Policy makers get energy policy wrong

But sometimes stumble into the right outcomes in spite of themselves

A lot of time is spent debating the Fed’s next move on interest rates, but the real determinate of future global economic growth is the price and availability of reliable sources of energy. Without energy, nothing works.

Robert McNally’s excellent history of the boom and bust cycles of the oil industry (Crude Volatility, Columbia University Press 2017) since oil was first discovered provides details on the price of oil from 1859 to the present and a well-reasoned argument as to why the nascent oil industry wildcatters, their successors and governments shared primary objectives in terms of energy for at least the first century - to keep prices high enough to make it profitable to produce oil. The Texas Railroad Commission (TRC) was a regulatory cartel, the handshake agreements between the emerging oil producing companies and subsequent formal agreements (often at the instance of John D. Rockefeller) among larger producers, the so-called “Seven Sisters” cartel and ultimately the OPEC cartel all had the dual objectives of price stability by restricting supply on the one hand and maintaining spare capacity to prevent shortages from causing spikes in the price of oil and resulting economic damage that would precipitate the next slump.

Private enterprise and government regulation shared the same objectives. Their tacit cooperations kept oil prices low enough to fuel economic growth while high enough to encourage production. From 1871 to 1971, the price of oil ranged from a few cents to $5 a barrel with surprising stability despite the competing forces of the profit motive on the part of producers and produced economic growth without inflation with limited intervention on the part of governments and their regulatory bodies. Many companies were born and died with the swings in price, but the industry continued to grow and with that growth the industrial economy emerged.

In a nutshell, the industrial revolution only took place because there was a confluence of industry and government objectives. I like the “nutshell” analogy since in today’s world it is “climate nutters” who have driven governments to enact stupid energy policies that have the same underlying motives but are distorted by ideological goals rather than economic goals.

There is an abundance of hydrocarbons on Earth today, and there is no danger of them “running out”. “Peak oil” is one myth. Hydrocarbons remain the most cost-effective source of energy by a wide margin. There is no evidence that hydrocarbons when used as fuel result in emissions that are harmful and the claim that atmospheric CO2 levels rising above the current level of 430 ppm by volume is some sort of threat are purely ideological and are devoid of any consistency with the laws of physics. That theory is another myth.

But perhaps, if seen through the same lens as energy policies for the first century of widespread use of oil & gas, today’s policies (while clumsy) may be achieving the same goals at least to some extent. The abundance of hydrocarbons which can be produced at low cost would almost certainly result in oversupply if there were no barriers to increased production. Even a small oversupply manifests itself in a plunge in prices. Similarly, even a relatively small shortage will see a surge in prices. McNally makes this point throughout his book and no sensible person can argue otherwise.

The U.S. Strategic Petroleum Reserve (SPR) acts as an inventory buffer, not to provide energy for military purposes (despite claims that it is for military purposes) but as buffer to preclude shortages from driving prices so high economic growth is stifled. President Biden’s 2022 releases from the SPR were for precisely that purpose when oil prices reached US$140 a barrel and both fueled inflation and had the potential to strangle growth.

Royalties are often imposed on oil producers in addition to income taxes and energy consumers in Canada are burdened with HST and a silly “carbon tax”. These are barriers to excess production by acting as drags on demand, and by reducing demand are keeping industry players in check by discouraging over-production. Anti-pipeline legislation (like the Impact Assessment Act) and climate activist protests curb supply. Both forces tend to keep supply and demand in a loose balance.

In the absence of these policies and acts, there is a strong likelihood that the industry cycles would be severe. The 1973 Arab oil embargo demonstrated how much impact a shortage of supply could have on markets, nearly quadrupling the price of oil in a matter of weeks. The COVID-19 pandemic demonstrated the degree to which a small reduction in demand could have on oil & gas prices (oil prices fell almost 70% in a matter of weeks), driving many producers to the edge of failure and the weakest into bankruptcy.

Political leaders rely on votes to retain their offices. Few would enact a policy with the overtly stated objective of causing economic harm to a world industry or purposely to create hyperinflation , yet without the threat of such harms the energy industry has the power to fuel rampant inflation or put the brakes on economic growth. It is almost certain the oil & gas industry would swing between those extremes in the absence of government intervention. It is easier to tell the electorate your policies are to protect national security or save the planet than to tell the truth - that energy policies are a balance to ensure stable prices and sustained economic growth and that “climate risk” is nonsense. So lie is what they do.

