The real risks of leftist policies remain high

Driving interest rates down with quantitative easing has consequences when unwound

The U.S. banking system is a long way from health as the combination of leftist intervention in markets to drive down interest rates called quantitative easing (QE) fueled asset bubbles and added fuel to the inflation fire as the Fed was forced to raise rates to curb inflation which hit as high as 8%. In addition to raising the overnight rate, the Fed has to unwind the trillions of dollars parked on its balance sheet from the QE period and deal with what is today called quantitative tightening (QT). QE was popular politically since it made mortgage rates fall to historic lows and allowed the federal government to borrow at near zero interest rates, encouraging the Biden administration to follow the Trump administration habit of running major deficits since the government could claim that debt service costs were still a small percentage of gross domestic product (GDP).

The inevitable result of buying votes with taxpayer money augmented by reckless borrowing was the rise in inflation of the past two years which got a boost from silly climate policies that pretend CO2 causes global warming driving capital out of the oil patch and running fossil fuel prices northward. To rein in the inflation, Biden enacted the “inflation reductionc act” or IRA which does little to mitigate inflation but comes at the expense of billions more federal debt.

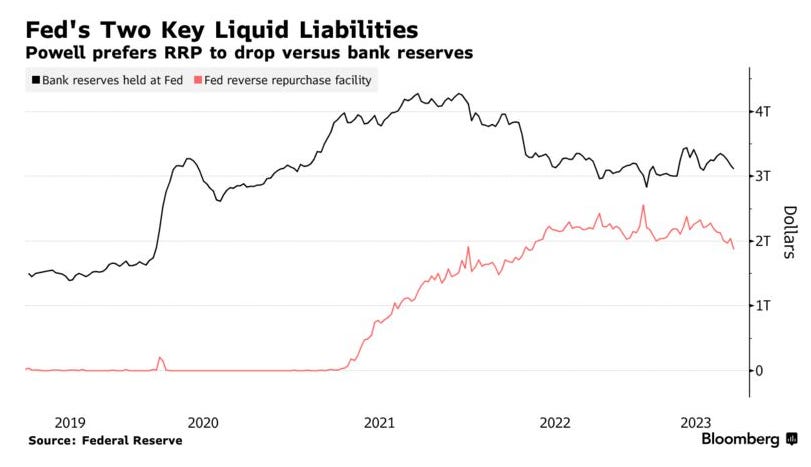

The U.S. banking system is complex and a side effect of these nonsensical policies was the effect on both bank reserves and the “reverse repo market” (RRP)which gave money market funds a place to park the money fleeing treasuries. Money flooded into the RPP while bank reserves fell.

The scale of the problem created is masked by accouting legerdemain which allowed major banks to carry treasuries at face value even as the market value of the securities tumbled as rates rose, something emphemistically called “hold to maturity” and presented at face value rather than market value on the theory that the risk of default was minimal. I am fairly confident that approach if tried would have failed in Turkey, Argentina, Zimbabwe or Venezuela, and it risks a similar outcome in the United States. The “mark to market” losses on hold to maturity portfolios on bank balance sheets is on the order of $1.8 trillion compared to total equity of the banking system of around $2.4 trillion. Banking was always a con game but has now become a Ponzi scheme.

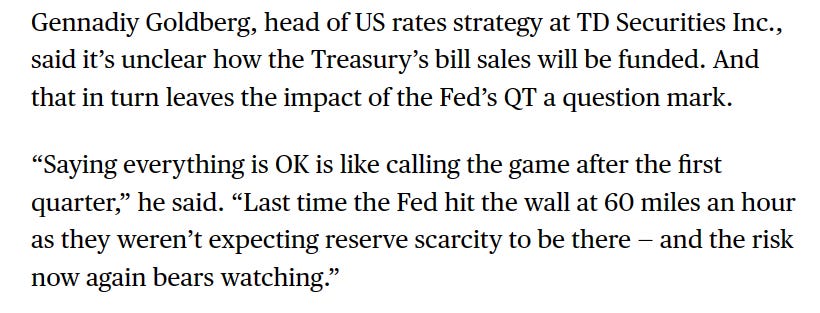

Quoting from a Bloomberg article, the risks are real and mounting.

Think the problem will prompt the Biden administration to alter course? Not likely. Hoping for a second term in the 2024 election Biden is doubling down on policies that don’t work and claiming they will. There is a tail risk of a banking crisis that will make the global financial crisis look like a walk in the park.

Can we assume that the Canadian banks are holding Govt. of Canada and Corp Bonds that are marked to market, instead of their real reduced value?

When we need to understand how the “ reverse repo market “ works in order to have a view on monetary policy ( which along with the economy Trudeau said .... they look after themselves) , then I think we have a serious problem.

I doubt 10% of our 338 MPs have even heard of the reverse repo market.

We’ve set ourselves up for “ experts” to bullshit us