Solaris should bring sunshine to copper bulls

The exploration success keeps growing

Solaris Resources (SLS.TO) is a Toronto listed copper exploration company with a large and growing deposit called Warintza in Ecuador. Solaris is debt free and actively drilling out the resource to bring it to the stage where a mineable deposit is proven and can be financed.

Drilling to date has identified over 1 billion pounds of copper and an average grade just over one half of one percent. Inferred resources (highly speculative at this point) triple that number. Copper can be economically mined down to grades as low as 0.2%. This strike seems likely to be economical and eventually to become a mine. Solaris targets construction in 2025, although there is a lot of water to go under the bridge to get this small company funded to build a mine in Ecuador. Most development stage deposits never make it into production (only about 1 in 6,000 get built) and it is dangerous to buy early stage mines. But Solaris looks promising.

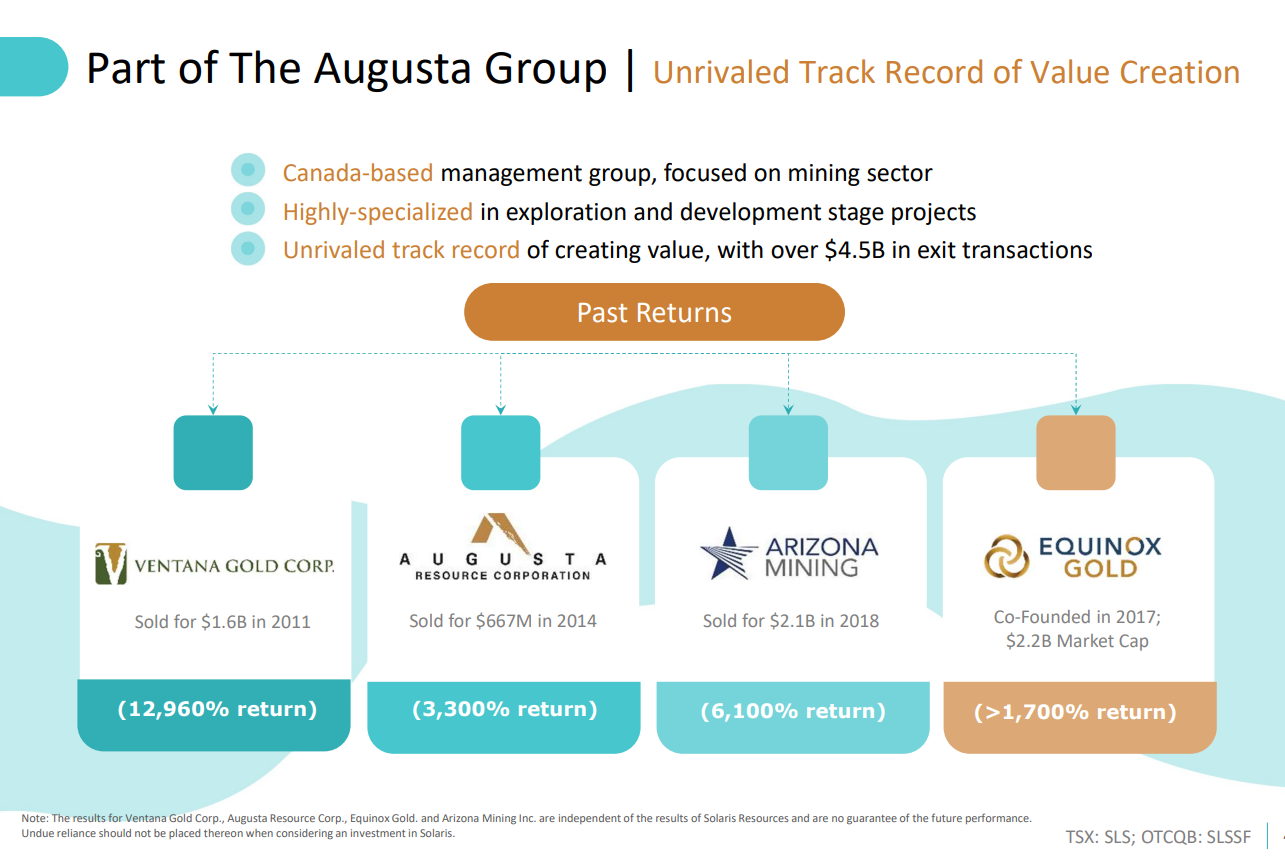

The sponsors of Solaris have a great track record of developing mines and shareholders include Lundin Mining (5%), Blackrock (9%) and management with 5%. Chairman Richard Warke holds 40% of the shares and is well known in the mining community having become a billionaire through his mining ventures.

Copper demand is likely to remain firm for several decades given the penchant for automobile assemblers to shift to electric vehicles (EV’s) from internal combustion engine (ICE) vehicles since each EV uses about three times as much copper as an ICE vehicle and there are over 1 billion cars on the road worldwide. If anything, there is more likely to be a shortage of copper production rather than a surplus for several years and high grade deposits will benefit from market tailwinds.

When it becomes clear that commercial production is likely, the company will either build a mine itself or become an acquisition target for mining majors. I suspect the latter given the track record of the sponsors but since the company has a market capitalization of about CAD$800 it seems within reason for the company to raise enough money to build the mine on its own. A better analysis awaits an updated NI 43-101 report on the Warintza project to include capital and operating costs which are not available at this stage of development. Warintza it is not the only Solaris project but at this point is the most interesting one and the only one I have given any thought to in writing this article.

Solaris has some analyst support with TD analyst Arun Lamba claiming a $20 per share “target” and an estimated Net Asset Value of $28 a share, but being careful to call the name “speculative” which it certainly is.

With SLS.TO shares currently trading below CAD$6 per share, I purchased a small position in the company and will keep a “watching brief” as it progresses. At this point, I think it likely the company is undervalued.

Michael, if it is not too much to ask and just out of curiosity, do you own other Copper stocks?