Has natural gas production peaked in the U.S.?

If it has, Canadian gas producers will benefit

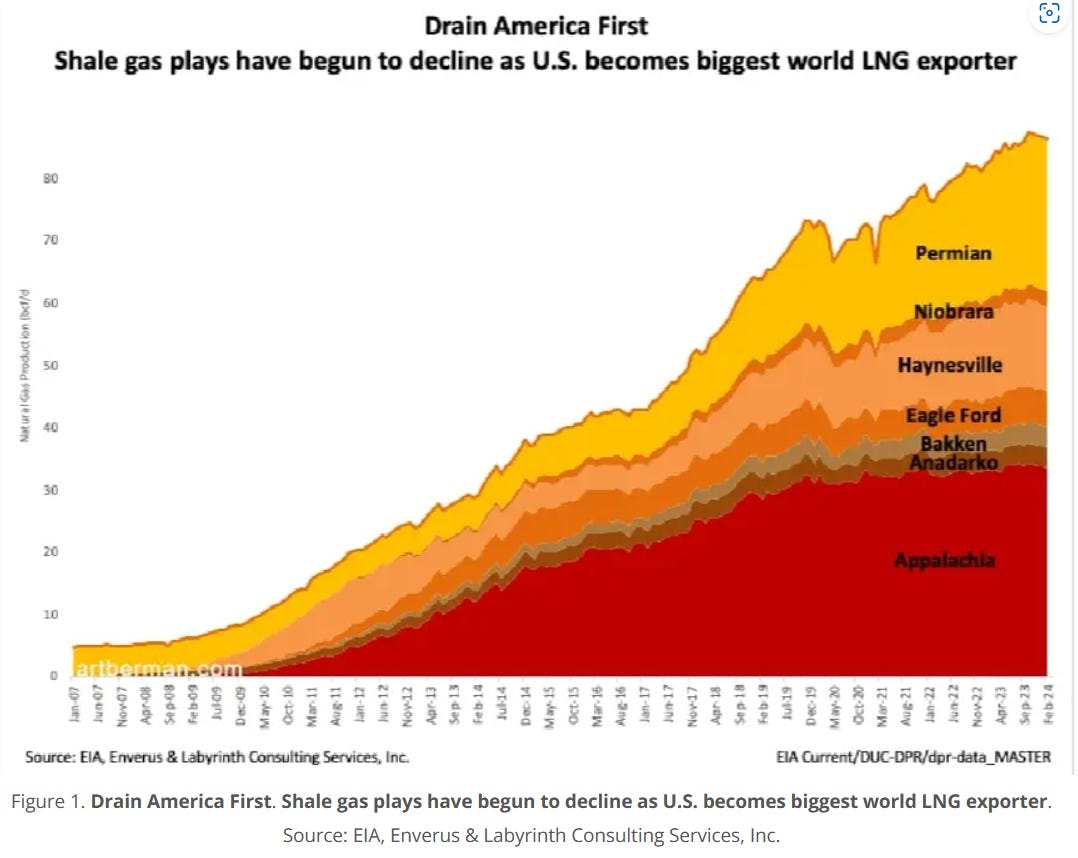

In a recent article, petroleum engineer Art Berman claims that United States shale gas hads run its course and will decline sharply in the next few years. Berman opens his article with this troubling chart showing that share gas output is levelling off just as U.S. LNG exports catch fire. Shale gas comprises 82% of U.S. gas output according to Berman (I am a bit skeptical since “associated gas” from oil production is likely more than 18% and there are other conventional gas wells).

