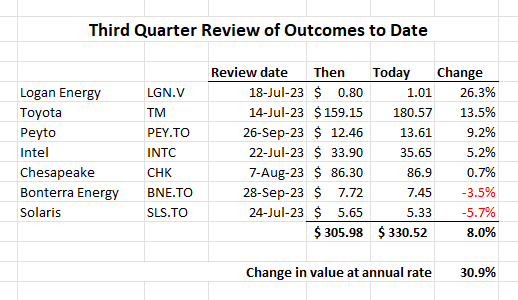

Stocks reviewed in Q3 - outcomes

Returns of 30% plus at annual rate in a tough market can't be all bad

During the July-September period, I reviewed a handful of stocks that I thought would interest readers, excluding reviews that covered more than one stock. I like to look back and see whether those reviews were out to lunch or turned out to be reasonable choices as investments. So far so good.

I think each of these names remains undervalued and should be good additions to portfolios despite the likely recession that seems to be anticipated at some point but waiting for it to happen is like “waiting for Godot”. Logan and Bonterra should benefit from recent strength in oil prices; Peyto and Chesapeake should benefit from firmer natural gas prices this winter and Peyto in particular from its recent acquisition of assets from Repsol; Intel is on a recovery path and Solaris keeps turning in excellent drilling results in its copper rich deposits; and, Toyota seems to be the only legacy automobile assembler with a sensible plan to produce both hybrids and electric vehicles that customers can afford and that will be profitable for Toyota.

Time will tell. It is always useful to review the bidding to see if the insights we share on Substack are of any value or just straws in the wind.

Your write up on Baytex will probably be the Most Profitable stock in 2024.

Michael

I wanted to acknowledge to you that your write up on Peyto was only done on the 26th of September and thus was an outstanding call on a company that has initiated for itself a transformative acquisition that has changed it's overall strategic position in the Canadian gas E&P market outlook. Your commentaries are always of great interest to me, and in general I agree with your views. = Richard Y. ( Queen's Comm. Hon's 1969).