Has Headwater gotten ahead of itself?

Investors love the company. Despite a short RLI I think there are hidden values

Headwater Exploration (HWX.TO) has been an energy investor darling since it was first publicly traded. What is not to like - rapid and profitable organic growth without debt and a sensible dividend policy. But as I do with all commodity based companies, I estimate intrinsic value based on NI 43-101 Reserve Reports and using a modified Black-Scholes methodology.

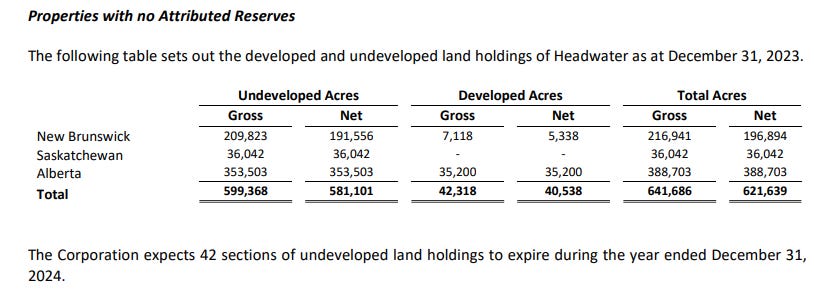

Where this methodology falls short is when the company being evaluated has extensive unexplored or undrilled acreage and can add reserves at low cost. In the case of Headwater, proven plus probable reserves grew from about 29 million barrels of oil equivalent at year end 2022 to almost 43 million barrels of oil equivalent at year end 2023, and Headwater has 581,101 acres of undeveloped land (although rights to 42 sections equal to 26,880 acres will expire undeveloped during 2024).

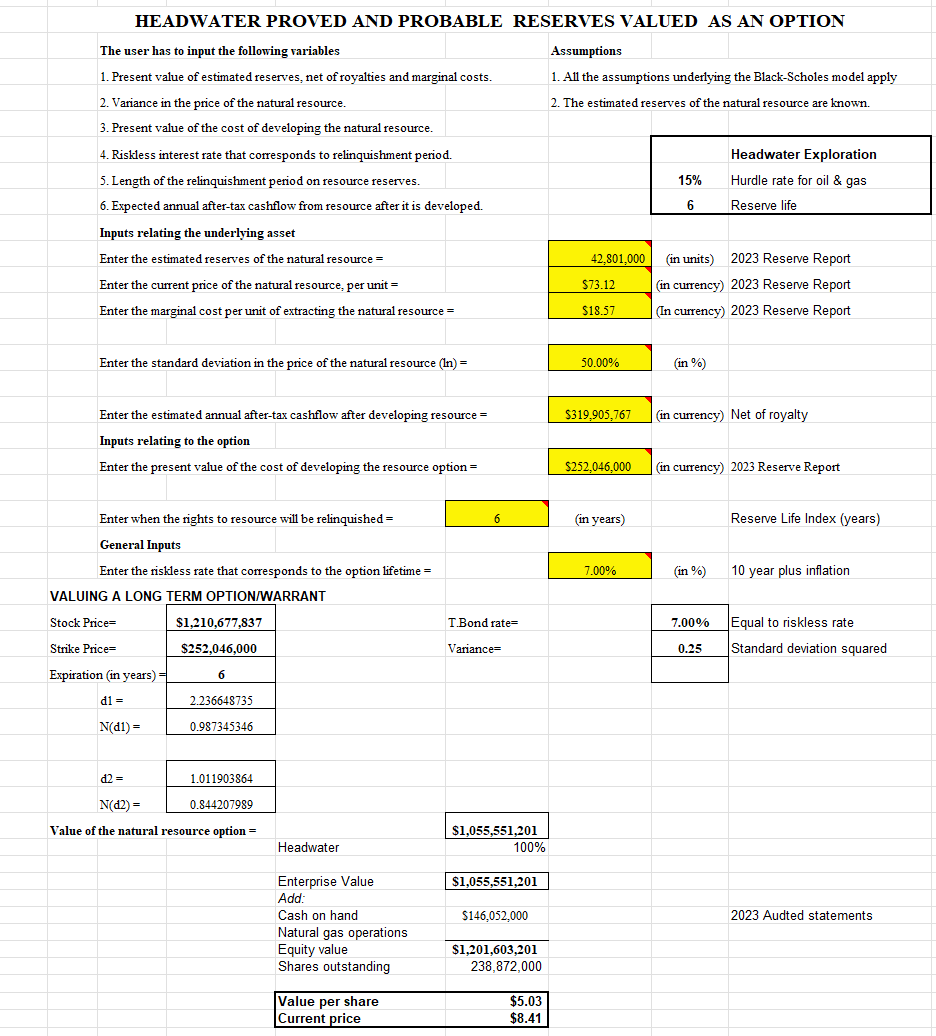

With production for 2024 (according to the company’s guidance) expected at ~20,000 barrels of oil equivalent a day, the company’s reserve life index (RLI) appears to be 42,801,000 / (20,000 * 365) = 6 years. Obviously if the company can add about 2 years reserve life while producing about 7 million barrels of oil equivalent a year, the RLI is misleading. Since the reserves recorded reflect development of only 40,538 acres, actual reserves (assuming equal success and productivity, a bit tenous but useful anway) actual reserves may be mroe than ten times those reported. The proof is in the drill bit and it merits watching.

If the RLI was in fact only six years, the Black Scholes method returns a value per share of CDN$5.00 per share versus a market price in the CDN$8.40 range.

The market clearly sees drilling success as likely to persist, and so do I. If actual reserves (or at least those I have inferred without data) are in the 400 million barrel range and production continues at current rates over a 60 year reserve life, the Black Scholes model returns a value of close to CDN$9.00 a share. Higher production rates will shorten the inferred 60 year RLI but result in a higher valuation (the magic of present value).

Obviously, Headwater managed has to balance growth rates with investors’ desires for sustained or increasing dividends and the availability of drilling rigs and geological data to guide drilling, so the ultimate value of the company is in hands of management (which is first class).

I believe the underlying value of Headwater shares (with all the usual caveats about oil prices, drilling risks, etc.) is probably in the CDN$15.00 range and expect investors who hold the stock long term will enjoy the ride.

"If the RLI was in fact only six years, the Black Scholes method returns a value per share of CDN$5.00 per share versus a market price in the CDN$8.40 range."

So suddenly black scholes valuation proved to be wortheless.