Starcore International

A microcap call option on gold prices with a four year duration

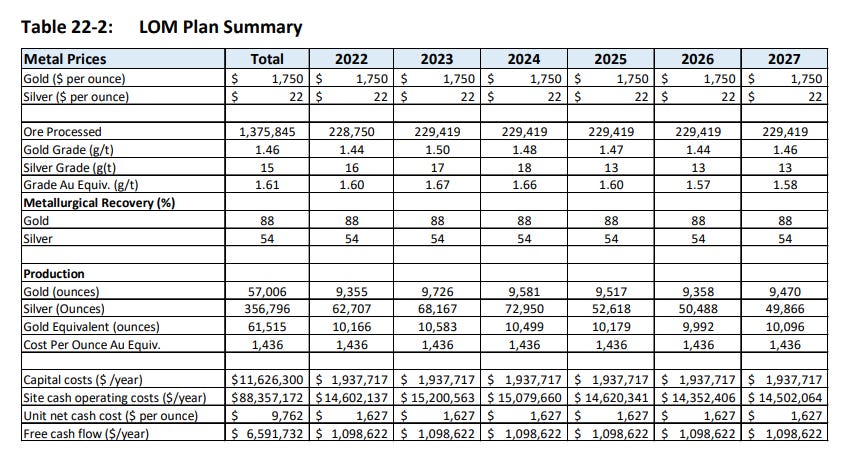

Starcore International Mines (SAM.V) is a tiny Canadian silver and gold producer with a handful of exploration projects that include the large El Creston molydenum and copper deposit and the Ajax copper deposit, both of which have the potential to become operating mines. But the current operations of the San Martin mine have limited remaining life. This summary from Starcore’s 2021 NI 43-101 Technical Report sets out the future of the mine as seen at that time.

A lot has changed since 2021, the most important of which is the run up in the gold price to about US$2,250 per ounce and the silver price to about US$26.50 per ounce. Assuming no material rise in estimated operating costs, this tiny mine should generate just over US$24 million in revenue in each year of its remaining life and operating margin of about US$7 million.

Debt free, Starcore has annual SG&A costs of about CDN$5.3 million (US$4 million) so over the next four years Starcore should generate about US$12 million of cash to add to its existing cash balance of about CDN$4 million, bringing the total to ~CDN$20 million.

Peanuts really, but with only 75 million shares outstanding, the per share value of the cash balance comes to about CDN$0.25 per share, about double the current price.

It is hard to get excited about a closely held company with such a limited future from its only producing mine, but a deeper look suggest option value.

When Mercator Minerals went into bankruptcy, the trustee sold Mercator’s Creston Moly subsidiary to Starcore for CDN$2 million. Mercator had paid $195 million to acquire Creston Moly, the assets of which were the El Creston mine and the Ajax Molybenum project in B.C. Maybe Mercator overpaid, maybe the mine has technical issues that will impede permitting, maybe El Creston will never get into production. The Ajax project has even further to go to become a mine. That is the lot of junior mines, only one in 6,000 of which ever make it into producing mines.

Nonetheless, I am intrigued by the potential. At the current gold price, Starcore is not bleeding money like so many juniors, and with annual gold output of over 9,000 ounces, a further run up in gold prices could be a bonanza. Anyone who thinks they can forecast gold prices needs therapy, but a lot of forecasts exist, some of which are summarized below:

In essence, Starcore is a short term option on gold prices. I doubt gold will come anywhere close to US$5,000 to US$9,000 an ounce (like some of the above forecasts) but at US$5,000 Starcore would generate almost US$30 million of cash in a year and at US$9,000 gold more like US$60 million.

Owning shares of Starcare is definitely a trip to the Casino, and most people leave casino’s unhappy, but for what it worth I bought 50,000 shares of Starcore a while back for CDN$0.10 per share. I expect I will lose that five grand, but I will let it ride until 2028 and see.