debt free and will pay a dividend of $0.10 annually paid monthly starting this month. Not a moment too soon, as oil & gas stocks plummeted today on recession fears.

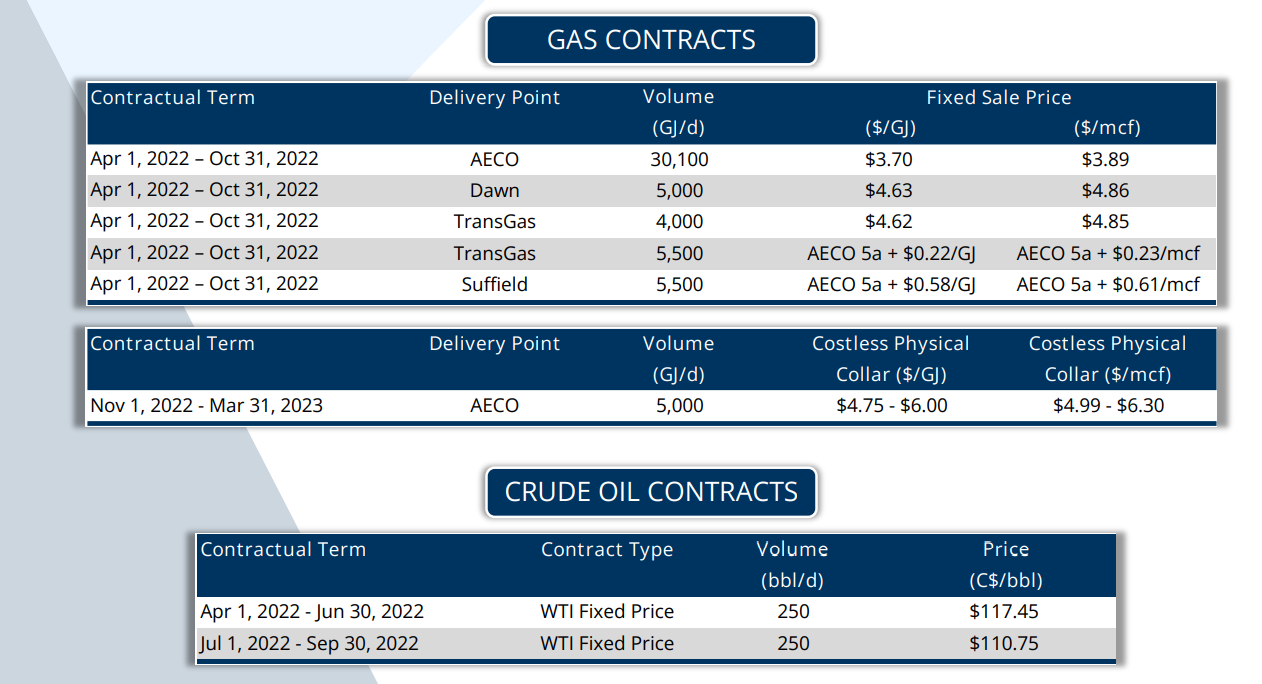

Ninety percent of Pine Cliff’s production is natural gas and the outlook for natural gas is strong, with summer storage levels well below typical levels and current prices in the CAD$5.00 per gigajoule range. Pinecliff has hedged much of its production at prices of CAD$3.70 to CAD$6.00 giving it some protection if the North American economies dip into recession, but at the expense of higher cash flows if prices rise.

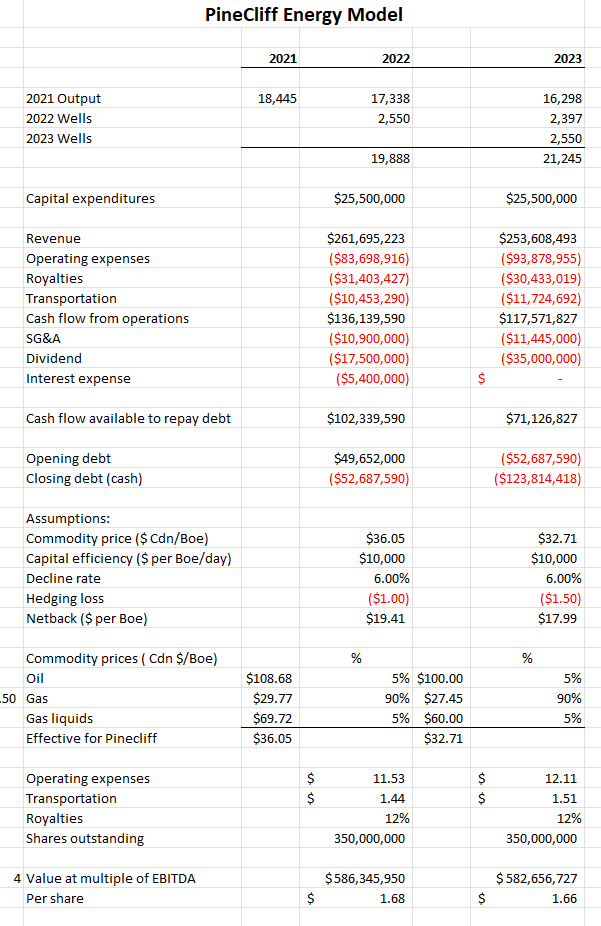

Pinecliff has a low 6% base decline rate putting the company in the enviable position that little capital is needed to sustain output. I estimate the company will end 2022 with CAD$50 million in cash and generate ~CAD$100 million free cash flow in 2023. My model is set out below:

At its current price of CAD$1.50 per share, Pine Cliff seems modestly undervalued at a multiple of four times EBITDA, but given its low decline rate and high free cash flow (which I value at a ten times multiple) the shares have a potential value of closer to CAD$3.00 a share and with a CAD$0.10 annual dividend have a cash yield of 6.7%.

I typically stay away from mico-cap names but like this one for its clean balance sheet and capable leadership under legendary George Fink who acts as Chairman. I own 15,000 shares.

Mr. Blair

Another insightful analysis of a Canadian energy company. I have a position in this firm and expect to add to that position as this free fall completes. Thank you very much.

Thank you for sharing Mike. Been a fan of PNE.TO I hope they will recognize this news. https://twitter.com/BOEReport/status/1544082387520200704