This follow up article begins with a chart from a thesis written by Otto Kiskinen which sets out global primary energy costs as a percentage of global GDP.

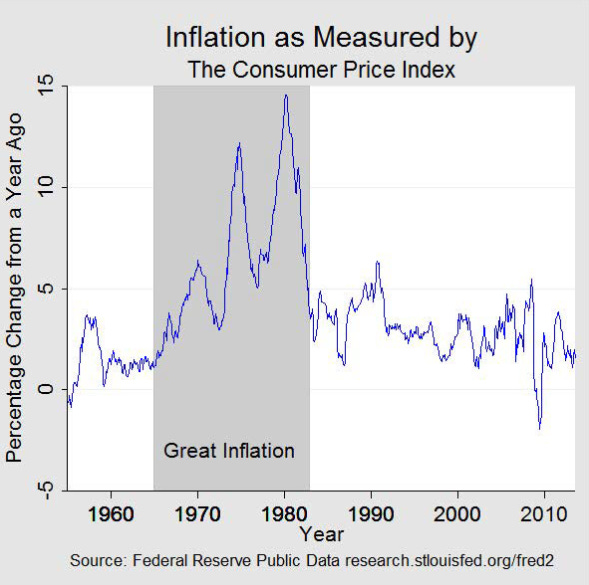

In the period from 1971 to 1982, energy costs rose from ~3% of global GDP to almost 10% of global GDP. The primary cause of that increased percentage was the price of oil following the energy crisis of the 1970’s which emerged in earnest at the time of the 1973 Yom Kippur violence in the mid-East and the OPEC oil embargo in retaliation for the Western backing of Israel in that conflict. Higher energy costs (driven by price and captured in the GDP measure) manifest themselves in inflation and this was obvious in the 1970’s when the eight percentage point rise in global energy costs relative to global GDP saw inflation run about from 6% in 1973 to ~14% in 1982 according to Federal Reserve public data.

The oil price to inflation linkage is not immediately seen. It takes a while for higher energy costs to become passed on to consumers in price as businesses deal with the costs of production and transportation (that have major energy components) by raising prices to their customers and consumers deal with higher costs to heat their homes and fuel their vehicles by demanding higher wages. This becomes a classical cost-wage-price inflation cycle. The subsequent abatement in energy costs as a percentage of global GDP following an ease of tensions in the mid-East saw inflation fall in parallel. The correlation in this case evidences causation and is too tight to ignore.

Central bankers want to claim that interest rates are effective in controlling inflation by reducing economic activity. They don’t comment on how effective rates would be be in controlling inflation if society were not indebted and did not rely on borrowing either at household or government levels to fund consumption. They largely ignore fiscal policy as a contributor and totally ignore energy geopolitics most of the time. Government intervention in the economy affects inflation at the margin but the primary driver of inlation today and 50 years ago is not monetary or fiscal policy but energy policy with monetary and fiscal policy introducing short term volatility and exacerbating the inflationary force of energy costs. Drive up the costs of energy and inflation will result regardless of fiscal or monetary policy as the higher energy costs become imbedded in the prices consumers pay for goods and services.

The most recent outbreak of rampant inflation after decades of relatively benign inflation followed a rapid increase in global energy costs as a percentage of GDP in 2021-2022 when Bloomberg reported that the ratio of energy costs to GDP globally had almost doubled to 13% from about 6.5%. In parallel, inflation surged to the 9% range in North America from a 2-3% range in the prior periods. Think about it - energy costs rise 650 basis points as a percentage of GDP and inflation surges by a similar amount, more or less. The recent abatement of inflation resulted from the decline in global oil prices from the US$120 per barrel range to the current US$80 per barrel range, not from monetary or fiscal policy which at best tinker with the market forces and fuel heated debates at cocktail parties.

Once higher energy costs kick off an inflationary cycle, wage demands and price pressures on businesses and in turn consumers cause volatility in prices. Central bankers and so-called “experts” - mostly economists and financial advisors and their ilk - begin to analyze the first derivative of the changes on a daily basis speculating on what action the Fed will take, whether a recession is imminent or whether there will be a “soft landing”. They ignore the root cause of the problem almost in its entirety - inane climate policies which lead to thoughtless energy policies which manifest themselves in shortages of fossil fuels which comprise about 80% of the world’s energy sources.

CO2 is harmless but the pretense that it causes climate change persists and has two inescapable consequences - first, it permits energy investors to enjoy very high returns and second, it fuels persistent inflation met with central bankers raising interest rates rather than governments reducing spending or encouraging added fossil fuel supplies. Recession may follow the higher rates and provide temporary relief as demand falls, but inflation will resume in any expansion unless the gap between energy supply and demand is filled with expanded output of fossil fuels. This self-reinforcing cycle is made worse by political ideology with leftists promoting the specious “climate change” narrative and consumers bearing the burden of their ineffective policies in energy costs, food inflation, higher interest rates and emotional activists either gluing themselves to roadways or throwing paint on the art works of masters in museums decrying a lack of progress on climate change (which it is impossible to control by reducing emissions of harmless CO2) or protesting food and energy costs forcing them to choose between warm homes and sufficient food in winters.

It is hard to imagine a worse set of outcomes from progressive ideology short of outright tyranny and global socialism. Yet here we are, and half of Americans and a large minority of Canadians support the progressive political parties despite their toxic effects on their lives and livelihoods. If the next round of elections does not bring about a shift to the center and the return to common sense in the halls of power, economies will verge on collapse and there will be another financial crisis as bond investors eschew treasuries and the massive deficits of United States and Canada cannot attract enough lenders to keep the charade alive.

Hmm. Normally I am in lock-step with you. A bone to pick in this one however. I associate vast increases in the money supply following Covid with inflation. The price of everything rose due to debasement of the currency and supply chain disruptions. What am I missing?