Modern valuation methods help avoid losses

Valuation of mining stocks as "real" options pays off

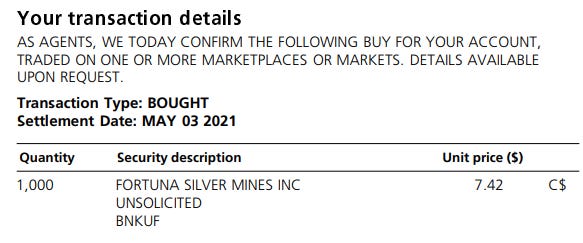

On April 26, 2021, I came across a press release that Fortuna Minerals (FVI.TO) had agreed to acquire Roxgold, and the release was chock full of positive metrics, so I bought a thousand shares as an opening position while I did more due diligence on value. At first blush a small capitalization gold miner promising to produce 450,000 gold equivalent ounces per year at an all in sustaining cost of US$950 per ounce was appealing.

Fortuna Silver had been around for a while and I presumed the market price was in the ballpark of sensible value for its then existing mines so future gains would have to come from the Roxgold acquisition or higher commodity prices. At the $7.42 per share price I paid and with 290 million shares outstanding post acquisition (including the shares issued to settle the Roxgold purchase), Fortuna had a market capitalization of about $2.2 billion and had effectively paid $1.1 billion for Roxgold according its press release, and the company expected annual Earnings Before Interest Depreciation and Taxes of $500 million from the merged company.

Since commodity prices are volatile and are the key determinant of value of a mining company, I completed a valuation of Roxgold using Black Scholes and treating the Roxgold deposits as a “real option”. That analysis indicated that Fortuna had paid CAD$1.1 billion for a mine with a value of about US$320 million or approximately $400 million Canadian.

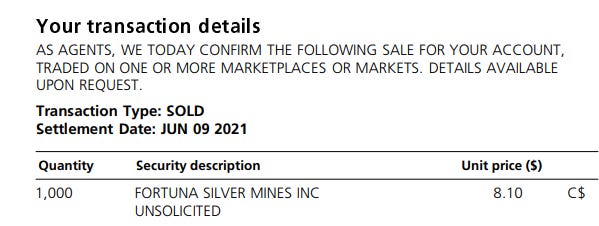

I immediately sold my shares realizing a price of $8.10 and pocketing a small gain.

The market soon caught up to the value destruction arising from the acquisition and Fortuna shares fell to trade in the CAD$4.00 to $5.00 range where they have languished ever since.

Modern valuation techniques can make you money and save you money. Successful investors ignore the hype, do their homework, and move quickly to cut losses if they have blundered.