MEG Energy seems undervalued

Markets overreact to the company's debt

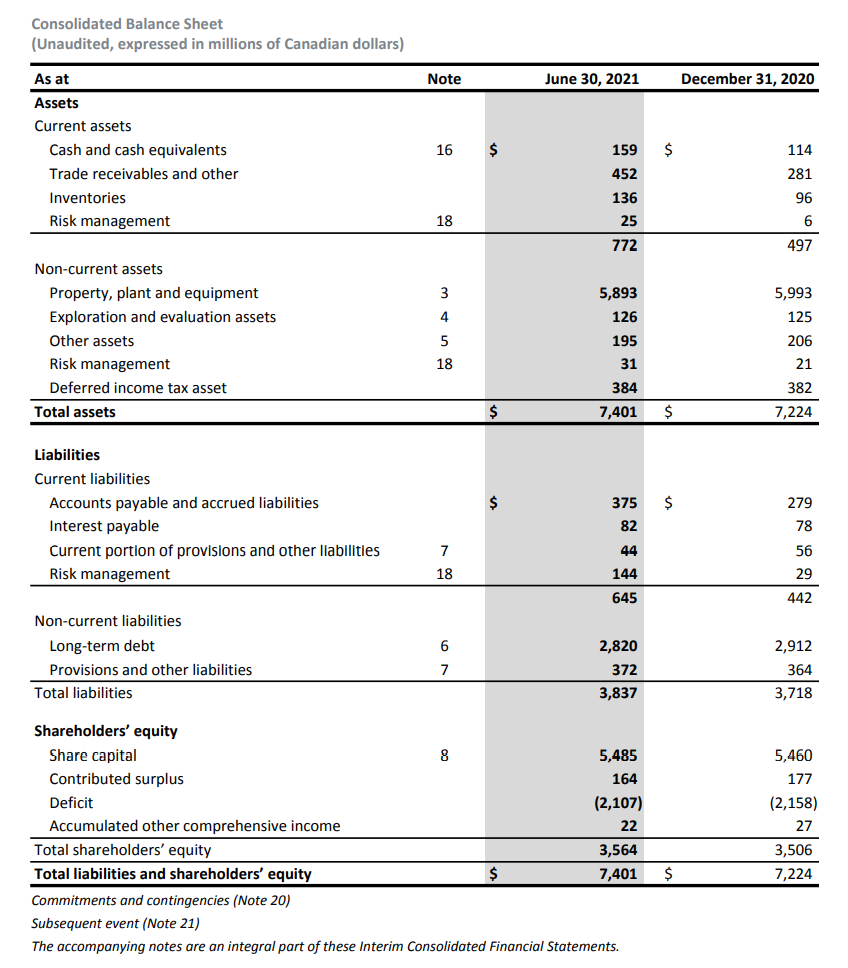

MEG Energy (MEG.TO) is trading at about $9 a share and with 307 million shares outstanding has a market capitalization of $2.7 billion. The company has debt and third party liabilities of $3.8 billion. The market appears concerned about the prospects of a financial liquidity crisis despite the fact that the average maturity of its liabilities is 3.4 years (3 years for $0.6 billion; 5 years for $1.5 billion; 8 years for $0.7 billion; and, current liabilities and provisions comprising the balance). MEG’s June 30, 2021 balance sheet is reproduced below.

With oil prices running at about $85 a barrel in Canada, MEG is rapidly paying down debt from free cash flow (that is cash flow after capital outlays). Market analysts are divided about the prospects for MEG’s future based on my reading of a few dozen research reports, but none of those reports values MEG based on modern valuation theories for highly indebted companies, which assesses the value of the equity in the company as a call option on its assets with a strike price equal to its debt and a “time to expiry” equal to the average maturity of its debt. Options can be valued using either the binomial probability theory or the Black Scholes option valuation model.

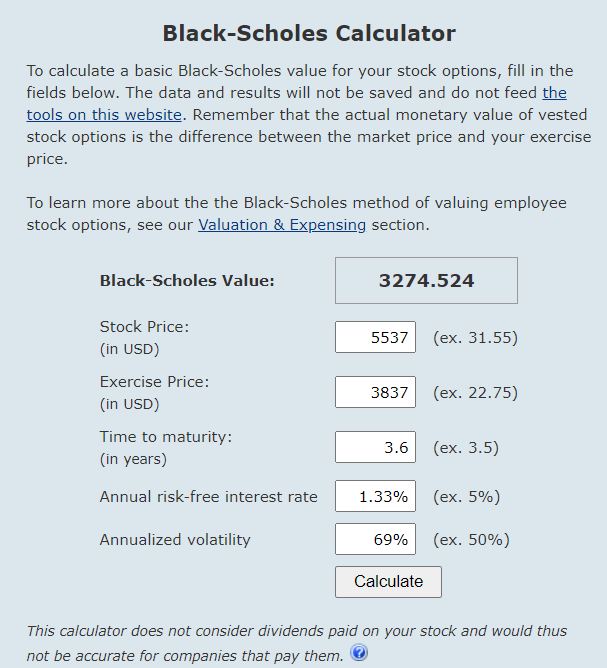

One strength of Black Scholes is that it explicitly considers volatility in commodity prices which are the primary determinate of whether a resource company will succeed or fail. The company mentions commodity price volatility 23 times in its 2020 audited financial statements and provides its estimate of the related volatility of its equity value in the notes to those statements, reporting volatility of 69% and a risk free rate of return of 1.33%. Those together with the market capitalization of the company’s equity and the value of its liabilities comprise all of the inputs needed to use the Black Scholes model to value the equity. The basic approach is well-described by Aswath Damodaran who teaches Advanced Valuation at NYU’s Stern School of Business.

In the case of MEG, the market value of the firm’s assets is equal to $2.7 billion equity plus $3.8 billion debt; the “strike price” for this real option is equal to the $3.8 billion debt; and, the risk free rate and volatility parameters I will use are those reported by the company. Entering these into the Black Scholes model returns a value for the equity of MEG of $3.3 billion. With 307 million shares outstanding that implies a share price of about $10.75 per share, versus the current trading price of about $9.00. Note that the calculations in the “calculator” below are in millions in the case of the dollar values shown, and are Canadian dollars despite the label USD in the chart.

Like all valuations, this one is as good as its assumptions and the Company’s estimates for volatility and risk free rate of return are suspect since I presume the company wants to report the lowest possible value for the stock options awarded its management both to mitigate the impact of those options on reported income and to reassure shareholders the awards are reasonable.

While interest rates today of 1.33% are typical for treasuries like the American 10-year note, they ignore inflation that is running at about 4%. A more reliable “risk free rate” is the implied risk free rate of real growth plus inflation which is more like 6%. The U.S. Energy Information Administration (EIA) reports that oil price volatility is at an all time high. If a 6% risk free rate and 120% volatility were used, the model would value MEG equity at $4.5 billion or almost $15 a share.

Either way, MEG shares appear undervalued today and that undervaluation seems likely to become deeper as free cash flow in the currently higher oil price environment brings debt down quite rapidly. Like all commodity companies, shares in MEG are not without risk.