Look to Riggertalk to guide energy investments

Markets look ahead - so can you

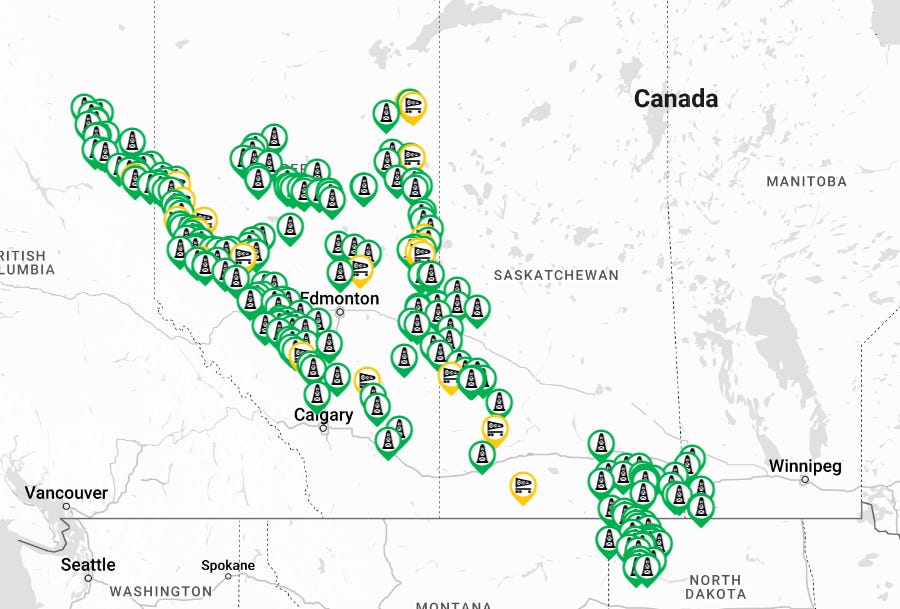

Riggertalk.com is a Canadian site that shows the location of every active drilling rig, who has commissioned the drilling and what service company is carrying it out. Future production of Canadian Exploration and Development companies can be estimated fairly accurately by paying attention to who is drilling and where they are actively doing so.

There is no shortage of activity in the Western Canadian Sedimentary Basin.

As we approach the 2023 reporting period and get updates on budgets and forecasts for 2024 and beyond, investors will react swiftly to both excitement or disappointment as the data come in. I try to get ahead of the reports by updating my models of the companies I follow and using data from the well logs reported to the Alberta Energy Regulator and estimate prospective results from current activity. That often gives me a leg up on the market.

Take Baytex (BTE.TO) for example. The shares of this highly leveraged and rapidly growing company have been in the doghouse for the past year as investors shy away from the risks of the debt Baytex took on to complete the acquisition of Ranger last year, falling from over CDN$6 in mid-October to the CDN$4.00 range today. But the drilling data suggest Baytex is rapidly expanding output, with six rigs active in key plays.

Source: Baytex rig locations from Riggertalk.com

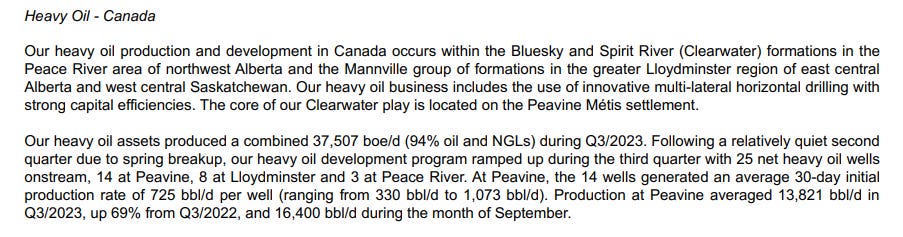

In November, Baytex reported that 13 new wells turned in an average initial production rate of 725 barrels a day in its Peavine play and that Peavine output had grown 69% over 2022.

Source: Baytex Q3 report

With six rigs active, and each rig capable of drilling several wells from the same location, I expect Baytex to report sustained growth in output in the Clearwater area and a strong fourth quarter of 2023. I model Baytex to exit 2023 with a production rate from all areas over 160,000 boe/day and annualized cash flow of over CDN$2 billion, more than enough to cover the company’s roughly CDN$1.3 billion capital program and make a serious dent in its debt levels. At a valuation multiple of 4 x EBITA, I model Baytex shares as having a value in the CDN$9 range, more than double today’s price.

There is plenty of slippage between the cup and the lip so I am cautious about getting carried away, particularly with the possibility of oil prices falling as global growth slows. Even so at current oil & gas prices, Baytex should generate enough cash flow to fund capital outlays, pay its nominal dividend, buy back somewhere around CDN$150 million in stock and still retire about CDN$500 millon of debt in 2024.

High risk, high return? Likely. I see Baytex as undervalued and hold my shares through stock options at a CDN$4 strike price maturing in January 2026 which I purchased for CDN$1.30 per option. I think the CDN$1 premium is worth the insurance it provides if oil prices do tank, but offer a return in the range of 80% if my estimate of value is realized in the market before the options expire.