Saturn Oil or Surge Energy?

Offense or defense?

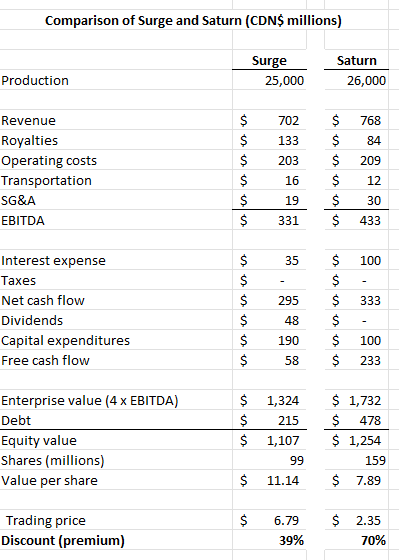

Saturn Oil (SOIL.TO) and Surge Energy (SGY.TO) have in common production of about 25,000 barrels of oil equivalent (Boe) per day and both have some merit as energy investments. A conventional valuation of both can be compared to begin the discussion. Both trade at a substantial discount to a 4 x EBITDA valuation.

A Black Scholes valaution of the reserves of each company tells a somewhat similar story, with the calculation return a per share value of Saturn of $16.69 and for Surge $14.06, with the Surge discount to intrinsic value 51% and that of Saturn 86%.

Both companies are undervalued in my opinion. With less leverage and a dividend, Surge is a safer investment and offers both reasonable downside protection and significant potential for gain. Saturn is higher risk and higher return. Which to choose (assuming you had to choose between these two and ignoring other options including not buying either) depends on whether your strategy is one of offense or defense.

In today’s energy environment, my choice is Saturn. Saturn debt is falling so fast it will soon be irrelevant even at a bit lower oil prices and Surge’s free cash flow will fall below the company’s current dividend if oil prices fall a bit more than 10% while Saturn will still have plenty of free cash flow to retire its high debt load.

As ever, a solid review by MB. Thanks for this.

I think royalties can be a timing a issue (so, lower rate earlier in development, rising later) and also location. As summarized in the Saturn Q3 MD&A:

"Royalties as a percentage of gross petroleum and natural gas sales increased for the three months ended September 30, 2023, reflecting increases in royalty rates for wells no longer eligible for royalty incentives. Royalties as a percentage of gross petroleum and natural gas sales decreased for the nine months ended September 30, 2023, which was primarily attributable to the Ridgeback Acquisition, reflecting lower associated royalties on acquired Alberta assets than the Company’s Southeast Saskatchewan Oxbow assets."