Stock-based compensation in energy stocks does investors no favours

Investors in Canadian oil and gas stocks are treated to millions of dollars effectively paid to senior executives of their investee companies comprising “stock based compensation” justified by “aligning the interests of executives with the interests of shareholders”. It is a silly system, “alignment” is grossly over-rated, and it leads to poor decision-making by those executives.

Oil & gas stocks are unique in that the prices of energy shares follows commodity prices more than any other factor. Executives of oil & gas companies have no ability to materially affect commodity prices.

This chart shows the correlation between the energy section of the S&P 500 using XLE as a proxy and the WTI oil price. It is pretty clear that the trading prices of members of the XLE ETF rise when WTI rises and fall when WTI falls. Share based compensation simply pays executives for events in the world oil market and not for what they do in running the energy companies they manage. That reality is subject to a lot of abuse.

Source: LinkedIN

I have no objection to energy company executives owning shares in the companies they manage, but I think they should be paid in cash for the work they actually do and receive incentive compensation for achievements of goals for events over which they have some influence - operating costs, where to drill, what service companies to use, what local infrastructure is needed, meeting capital budgets, acquiring prospective lands, etc. Cash flow and profit are not metrics over which they have much control on a short term basis. If they want to buy shares of the company, they can.

It is useful to review the disclosed compensation systems of two key companies, one which has elements of a sensible compensation arrangement for management and one which clearly does not.

Peyto Exploration & Development

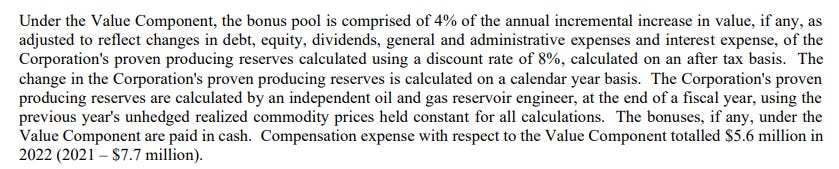

Peyto is a well-managed company by any measure. One element of its compensation approach is a reserves/value based bonus described in its Management Information Circular for the 2022 annual meeting as follows:

The $5.6 million bonus paid to selected executives was a reward for creating $140 million worth of additional reserves based on a calculation by independent reserve engineers and an 8% discount rate.

There is no doubt this is money well spent.

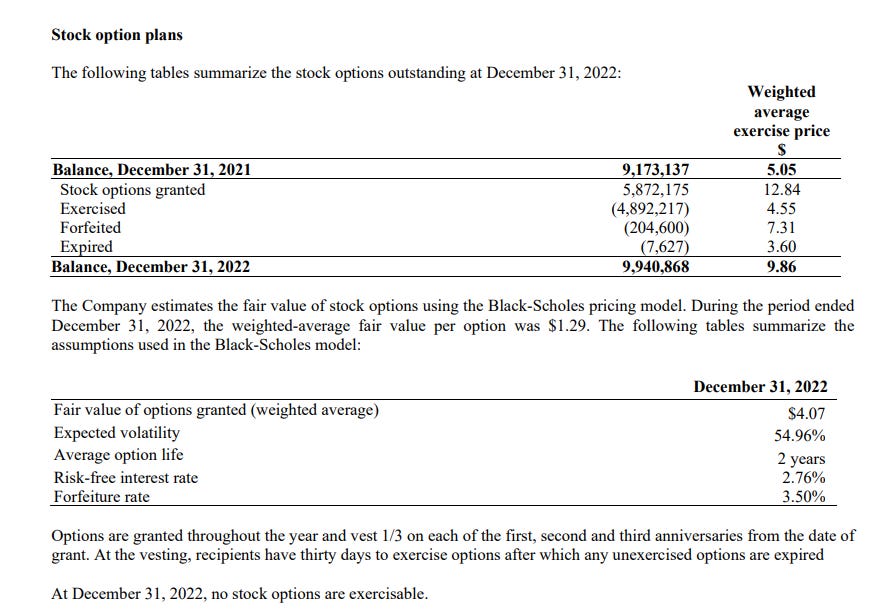

Peyto also has a stock option plan. The 2022 disclosure is set out below:

Peyto says the value of each of the 5,872,175 options granted in 2022 was $1.29 but reports stock based compensation for the year was $11.7 million. As popular as these options may be with managers, I think the board would have been better advised to award cash bonuses of $11.7 million and let the individuals decide whether to invest in Peyto shares or otherwise. Many would. What is important is not whether they own share but whether they are both motivate to do and in fact do a great job in running the show.