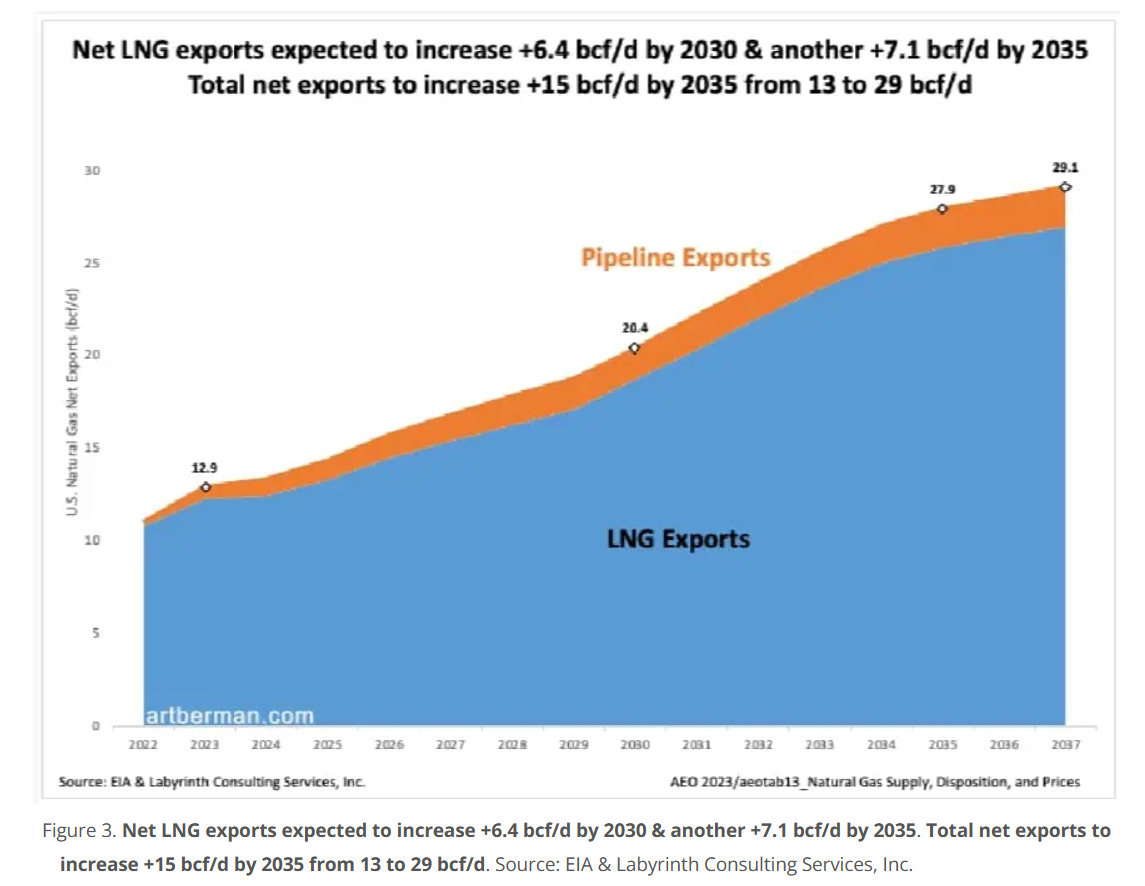

Whether 82% is an overstatement, it is inarguable that shale gas comprises a major source of natural gas in United States, and if growth from that source begins to decline and LNG exports keep rising, shortages are sure to follow. Berman includes a chart showing natural gas exports by pipeline to Mexico and in the form of LNG may double within the next decade.

Natural gas trades at a fraction of the price of oil in terms of its energy content. At a 6.1 Mcf/barrel of oil ratio which approximates the relative energy content, BTU equivalent prices would see gas trading at over US$12.50 a gigajoule with oil in the low US$70’s versus the current price at Henry Hub of about US$2.50. A shortage of gas will not prompt a switch to oil as fuel given those economics, so it will more likely manifest itself in a rise in field prices for natural gas.

Higher prices will not create additional gas in declining shale fields but might prompt a rise in conventional gas drilling from a low base, but a more likely source of the needed gas is Canada where the infrastructure is already in place. Suppose natural gas in the U.S. rose to US$6.00 per gigajoule and the cost of transportation to American hubs (often called the “basis”) is about US$1.50 (it is less than that today), Canadian producers would realize US$4.50 a gigajoule for exported gas, equivalent to about CDN$6.00 a gigajoule.

What does that mean for Canadian E&P’s? The answer is complex for some companies but relatively straightforward for others. For $PEY.TO $BIR.TO $SDE.TO $BNE.TO and $PNE.TO I see the following cash flows and implied share prices at a steady CDN$6.00 a gigajoule for gas and all other output at today’s prices (all in Canadian dollars).

Peyto - Cash flow of $1.8 billion and a $38 share value

Birchcliff - Cash flow of $800 million and a $13 share value

Spartan Delta - Cash flow of $330 million and a $10 share value

Bonterra - Cash flow of $150 million and a $12 share value

Pine Cliff - Cash flow of $230 million and a $2.50 share value

If Berman is right, shortages of natural gas will manifest themselves in the next four or five years and Canadian natural gas realizations should rise. Longer term investors in natural gas producers should see substantial increases in cash flow, dividends and share prices if that happens. I hold substantial positions in each of the companies listed since I believe shortages of natural gas are more likely than surpluses with a few years despite what seems to be a surplus and softer prices today.

I am grateful to Art Berman for his excellent analysis and willingness to share it with others.

BTW- I am a big fan of Canadian operators. Long -BTE, Peyto, BIREF, CPG, ATHOF, SU, PDS, and a couple of others. Counting the days until the TMX is shipping. Cheers

I normally like Berman's "the end is near" stuff. This one was a swing and a miss for the lad. Only the Haynesville is off a bit recently due to rig count, but up 5 BCF/D from 2020. The Permian is producing 7-8 BCF/D more than it did in 2020, and getting gassier by the day. The Marcellus is up 2 BCF/D since then. Will shale gas peak? Of course, we're nowhere near that yet. Cheers