The rush into lithium stocks seems misguided

Too many investors can't read below the headlines

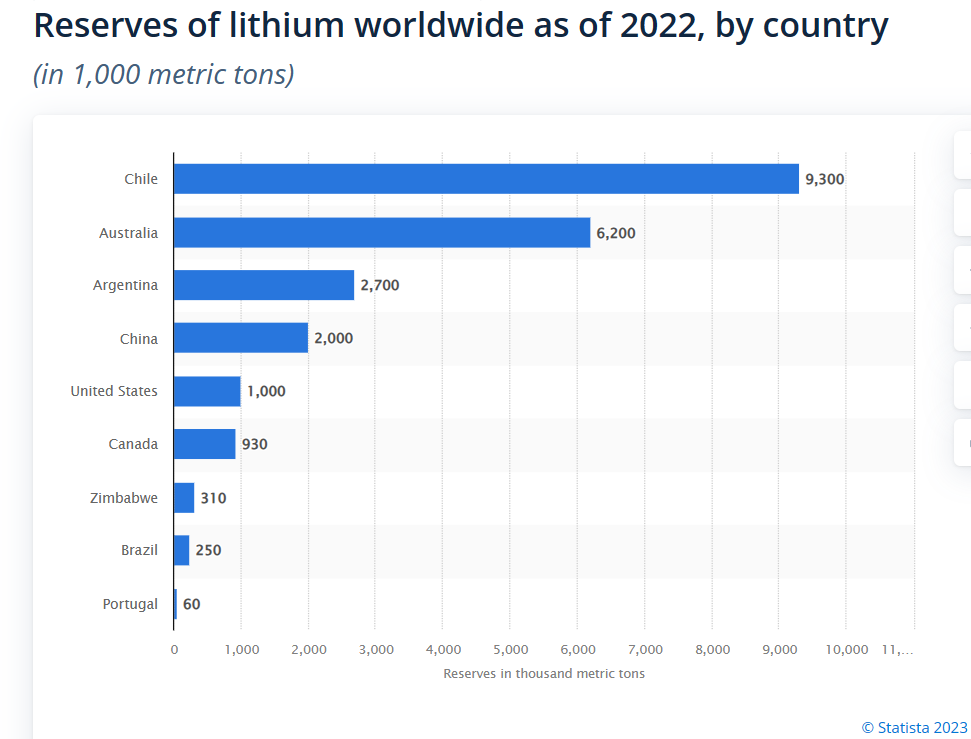

As the electric vehicle (EV) market grows, there has been a bull market in lithium stocks as if there was going to be a severe shortage of lithium. Reported reserves of lithium amount to over 20 million tonnes.

The average EV battery may be called a “lithium ion” battery but that doesn’t compel the conclusion it contains much lithium. In fact, lithium is a fairly minor mineral in an EV battery amounting to only 6 kg or about 3% of the minerals in the battery by weight. The known reserves of lithium would support over 3 billion EV’s whereas the world fleet of vehicles is about 1 billion vehicles.

There will be a serious shortage of battery metals as EV’s grow in volume but the pinch point is more likely to be graphite, cobalt, nickel, or copper. World reserves of cobalt comprise about 8.3 million tonnes and there is twice as much cobalt in an EV battery as lithium.

Copper usage is not confined to the battery of an EV but finds itself throughout the windings of the electric motor and the vehicles wiring. Total copper consumption in the average EV is about 185 pounds compared to 35 pounds n the average internal combustion engine (ICE) vehicle. The supply demand balance for copper is tight already and the lead time to find and develop new mines is measured in decades, particularly in left wing Canada where the Impact Assessment Act has made the time from discovery to production for a new mine as long as twenty or thirty years. Copper grades are falling and added copper output will come at a higher cost.

