Headwater Exploration is poised for gains

Robust Clearwater economics and a clean balance sheet

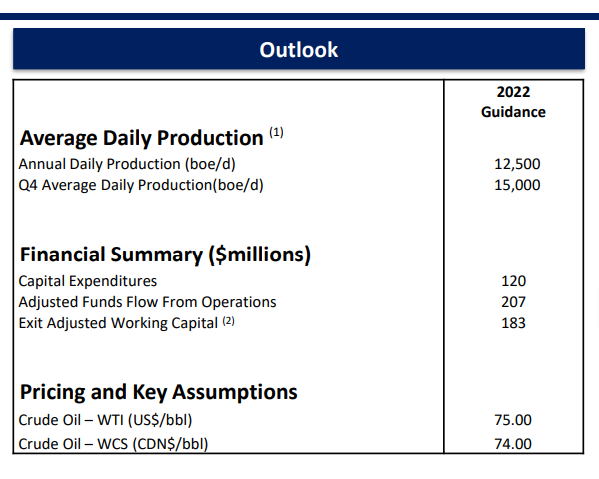

Headwater Exploration (HWX.TO) is a debt free pure play on the Clearwater development in Alberta, possibly the most exciting oil & gas development in Canada’s Western Canadian Sedimentary Basin today. Operating costs are low and field netbacks are about $40 to $45 per barrel of oil. Production today is running at about 8,000 barrels a day but growing rapidly. Management foresees average 2022 production of about 12,500 boe/day and cash flow from operations of $207 million based on a capital expenditure budget of $120 million. By year end, the company foresees production at a rate of 15,000 boe/day.

The company’s budget is predicated on oil prices of US$75 WTI and Western Canadian Select of CAD$74 a barrel. Current oil prices are somewhat higher than the budgeted levels.

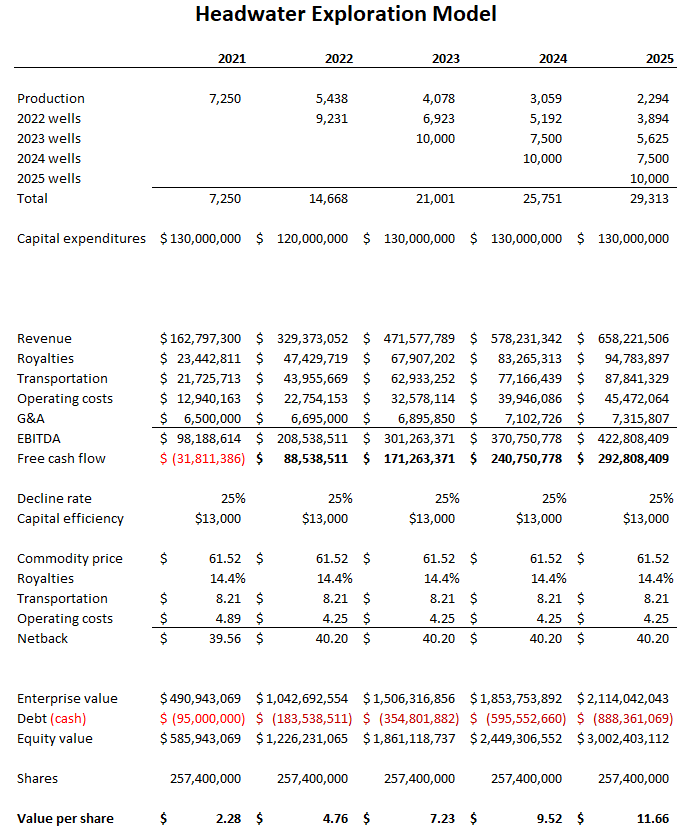

I have modeled Headwater’s operations over the next five years based on an average realized oil price of CAD$62 a barrel and current operating economics. That model shows both rapid growth in production and in cash on the balance sheet, with production approaching 30,000 boe/day by 2025 and the cash balance close to $900 million. With current oil prices well above that level, my model should be conservative at least for the short term.

Based on a modest EBITDA multiple of 5 times (which would be low for a company with this growth profile) I expect to see the share price rise to the $12 range from less than $7.00 today. Given the dramatically increasing cash balance, I would expect both a dividend and share buybacks with a lot of optionality in terms of growth, mergers and acquisition opportunities or simply a generous dividend.

In my opinion, Headwater is a relatively low risk way to benefit from tight global markets for oil with little risk of failure. I own 15,000 shares.