Is Tesla undervalued?

Arguably not yet, but it might soon be

Tesla (TSLA) is a stock market darling and the world’s most valuable car-maker. The stock has had quite a ride as shown in this chart from Yahoo.com.

The nearly eight-fold run up in the TSLA stock price reflects the rapid and profitable expansion of the company’s business, moving from annual losses of close to $1 billion in 2018-2019 to a profit of $11 billion in 2021. With a market capitalization of ~$510 billion Tesla trades at over 50 times net income today, but the share price has fallen over 50% from over $400 a share a year ago. Is it time to invest?

In my opinion, not yet. A global recession is likely and high multiple stocks will very likely come more cheaply. Tesla is in the process of reducing output in its Chinese assembly plant, apparently owing to softening demand - something the company may be experiencing for the first time in its history. The company has repaid almost $50 billion of debt in the past four years and now has positive working capital of about $8 billion with cash generation of $16 billion in 2021 and a cash position over $20 billion. The risk of a liquidity crisis is now low as I see it. The question for investors is one of valuation. With over 3 billion shares outstanding at $171 share, will growth be enough to justify the share price?

In my view, that question is academic. A better question is how far the share price might fall in a recession and will any fall be exacerbated by the drama unfolding owing to Elon Musk’s $44 billion takeover of Twitter? Reportedly, banks carrying $13 billion of the takeover debt are looking for Musk to post some Tesla shares as margin for the debt and Wall Street is speculating that a margin call might prompt some forced selling of TSLA shares.

Let’s review the bidding on that. If the $13 billion debt were called and one way or another Musk was on the hook (an eventuality too complex for me to unravel) and Tesla shares had fallen to $100 a share, sale of 130 million shares would eliminate the debt. Musk holds about 25% of Tesla’s 3 billion shares and the shares trade ~80 million shares a day. I don’t see such an extreme situation arising or it becoming a material issue to Musk or Tesla if it did. But fear that it might happen could fuel selling of Tesla shares and bring the share price to a level where I would be a buyer.

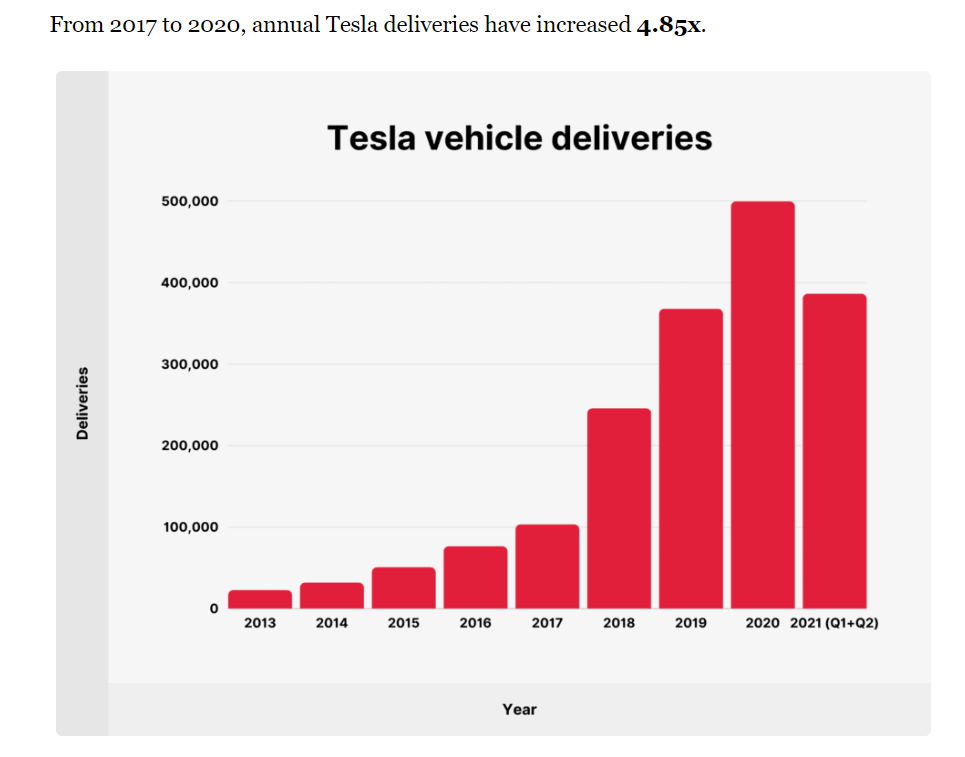

So what is that price? In my opinion, Tesla sales of its gorgeous electric vehicle models is likely to keep growing and I am going to value Tesla shares on the basis of a sustained 15 % annual growth rate, a far cry from the 48% annual rate of growth in unit sales of Tesla vehicles for the past 7 years.

Source: Backinfo

Tesla unit sales are projected at around 1.4 million vehicles for 2022. At a growth rate of 15% in unit sales, Tesla deliveries in 2027 would be 2.1 million vehicles and I estimate Tesla after-tax margin per vehicle at about $9,500, in line with estimates by others. That would profit in the $20 billion range in 2027 and, in my opinion, Tesla would be fairly valued at 30 times net income if the company can keep growing at a rate of 15% or higher. That translates into a market value of $600 billion or about $200 per TSLA share in 2027. I make investments in companies where I see the potential to double my money in a five year period, so I would be a buyer of Tesla shares at $100 a share and while that is well below the current share price of ~$170, a recession driven sell-off might see the shares drop to that level.

Others are willing to bet on higher growth and here is my rough estimate of the value of TSLA stock in 2027 at different growth rates:

20% - $330

25% - $405

30% - $494

35% - $600

While I have set $100 a share as my entry point for TSLA shares, a price that may never be reached, I would be inclined to buy into the company at higher prices if I were persuaded higher growth could be sustained, even at prices above today’s level. Higher growth will require investments in new assembly plants and new Gigafactories to build the batteries for the electric motors. Musk has plans to do just that, with his dream to build 20 million Tesla’s a year by 2030. If he can pull that off, TSLA stock is cheap today. There are some external barriers to overcome. There is a deepening shortage of battery metals - particularly copper and nickel - and the electrical grid in countries planning to mandate EV’s is in desperate need of expansion, and expanded electrical output is gated by the poor reliability of the ever popular “renewables” and the antipathy towards nuclear or fossil fuel generation. We already see some countries putting curbs on EV use during peak periods of electricity demand.

I miss many opportunities by being parsimonious but when I do put money at risk, I often make out well. So I will watch and wait and see if TSLA stock comes at a lower price. What is clear to me is that the Wall Street speculation about whether a $13 billion debt will bring Musk down to Earth is too remote for sensible consideration, but may assist me to open a position in the company at a deep discount to intrinsic value. Nobel laureate Richard Thaler demonstrated that investors overreact to unfavorable news and under-appreciate beneficial trends. His insights suggest the news flow might be my friend in contemplating a Tesla investment.

I own no TSLA shares today but that could change without notice.

Hi Michael, very interesting read. One of the things that Elon keeps talking about re: competitive advantage for Tesla is the advancements in self-driving technology. He might be right. The business model for the self-driving technology is actually a subscription model. So as this technology comes mainstream and really good, each car that Tesla sells will have re-occurring stream revenue...

Sophisticated analysis - as usual. (BTW I think you mean antipathy rather than antithesis.)