As McNally writes: “Oil is and will, for the foreseeable future, remain the lifeblood of advanced civilization.” (McNally, page 3). But vicious cycles in energy prices may be with us for some time, as McNally’s book suggests. McNally sees global oil prices fluctuating in a wide range from as low as $30 a barrel (when most drilling would stop) and as high as $130 a barrel (when energy’s contribution to global inflation would be significant).

Energy investors need keep that in mind when they vote in the U.S. Presidential election this November and the Canadian general election in 2025. The right path is to shift away from the extremes and temper the socialist desire to use restrictive energy policy based on specious “climate policy” as a tool to promote global socialism while restraining the conservative desire to “drill, baby drill” - a theme of the Trump campaign - which risks resurgent inflation.

I find it interesting that investors who actively comment on Twitter lament oil prices in the US$70 range and natural gas prices in the US$2.50 a gigajoule range as if they were catastrophic. Oil is quite profitable to produce at US$70 a barrel and many natural gas producers can operate successfully at US$2.50 a gigajoule. The problem is not commodity prices, it is unreasonable expectations. Investors who become agog when oil prices are over US$100 a barrel or apopletic when a natural gas producer cuts its dividend live in a fantasy world thinking it is about them.

Here are some reference points. At $70 a barrel, an oil producer who can add a flowing barrel for $20,000 of capital and has an all-in cost of lifting, royalties, transporation and administration (“all-in cost”) of $30 a barrel can achieve should realize first year cash flows of about $15,000 per barrel declining at (say) 25% per year owing to natural decline. At $2.50 a gigajoule (or ~$21 per boe assuming 10% liquids) a natural gas producer with a capital efficiency of $12,000 per Boe and an all-in cost of about $10.00 a Boe will receive cash flow of about $4,000 in the first year declining at (say) 25% owing to natural decline, and likewise be quite satisfied with the level of profitability.

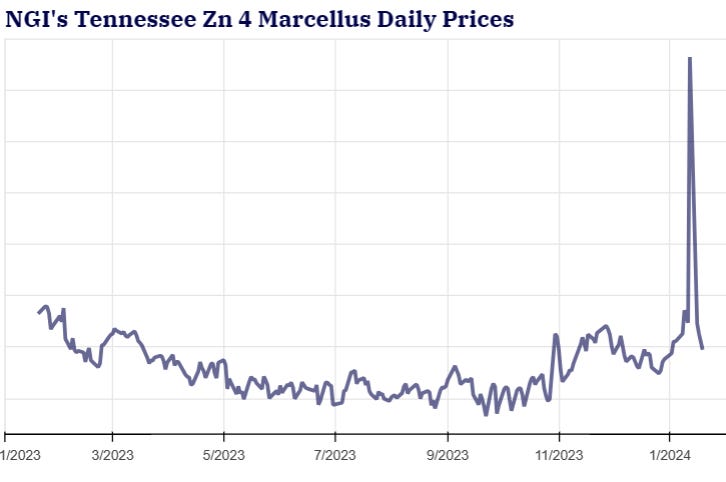

I am always amazed at how close in time euphoria can turn to despair for those who think they have the ability to forecast commodity prices. This chart tells the tale.

