How have the stocks I cover performed?

This is an update after a few questions from readers

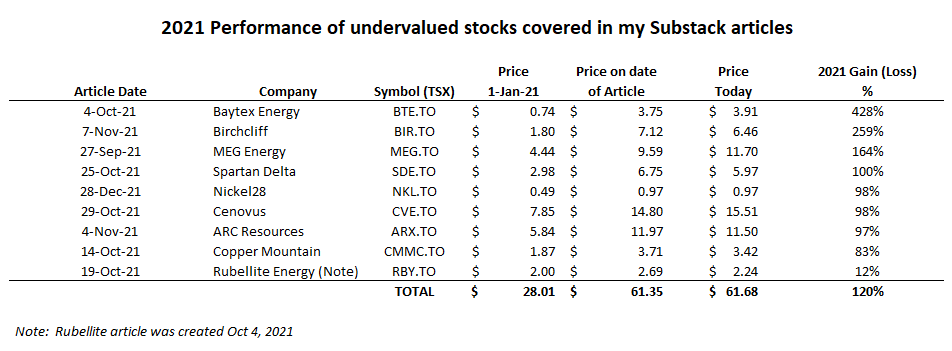

Last year I published an article summarizing the 2021 performance of the stocks I have written about here on Substack, which showed a return of 120% for all of 2021.

Some readers have asked: “2021 is fine, but how have these stocks have done since the articles were published?” That is a fair question since some readers conflate my articles with recommendations. I don’t make recommendations about stocks but I do present the stocks I cover as “undervalued”.

Here is an update on the performance of the stocks listed since the date of the related articles. The calculation of return is absolute, not converted to an annual rate, which would be much higher than the absolute return since the various articles have been outstanding since September 27, 2021 at the earliest and the absolute return since that date comprises just over 4 months of change and the annual rate would be at least three times the absolute gain.

On average, the gains have been a robust 39% and I expect these names to continue to benefit from firm oil & gas prices and disciplined management. Both laggards Birchcliff and Copper Mountain reported strong results when 2021 Q4 was released since both companies are enjoying commodity prices well above prior year levels, and both companies have paid down debt with free cash flow over the year.

I also wrote an article on Peyto Exploration just a few days ago on January 24, 2022. Peyto stocks was $9.57 on that date and today is $11.73, a gain of about 23% in the 40 days since I wrote. Peyto reports Q4 results on March 9, 2022 and I expect the company to demonstrate its earning power in that report. Peyto pays a dividend of $0.05 a month for a yield of over 5%. It is worth watching.

The 39% gain for the portfolio in a period of less than five months on average shows returns of ~100% at annual rate. If commodity prices remain firm, there is every reason to believe those kinds of returns will continue for a while longer.

Ill-conceived “climate change” policies have created a global energy shortage driving oil to US$115 a barrel and natural gas to $5.00 per thousand cubic feet in North America and over $30 per thousand cubic feet in Europe. This thoughtless set of policies will exacerbate the energy shortage and very likely drive fossil fuel prices mugh higher over the next few years. Economies will suffer from the resulting inflation and needed increases in interest rates to keep inflation under control, and stocks generally are more likely to trade lower than keep rising in the face of slower economic growth and higher rates. However, oil & gas stocks are beneficiaries of the government silliness and energy investors can expect higher prices, rising dividends, lower debt levels and long term gain.