Mike Rose or Terry Anderson?

Why management matters to me, and likely should matter to you

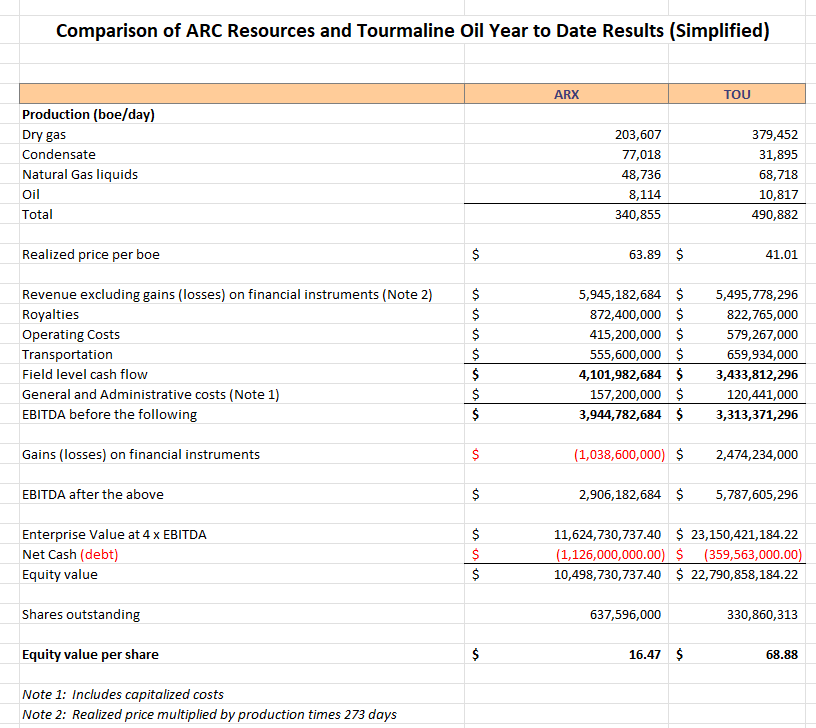

Tourmaline Oil (TOU.TO) and ARC Resources (ARX.TO) are two giant natural gas producers in Western Canada, both with outstanding asset bases. Here is a comparison of their year to date September 30, 2022 results, simplified by omitting incidental items that don’t materially impact the comparison:

Investors should note that the liquids rich composition of ARC Resources (ARX.TO) production produces both higher revenue and higher cash flows than the natural gas weighted production of Tourmaline despite Tourmaline’s higher production on a Barrels of Oil Equivalent (Boe) basis. Based on operating economics alone, ARC should have a trading Enterprise Value (EV) about 25% higher than Tourmaline and a share price about double the current trading price of ARX.TO shares.

The difference is management, pure and simple.

ARC Resources year to date September 30, 2022 lost over $1.1 billion on its “hedging” activities including all so-called “financial instruments” used to mitigate risk. Tourmaline Oil earned almost $2.5 billion on its similar “financial instruments”.

Management matters. Both ARC and Tourmaline have excellent assets. Both have competent operating management. But the two companies financial management is materially different and my money bets on Mike Rose and not Terry Anderson despite the extraordinary quality of ARC’s asset base. If that changes, I will be a buyer of ARX.TO as well as TOU.TO but not today.

Investors should also note that in today’s energy market, both ARC and Tourmaline are trading at an EV multiple greater than 4 x EBITDA (although there are good arguments in both cases to diverge from the traditional multiple of 4 x EBITDA). With the prospect of a recession looming, it is likely that both companies are “overvalued” in the market despite the throng of energy investors who are urging “buybacks” and claim the respective shares are trading below “intrinsic value”. With nothing but respect for the opinions of these investors, they typically have little expertise in business valuation and rarely go beyond applying a multiple of EBITDA to current operating results (which I have done in this article and comparison).

It made me wonder why financial experts bother completing the work to become Chartered Financial Analysts or Chartered Business Valuators, or why anyone would (as I did ) pay to take the graduate course in Advanced Valuation at the New York University Stern School of Business, when all they had to do was follow a few members of the Canadian Oil Mafia on Twitter and get valuation inputs from people who are certain they know the “intrinsic value” of their favorite energy names and have formed a throng of investors urging increased “buybacks” by Canadian energy companies. Who knew Twitter would be so useful?

These two companies remain excellent investments. Over time, either management will change its mind about “hedging” or the directors will change their minds about management and ARX.TO will start to exhibit its underlying potential. I expect that will happen sooner rather than later since much of the adverse “hedging” was inherited with the Seven Generations acquisition and as debt disappears the temptation to “hedge” will diminish. The best hedge of all is a debt-free balance sheet and low costs.

Similarly, the benefits TOU.TO received from its “financial instruments” are not always repeatable and that company’s stock will ultimately reflect is steady growth, fortress balance sheet and sensible dividend policies and grow into its market valuation even if it is somewhat overvalued today.

In both cases, the tailwinds of growing demand for LNG worldwide, the start up of the Kitimat LNG facility, and the domestic demand for condensate (much of which is now imported), and the likelihood the toxic Liberal party government will be ousted at the next election will be factors pointing to profitable longer term growth and supportive of higher multiples for either stock. Investors owning either stock can sleep at night.

NGas hedges from their new presentation, going lower in 2023, Seven Gen acquisition was in 2021

See page 19

https://www.arcresources.com/wp-content/uploads/2022/11/November-2022-Investor-Presentation.pdf

A lot of the people that love buybacks have never seen, ( or don't remember) how quickly things can turn around in the oil patch, and how important it is to have a clean balance sheet when that happens. I will take dividends over buybacks any day.