Peyto Exploration is my best bet for 2024

Low costs, fast growth, capital and dividend well covered by hedged cash flow

Scotia iTrade is calling for Peyto (PEY.TO) to reach CDN$23 a share within a year and notes the company’s capital program and dividends are covered by the portion of production protected by Peyto’s hedge book, so risk of a dividend cut or a compromise to its capital program won’t happen this year

Source: iTrade

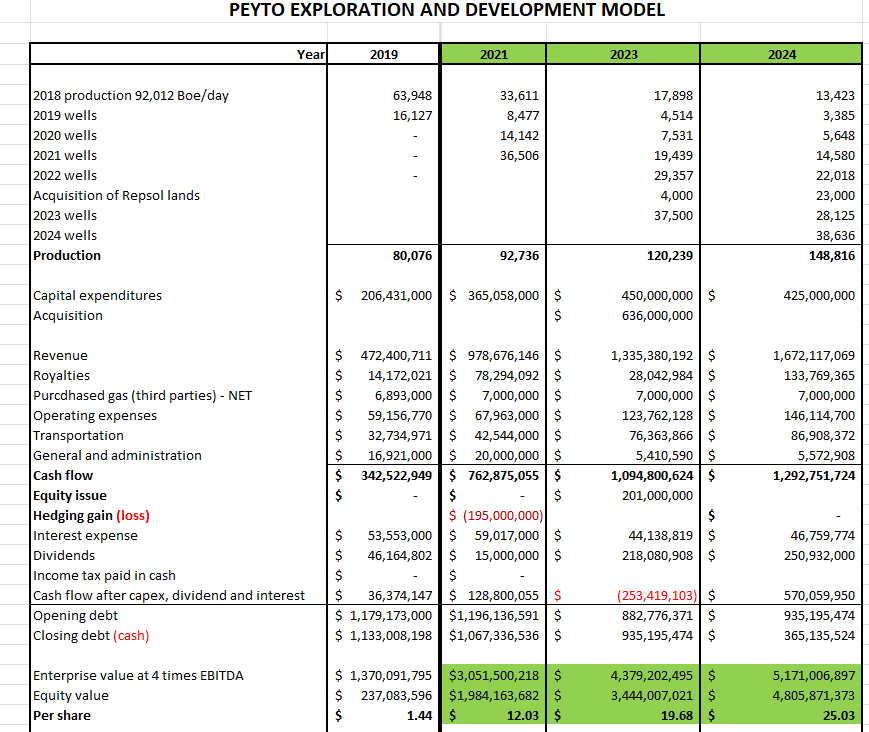

I model somewhat better outcomes. Note the production figures are end of period annual rates, not average for the period, so the valuation metrics are based on run-rates rather than calendar year reported outcomes.

Peyto’s Repsol asset acquisition provided lower decline rate output and better capital efficiencies on DCE & T capital expenditures. I see rapid declines in debt while continuing to pay a dividend of about 11%. Beyond 2024, further growth is likely but the economics will depend on commodity prices at the time.

The numbers incorporate a lot of assumptions and can be materially wrong depending on actual costs, availability of rigs, tie-ins, etc. but they are a reasonably good projection of the potential. Peyto should hit 150,000 boe/day sometime in the next two or three years and if the company continues to operate to historical standards the stock has a good chance of doubling in value within that time frame.

I see Peyto stock as deeply undervalued.

Dear Dr. Blair, thank for another great article.

As of 2024, I think, you are right. Peyto should be ok due to hedges.

Further years are a big question, as Natgas can get under continuous market pressure.

FYI New PEY presentation, showing Cascade drawing in Q1, with 100% starting Q2

https://www.peyto.com/Files/Presentations/2024/CorpPresJan2024.pdf

see page 26