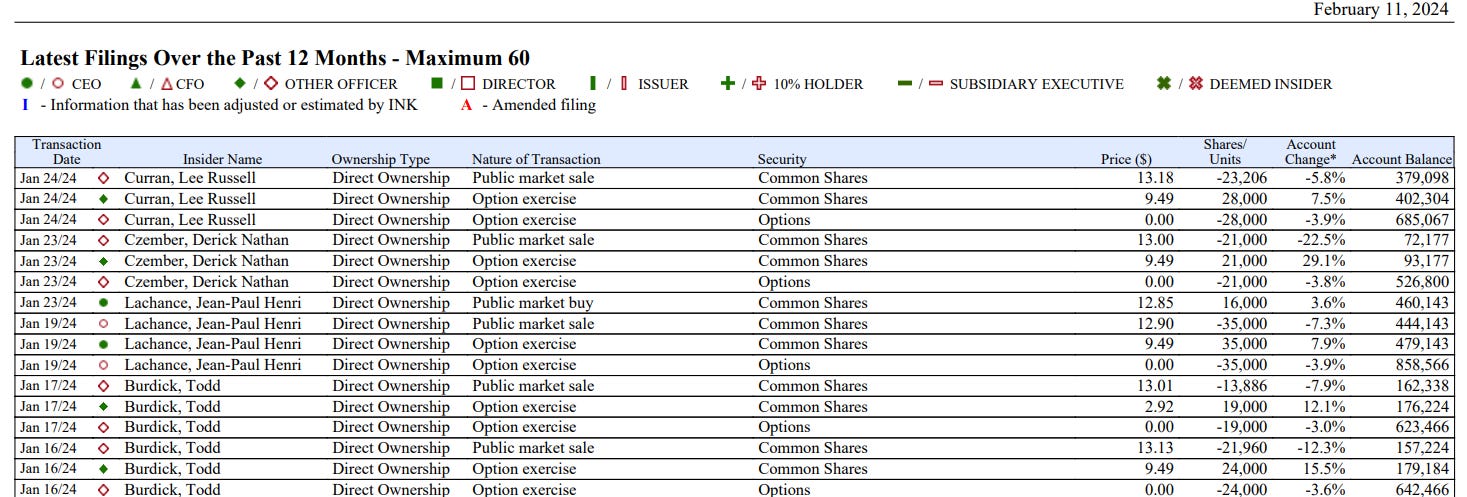

It is pretty clear that Peyto managers exercise their options and concurrently sell most if not all of the underlying shares when the options vest. Take Lee Curran for example. He exercised options on 49,000 shares at $9.49 and sold 44,206 shares at $13 to $13.18, for a capital gain of about $160,000 of which $80,000 is taxable and retained 4,794 shares and the $120,000 left after paying taxes on the gain. Would he have been less motivated to do a first class job (which I am confident he did) had he been awarded a cash bonus of (say) $375,000 (all taxable), paid taxes of $150,000 and used $65,000 to buy 5,000 Peyto shares (with zero dilution to Peyto shareholders leaving him with $160,000 and 5,000 Peyto shares? Why should his compensation be at risk to low commodity prices if he is doing a terrific job? If the price of natural gas falls, why punish him?

If the 49,000 options Curran exercised in fact cost the company $4.07 each for a total of $230,000 (after tax) the $375,000 suggested cash bonus would have been more or less the same cost to Peyto on the an after tax basis, the share count would not have risen, and Curran would be better off by several thousand dollars. There might even have been a saving in audit fees since some junior on the audit team had to spend a few $300 hours auditing the Black Scholes arithmetic, the continuity of the share count, and the preparation of the financial statements’ and information circular’s relevant sections.

Having said that, as option programs go, Peyto’s is sensible and well-disclosed. On balance, Peyto has an effective compensation system.

MEG Energy

MEG Energy is the opposite. The MEG Energy circular discloses a plethora of share-based compensation programs comprising stock optons RSU’s, PSU’s, and change of control benefits if stock making up control of the company changes hands.

MEG does little or no exploration, directs capital pretty well only to maintainance of its SAGD facility and operations, and has little or no control over the price of the Access Western Blend of oil it produces and sells. Its share-based compensation system is little more than a give-away to management for attendance. It seems designed only to make sure senior executives make millions of dollars.

MEG is a poorly managed company, in my opinion, and the self-serving compensation plans with generous “change of control” benefits are an egregious pillaging of the treasury that shareholders should reject. CEO Derek Evans seems to have made a career of being fired with a change of control payment of over $40 million at MEG, after reaping $7 million in compensation from Pengrowth leaving the company in 2018 on the eve of its 2019 sale to CONA for 5 cents a share on the eve of collapse after ten years with Evans as CEO. Evans even gets $6 million from MEG if terminated for cause. I would not be surprised if he spent his off-days looking for someone to bid for the company.

Pengrowth’s failure under Evans leadership arose from the toxic combination of too much debt and a collapse in oil prices. Apparently, the detailed measurements and objectives of the Pengrowth compensation system didn’t motivate management to prudently manage the balance sheet with only 10% of compensation targetting debt reduction. But at least the Pengrowth compensation system had sensible objectives for operations. There is no evidence that sort of “get paid for doing a good job” mentality made it into MEG.

Ultimately, you get what you pay for. In Peyto, you pay for a group of talented people who spend their time trying to make sure Peyto survives business cycles intact, grows steadily through those cycles, and pays out dividends to shareholders. In MEG, you get a group of people who seem more interested in their compensation than yours, make sure you can’t readily replace them except at great cost, and use free cash flow to buy back stock hoping it will make their options more valuable rather than pay you the dividends you have earned through your holdings.

Take your pick. It should be no surprise to readers than I hold Peyto shares and not MEG shares.

I was “lured” by my own guilessness into Pengrowrh many years ago. Foolish man child! The loss deductions helped just a bit. Now, older(80+) and a bit wiser thanks to M Boyd and fluidsdoc and now yourself, I would not even piss on MEG if the shares were burning! My recent best thing was VST which is now my largest position. During the storm several winters ago they got slammed by many on SA for losing money to keep their customers warm. I was proud to stick with them and commented that the whiners were just jerks. Character does matter and it is in hard times that you learn who has it, even though it might be better for all to not learn the lesson. Much appreciate this piece.

Insightful piece Michael. As always thanks for sharing your wisdom. Your point about MEG is very well taken, and I will have to take another look at Peyto. Again, many thanks!