Source: Natural Gas Intelligence

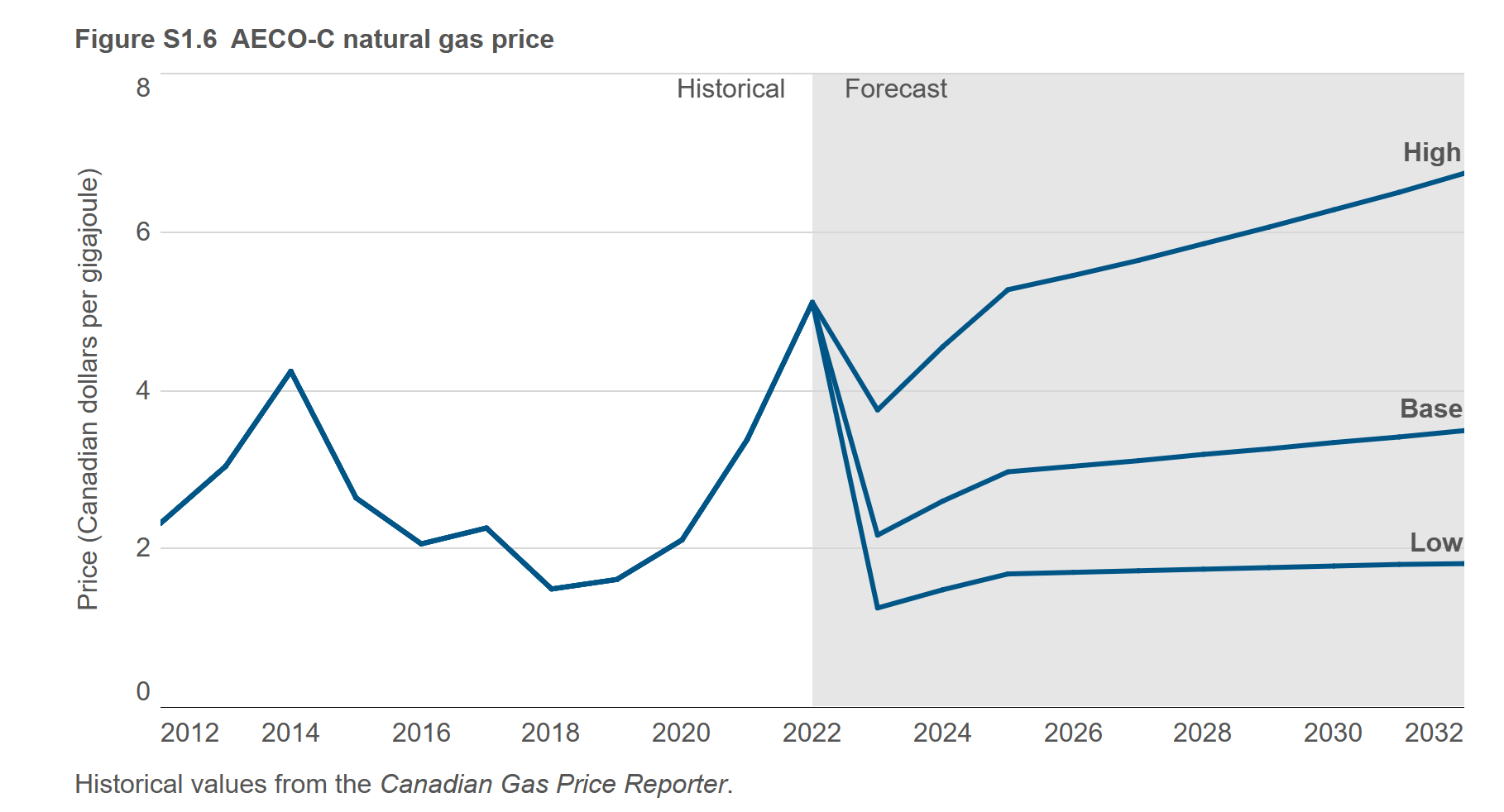

The Alberta Energy Regulator provides forecasts of natural gas prices which make a lot more sense than “strip”. Here is the most recent forecast which says that AECO natural gas prices are likely within the range of CDN$1.75 to CDN$7 per gigajoule over the next decade with 2024 likely weaker than 2023. Given El Nino, that seems more likely than not.

The lessons are simple. If you can’t stand the volatility, buy bonds and stay out of the oil & gas space. If you are going to invest in energy, buy low cost producers with clean balance sheets when commodity prices are low and don’t waste time checking the stock price five times a day. Stay calm, exhibit patience and over business cycles you will earn plenty of money. Try to time the market and bet you can forecast commodity prices or get deluded by sell-side analysts who value companies based on so-called “strip” prices (which are about as valid as astronomy, tea leaves, palm reading or tarot cards) and then lever up thinking this is your shot at wealth, prepare for disappointment. Energy investing is not for sissies.