Soft natural gas prices in Canada will weigh on Advantage Energy

Dry gas and few hedges make the stock vulnerable as I see it

Advantage Energy (AAV.TO) is an analysts favorite with most advisors bullish on the name. In addition to its excellent acreage in the Montney, Advantage has a subsidiary called Entropy in the carbon-capture business which has captured the imagination of many climate nutters who continue to suffer from the delusion that CO2 causes climate change and spending billions of capital on carbon-capture makes sense. Over the long run, that subsidiary will become a stranded asset in my opinion.

But the company’s gas operations are well run and benefit from low costs. Advantage has about 14% of its 2024 output hedged at over CDN$4.00 a gigajoule which gives the company some breathing room but its exposure on the other 80% of output points to a tough summer.

Natural gas in Canada is currently well below CDN$2.00 a gigajoule and expected to stay there for the next few months until the combination of La Nina (expected this fall or winter) and the start up of the Kitimat LNG facility (sometime next year) add enough demand to tighten the over-supplied market. With storage levels near record highs at this point in the cycle, many expect low prices to deepen.

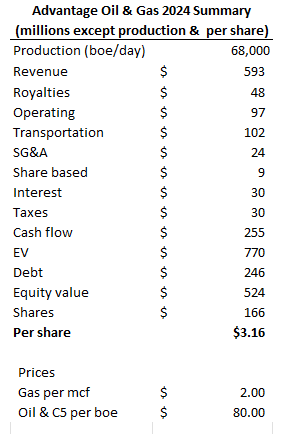

My model of Advantage’s operations at a natural gas price of CDN$2.00 a gigajoule suggests share value in the CDN$3.00 range while the market is paying about CDN$9.00 a share. I am assuming Advantage liquids output will fetch an average of CDN$80 per boe.

That makes Advantage a good short in my opinion, and since I am long other gas producers like Birchcliff and Peyto that pay dividends (while AAV prefers to buy back stock) I use a short on Advantage as a hedge against weakness in the other names and am short 35,000 shares.

We will see how that works out over the summer.