Open Text should be in your future

Profitable, growing and undervalued

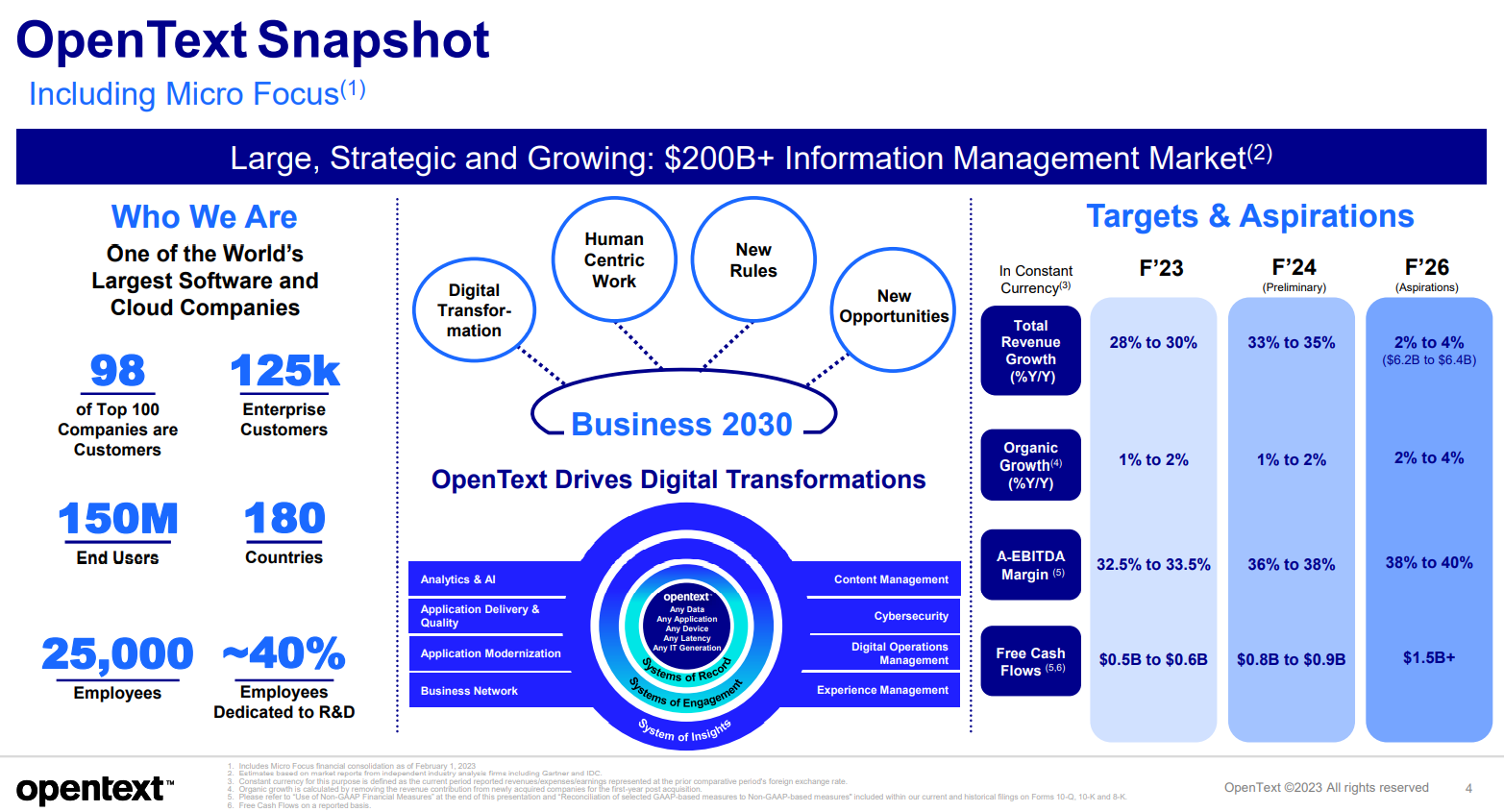

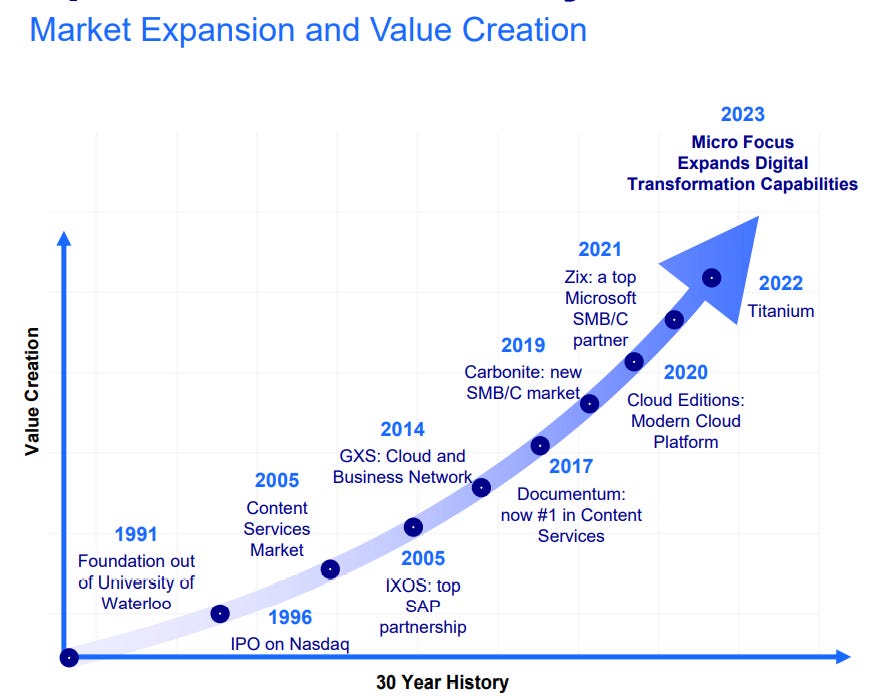

Open Text (OTEX) is a Canadian technology company, a rarity since Canada sports very few companies that qualify “technology” companies. The company provides a wide range of document management applications. Founded in 1991 as the outgrowth of a University of Waterloo project to index the Oxford dictionary, Open Text was at one time ahead of Google in Internet Search, but the company took a different tack. Today, it is one of the world’s information management software companies with a blue chip list of clients and with plans to triple free cash flow from about $500 million in 2023 to over $1.5 billion in 2026.

I first heard of Open Text from the late Ben Webster, President of Helix Investments, who was a founding shareholder of the company I founded in April 1984 - The Enfield Corporation Limited (“Enfield”). Ben had a lot of good things to say about Tom Jenkins, who was President of Open Text for many years, then Chief Strategist and today Chairman of the Board. Tom’s leadership was key to the company’s success.

While I was in the process of founding Enfield, Ben let Fred Sorkin share an office at Helix next to mine, and Fred created Hummingbird Communications, Inc. that developed into a major public software company, itself eventually acquired by Open Text. Ben died of lymphoma December 13, 1997, a significant loss to Canada and to me personally.

Open Text is undervalued by a wide margin. Today’s quarterly report shows the potential and the 33% drop in the share price from $69 to $47 in the past 2 years creates the opportunity, and today’s sharp rise in the share price suggests the market is waking up to the value of the company.

In my opinion, for whatever it is worth, I believe the company has a value of about $55 to $60 a share or a market capitalization of somewhere around $15 to $16 billion. The current 3% dividend is a bonus, since Open Text’s real value is its ability to successfully find, acquire and integrate other information management software companies and create synergies between its suite of offerings. I would expect to see the dividend increase over time, and understand the company has a “buyback” program as well. $16 billion is ~10 times 2026 free cash flow if the company’s published projection of $1.5 billion plus is realized. That projection is based on integration of recently acquired Micro Focus (with synergies estimated by Open Text at about $400 million) and organic growth in the low single digits.

Open Text has a long history of growth through market expansion.

Readers interested in the company’s prospects should start with a read of their recent corporate presentation. It is an impressive story.