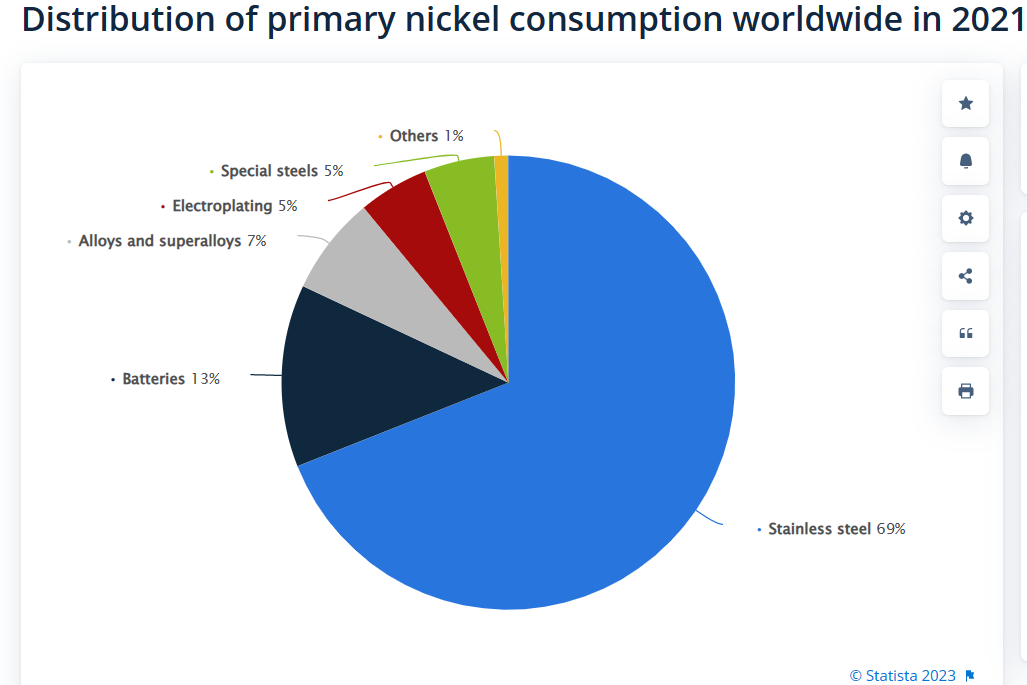

World reserves of nickel comprise some 95 million tonnes. With 27 kg of nickel in a typical EV battery, nickel markets will also be tight for years to come. Nickel’s primary market is stainless steel which consumes almost 70% of nickel production annually. As EV demand grows, nickel prices will likely rise.

Smart money eschews the lithium fad and places long term bets on copper and nickel mines such as Hudson Bay Mining (HBM), Capstone Copper (CS), First Quantum Minerals (FM), Nickel28 Capital Corporation (NKL), Canada Nickel Company (CNC) and Lundin Mining (LUN) as well as majors like Glencore (GLEN), BHP Group (BHP), Southern Copper (SCCO) and Freeport McMoran (FCX). Development stage mines like Western Copper (WRN) and Solaris Resources (SLS) are worth including as is Arizona Mines (AMC). Teck Resources (TECK.B) is reorganizing itself into a pure metals company emphasizing its excellent copper assets and will become an institutional favorite. Long shots include Northern Dynasty Metals (NDM) and Taseko Mines (TSK) which have very large, rich deposits tied up in regulatory approvals with a lot of opposition to their permitting despite the massive resources each presents. Politics plays such an important role in the permitting of a major mining project that common sense suggests keeping jurisdiction risks in mind and not fooling yourself by believing Canada or the United States are “safe” jurisdictions under progressive governments that have frequently shown a propensity for stupidity in their environmental policies regardless of their rhetoric. Chile and Peru are probably just as safe since, despite governments with mercurial policy decisions, the economies of these countries depend on mining and one way or another they will come to terms with miners that work for all parties.

A portfolio of copper and nickel mining stocks should provide long term benefits and in my opinion would benefit from inclusion of all the names mentioned.

I like Glencore. They have their feet in both the coal camp and the net zero camp .