Reserves, not cash flow, are the value in commodity stocks

Common sense would help retail investors accumulate wealth

I have many interactions with energy and mining investors on the X platform, and benefit from the discussions most of the time and am bemused by them at other times. What is clear is that most of the #COM crowd think high stock prices are a benefit, that they can make the most money by “timing” their purchases and sales of stocks (i.e., trading) and that they can predict commodity prices. Many of them think a multiple of cash flow based on an assumed future commodity price is going to help them choose wisely, and look to charts and past stock price performance as having some predictive value. Really?

Commodity based companies exist because they hold mining or drilling rights to acreage under which there exists a finite amount of oil, gas, coal or metals (I am excluding forestry companies for the purposes of this article). When the particular company begins to produce a mining deposit or exploit and oil & gas reserve, it is on a track where without adding acreage it is going out of business, and its value is the economic rents it will obtain from converting the reserves to net income. Nothing else.

Here is an example of the silliness.

If natural gas prices fall to zero and remain there, $ARX $TOU $NVA $PEY.TO $BIR $PNE $CNQ.TO $SDE etc. would have values that reflected solely the economic rents from development of their liquids reserves and have values far less than current market prices. No one would develop natural gas so the only gas available for petrochemicals, electricity production or as fuel for SAGD would be associated natural gas from oil drilling, and the shortage in natural gas would soon see markets operate to either increase the price of natural gas to an economic level or drive the prices of alternative fuels like coal or oil higher. Markets work. The old adage is “the best cure for low commodity prices is low commodity prices”.

Ultimately, the decisions by management as to how to realize the greatest economic rents from the reserves they have or will create by drilling on the acreage they hold fall into two categories - one is “exploitative” where the company tries to get as much money from its reserves as quickly as regulations allow. This is often the case when commodity prices are high and management sees very high short term returns from drilling and producing. The other is “optimization” where management makes judgments as to how to produce the most output from their holdings over the life of the proven, probable or inferred reserves (what is actually there in whatever form).

Traders like companies that follow the “exploitative” strategy since it produces rapid rises in market prices for shares while prices are high combined with rapid declines in share prices when commodity prices fall. Since traders earn their money solely at the expense of other traders (but for any dividends they may receive while holding a particular stock) traders as a group lose money since secondary trading produces no value added but comes at the cost of fees and taxes. Few traders ever make much but they all think they will - a bit like the retired widows you see wearing adult diapers at the slots in Casino’s squandering every penny in the belief they will hit the jackpot.

Investors prefer “optimization”. Real wealth is created by holding a portfolio of dividend paying stocks that grow with the economy generally and in the case of energy stocks that are managed by teams that produce the greater economic rent from the reserves they are stewards of.

Share based compensation creates conflicts of interest (sometime conflated with “alignment” with shareholders, which is a valueless concept). Managers focused on share prices are akin to traders - they want to drive up the stock prices and sell their stock, hoping they can persuade their boards of directors to award them more options, RSU’s PSU’s and the plethora of other share-based units compensation consultants charge their employers for recommending so that management is assured of high income regardless of their competence. One thing is certain, they have no control over the world price of the commodity they produce and will be major beneficiaries of a rise in commodity prices even if incompetent at their day jobs.

Share based compensation encourages destructive initiatives like share “buybacks” which investors and management hope will increase share prices. Higher share prices will enrich the managers through their share based compensation, but tend to impoverish investors who must": (1) either divest all or a portion of their holdings to realize any benefit at all, and then pay taxes and fees on the associated transactions and (2) find another investment that is as good as the one they sold. Buybacks create value only when two circumstances obtain - they are, when the price of the buyback is less than the intrinsic value of the shares repurchased and when management has no profitable use for the money used in the buyback that holds a return greater than the best available return on investment available in the company’s capital program as yet unfunded. Traders love “buybacks” but investors don’t benefit from them unless those conditons are met.

In Nacho We Trust (@NachoTrust) seems deaf to reality and perhaps desperate to find some credence to his trading strategy. He is bearish on Birchcliff because the company pays a dividend for the time being financed by added debt. Franco Modigliani and Merton Miller won a Nobel prize in economics in 1961 for demonstrating that dividends werea financing decision irrelevant to corporate value. Birchcliff has modest debt and can well afford to pay its current dividend for the time being, has management that turns its minds to financial stability and demonstrated that it will raise or lower its dividends when needed to ensure financial strength.

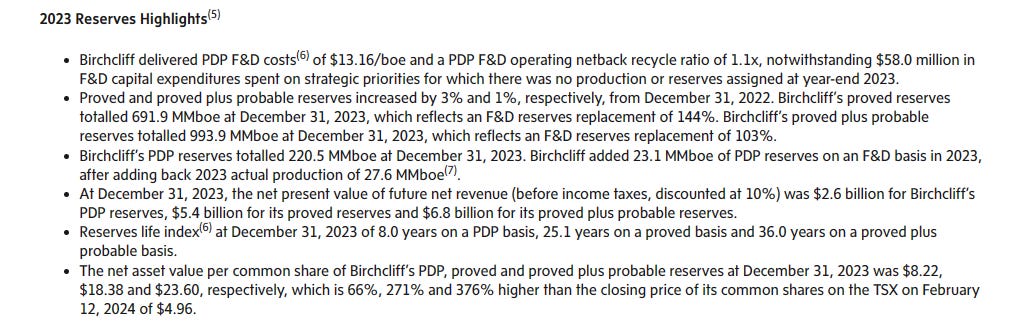

What Birchcliff also has sizeable natural gas and oil reserves which it reported at year end 2023 had an estimated value of between $8.22 and $23.60 per Birchcliff share based on the independent reserve engineer’s NI 53-101 reserve report.

What happens if natural gas prices go to zero for a short period? Unsophisticated investors will sell Birchcliff stock driving the share price down, I will add materially to my large holdings of Birchcliff stock, and when the dust settles I will be appreciably richer. That is what will happen.

I value Birchcliff shares using a modified Black Scholes approach to valuing its reserves (which relieves me from any assumption about future commodity prices other than that they will be volatile) and find they are worth over CDN$13 a share. I hope they do fall in price so I can buy more at discounted prices.

Like your thoughts on ITE , small Clearwater play, appears to be substantially undervalued based on reserve life .

Looks to be a potential takeover candidate.

Cheers

Dear Dr. Blair, would you be pls willing to assess the value of $VET in your model? I think it might be another hot name in #COM, which is actually a value trap. Thank you.