Spartan Delta could surprise investors with strong profit growth

Bellatrix Exploration is reborn and hopefully not stillborn

Bellatrix Exploration was a high-flying natural gas producer in Alberta with some of the most prolific gas fields in the Western Canadian Sedimentary Basin (WCSB). Unfortunately, management was too agressive and relied on debt to fund expansion exposing the company to the risks of a sharp drop in commodity prices. That happened and in October 2019 and a Court ordered transaction took place where the predecessor to Spartan Delta acquired all of the Bellatrix assets for nominal consideration. I was a Bellatrix shareholder at the time and took a bath on my shares.

One man’s loss is another man’s gain. Spartan Delta (SDE.TO) enjoyed the benefit of some $2 billion spent by Bellatrix over its life finding and developing its energy acreage. The result was that Spartan Delta enjoyed very strong capital efficiencies and very low operating costs having paid almost nothing for the Bellatrix reserves and infrastructure.

Barely a few months later, Spartan Delta completed three strategic acquisitions funded by concurrent public financings. In July 2021, the company made another large acquisiton of Velvet Energy Ltd. for $747.3 million, concurrently financed with share issues and some debt. This aggressive expansion put the fear of god into many investors, me included, owing to the rapid pace of the acquisitions and the almost frenetic pace of new financing. Was management heading down the same rabbit hole that had swallowed up Bellatrix and cost me plenty?

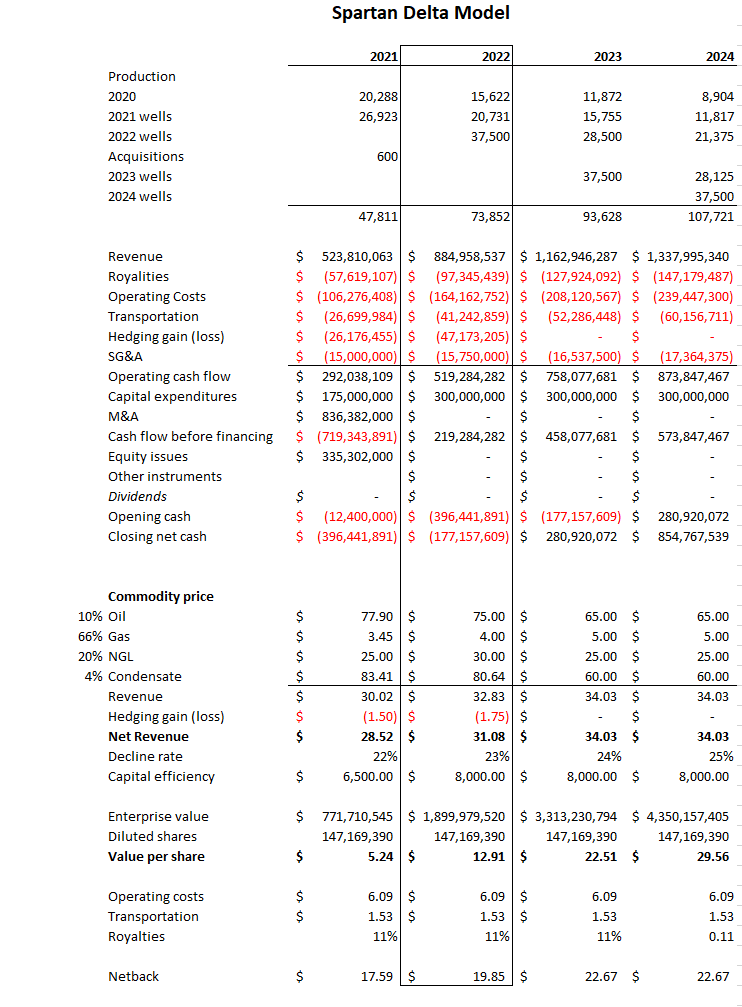

To answer that question, I built a model of the company’s operations laboriously poring through historic public filings by Bellatrix and the disclose by Spartan Delta.

Here is that model.

I was pleasantly surprised by the results. With natural gas and oil prices firm at present and expected to stay that way through the winter, Spartan Delta operatons pay down the new debt very quickly, ending 2021 with an estimate $400 million of debt (too much for my comfort generally) but with built in growth in 2022 capable of generating free cash flow of more than $200 million after funding a $300 million capital program. If prices remain firm, the company will end 2022 with debt below $200 million and production nudging 90,000 Boe/day and free cash flow in 2023 could be over $500 million.

The risk is high if commodity prices collapse before the end of 2022, but beyond that horizon the company will be quite conservatively funded and by my estimation have a value somewhere around $30 a share. That is a long way north of the current price of $6.75 a share. The company reports earnings for Q3 November 8, 2021 and should give an indication of how it sees the winter outlook.

I don’t pretend to be Nostradamus and I have plenty of scar tissue from investments in the energy sector that turned sour, including my ill-fated foray into Bellatrix. Notwithstanding, I like the odds in this case and purchased 95,000 shares at a price of about $5.00 a share. We will see if that turns out to be a bad bet (it woudn’t be my first) or a trip to a multi-million dollar gain in a relatively short period.